Our DSCR program is specifically designed to assist new and experienced real estate investors in financing their properties, qualifying based on the cash flow generated by the investment.

Program features

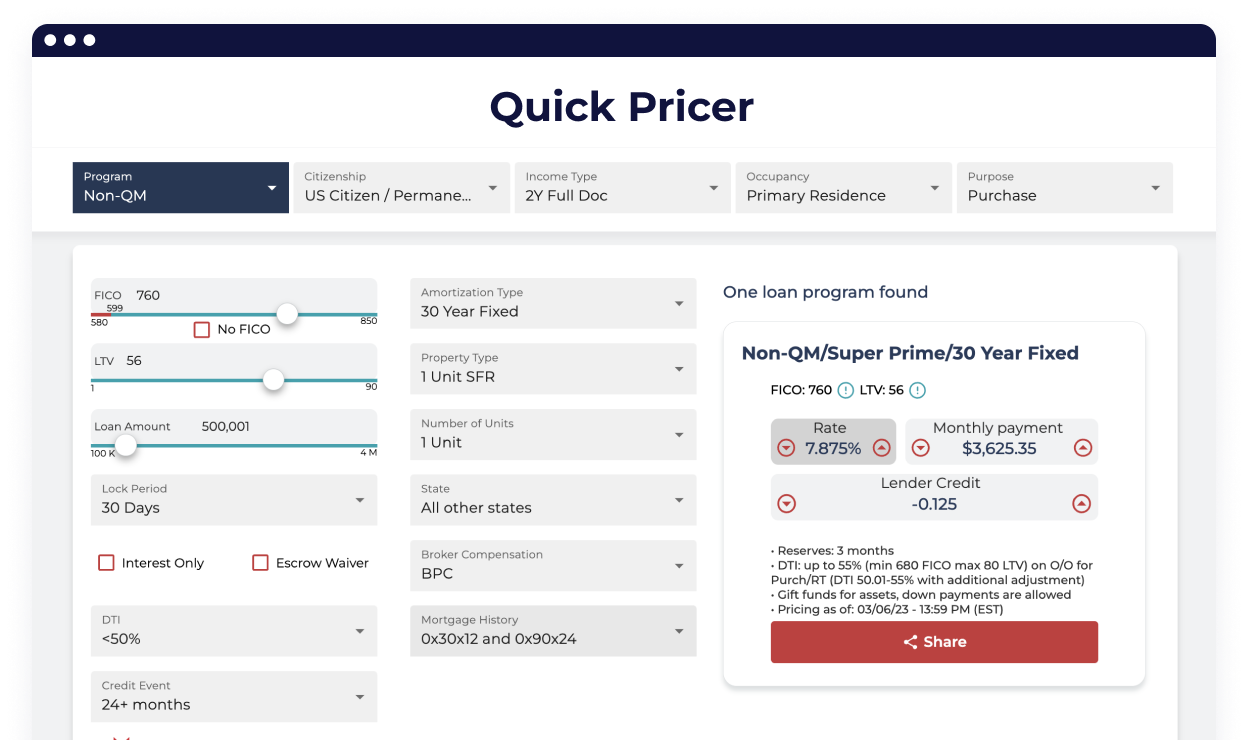

Struggling with a loan scenario? Push the button and get a solution in 30 minutes!

Write to us, we will contact you within 30 minutes.

24 hours

24 hours

24 hours

24 hours

A debt service coverage (DSCR) loan is one that qualifies borrowers through an investment property’s cash flow rather than the borrower’s income. DSCR loans — also known as investor cash flow loans — are frequently used by real estate investors to qualify for mortgages and buy investment properties.

The debt service coverage ratio (DSCR) is the ratio of an investment’s net operating income to its total debt service. It is a way of determining whether a borrower has enough cash flow to pay its current debt obligations.

DSCR can have applications in business, government, and personal finances. Like DSCR loans, this ratio is often used in real estate to determine whether an investment property’s cash flow can cover its mortgage payments.

The higher the DSCR, the better the ratio. A DSCR above 1 means that an investment property has positive cash flow and enough net operating income to cover its debts. As a general rule, anything above 1.25 is considered a good DSCR.

When your borrower applies for a mortgage loan, we look at their income to determine how much they can afford as a monthly payment. The key figure examined is the debt-to-income ratio (DTI), which is the percentage of their monthly income that goes toward debt.

But in the case of investment properties, A&D Mortgage offers DSCR loans. Rather than looking at a borrower’s income, we consider the expected monthly rent from the property. And instead of using the DTI to determine eligibility, we look at the DSCR.

While DSCR loans may not have the exact same requirements as Conventional mortgages, there are still guidelines real estate investors will have to meet to qualify.

Unlike Conventional mortgages, DSCR mortgages are not backed by entities like Fannie Mae and Freddie Mac. Therefore, there are no standardized requirements. However, there are a few things that we will look at.

Property eligibility. DSCR loans can be used for investment properties with one, two, three, or four units. In certain cases, we have been able to approve up to eight units!

DSCR loans have many advantages including: