Post content:

If the borrower believes they are stuck in a Non-QM solution that does not fit their needs and goals, the broker should educate them about the main exit strategy – refinancing. This article explores how this process works, helping the broker to come prepared for the common question, ‘Can you refinance a Non-QM loan?’

Direct Answer: Yes, you can refinance a Non-QM loan. Borrowers may refinance into another Non-QM loan or transition into a Qualified Mortgage if their financial profile changes. The right path depends on timing, credit, documentation, and the borrower’s long-term goals.

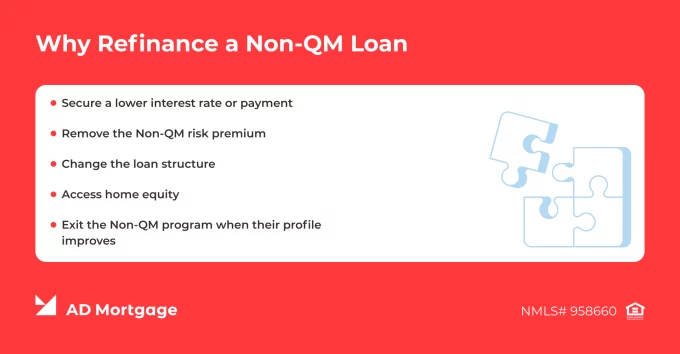

Why Borrowers Refinance a Non-QM Loan

There are many reasons why borrowers might want to refinance their Non-QM loans:

- Secure a lower interest rate or payment

- Remove the Non-QM risk premium

- Change the loan structure

- Access home equity

- Exit the Non-QM program when their profile improves

If any of these reasons apply to your client, refinancing may be the right choice.

When Does Refinancing a Non-QM Loan Make Sense?

Non-QM refinance is typically performed when the borrower’s financial profile has changed, allowing them to qualify for loans with lower rates. For example:

- Credit score increases – usually because of late payment removals or reduced revolving balances

- Income documentation changes – for example, when transitioning from freelance work to stable employment and demonstrating consistent income

- Home value increase – often due to appreciation, renovations or principal paydown of the original loan

- Stabilized financial picture – including a reduced debt-to-income ratio, increased cash reserves, or credit event seasoning

- Clear net tangible benefit – which is crucial for compliance and broker credibility

Can You Refinance from Non-QM to a QM Loan?

To refinance a Non-QM loan, the borrower must meet the eligibility requirements of the new loan – the transition is not automatic and depends on the borrower’s current financial profile.

For many borrowers, Non-QM loans serve as a temporary bridge, helping secure financing when traditional options are unavailable. Then, when their profile improves, they might refinance into a QM loan to access lower rates or reduce risk premiums.

Which mortgage type to refinance a Non-QM loan into – Qualified Mortgage vs Non-QM?

- Non-QM → QM. The borrower now qualifies for an agency-backed or conforming mortgage and seeks to reduce monthly payments. Refinancing requires full documentation and compliance with QM rules.

- Non-QM → Non-QM. The borrower’s profile is not yet strong enough to qualify for traditional financing, but a new Non-QM product may provide lower rates or reduced risk premiums.

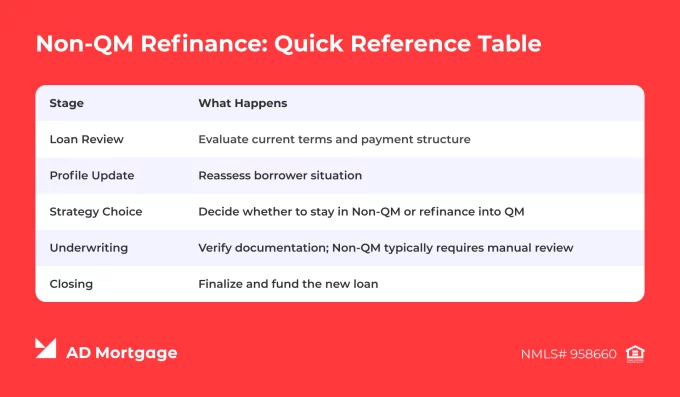

Step-by-Step: How Non-QM Refinancing Works

Typically, refinancing goes through five key stages. The broker’s task is to walk their clients through the process, explaining each step clearly.

Step 1. Evaluate the Current Loan

The broker evaluates the loan terms, interest rates, and payment structure to determine whether the current loan fits the borrower’s long-term goals. It is also important to understand the prepayment penalties or exit fees early in the process.

Step 2. Reassess Borrower Profile

The borrower’s creditworthiness depends on a variety of factors. The broker should review income documentation, credit score, assets, cash flow, and other financial information to determine QM eligibility or qualification for better Non-QM pricing.

Step 3. Determine Refinance Path

While considering the borrower’s strategic goals, the broker evaluates the financial benefits of refinancing and decides whether to stay in a Non-QM loan or transition to a government- or agency-backed mortgage.

Step 4. Underwriting and Approval

The lender verifies the documentation – full documentation for QM loans or alternative documentation for Non-QM loans. While QM loans typically use automated underwriting, Non-QM options are usually reviewed manually.

Step 5. Close and Reset the Loan

At the last stage, the loan is finalized, similar to the traditional mortgage process. The broker should update the borrower on post-close obligations, such as escrow or insurance.

Non-QM Refinance: Quick Reference Table

Common Misconceptions Brokers Hear

- ‘I am locked into Non-QM.’ – Consistent work on improving the borrower’s financial profile can expand mortgage options and help them qualify for traditional loans.

- ‘It takes years to refinance.’ – If there is no prepayment penalty restriction, the borrower can refinance as soon as they qualify and when it makes financial sense. It is often possible to stabilize credit, prepare documentation, and build equity within 6 to 12 months.

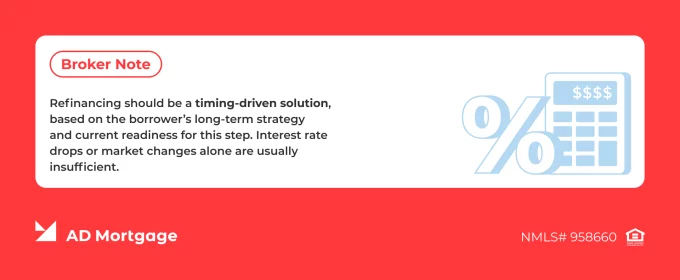

- ‘Rate drop is the only thing that matters.’ – Although market rates impact the decision, refinancing should only be performed if it improves the borrower’s overall financial position and helps them achieve their long-term financial goals.

How AD Mortgage Supports Non-QM Refinance Strategies

AD Mortgage is a leading Non-QM lender and offers a variety of mortgage solutions, including refinancing options – both Non-QM and QM programs.

Visit our Non-QM loan programs page for an overview of our solutions and choose the best-fit program for your borrower’s case.

Broker Talking Points

- ‘Non-QM is not necessarily a permanent solution. Consider it a bridge, connecting you to a traditional loan and more favorable terms in the long run.’

- ‘Refinancing depends on your readiness and is less driven by market changes or rate drops.’

- ‘The goal is to align refinancing with your long-term financial goals, not just chase a lower rate.’

FAQ: Non-QM Refinance

Can You Refinance a Non-QM Loan?

Yes. A borrower can refinance a Non-QM loan into a QM loan or another Non-QM product, as long as they meet the requirements of the new mortgage.

Can You Refinance from Non-QM to QM?

Yes. Refinancing into a QM mortgage is possible – typically when the borrower’s financial profile has changed through a higher credit score, stabilized finances, or a transition to traditional income.

Is There a Waiting Period?

Generally, Non-QM loans do not require a seasoning period, allowing refinancing as soon as the borrower qualifies.

Can You Do a Cash-Out Refinance?

Yes. Many lenders, including AD Mortgage, offer cash-out options – submit a scenario request and choose the program that fits your needs.

Does Refinancing Remove Non-QM Features?

When refinancing, the rules of the new loan apply. Therefore, transitioning to a QM loan can eliminate some Non-QM features such as interest-only payments or higher risk premiums.

Do Brokers Need Different Documentation?

To qualify for a traditional mortgage, borrowers typically need to provide full documentation instead of alternative documentation accepted for Non-QM loans.

Struggling with a loan scenario?

Get a solution in 30 minutes!Fill out the short form and get a call from our AE

Submit a ScenarioThank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again