Post content:

Brokers often field questions about conventional loan requirements – as this remains a highly relevant issue for mortgage originators and their clients.

However, the key isn’t simply knowing the list of requirements. It’s understanding which ones offer flexibility and which factors are more likely to create real friction. In this article, we explore conventional mortgage requirements through that practical lens.

What are the Requirements for a Conventional Loan?

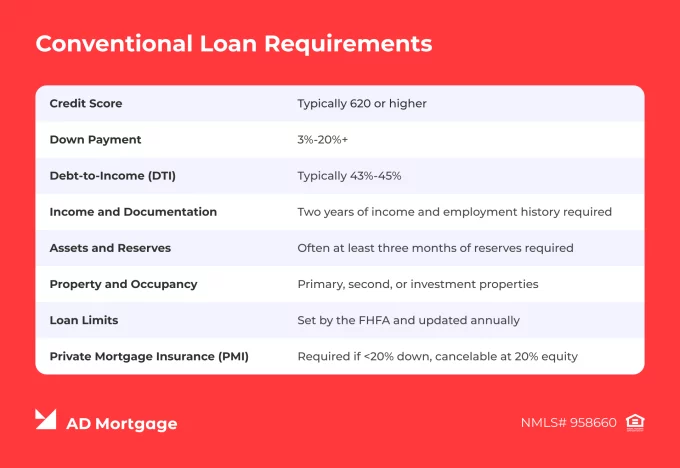

While the requirements for conventional loans are not universal and vary by mortgage lender and program, there are common criteria that can be used as a basic reference:

- Credit Score – The minimum required score is typically 620. However, a higher credit score results in better terms. Improved pricing usually starts at around 740. Apart from the score itself, lenders review the borrower’s full credit history, as negative events and outstanding debts can trigger manual underwriting or overlays.

- Down Payment – First-time homebuyers can qualify for a down payment as low as 3%. The standard down payment requirement for conventional loans is between 5% and 20%. Additionally, a down payment above 20% removes the need for private mortgage insurance (PMI) and contributes to better pricing.

- Debt-to-Income (DTI) – The maximum DTI is often 43%-45%, but the threshold might stretch to 50% with strong compensating factors. Lower DTIs receive better pricing, and higher DTIs increase sensitivity to other risk factors.

- Income and Documentation – Two years of income and employment history are typically required to demonstrate stable and sufficient cash flow. Accepted income documentation includes pay stubs, W-2s, tax returns, bank statements, and other financial documents.

- Assets and Reserves – Generally, three months of reserves are needed. Assets and large deposits serve as compensating factors but might require explanations and additional documentation.

- Property and Occupancy – Conventional loans provide significant flexibility in terms of eligible property types. Primary residences, second homes, and investment properties can be purchased if they meet minimum property condition standards and appraisal requirements.

- Conforming Loan Size Rules – To maintain favorable pricing, loans should stay within FHFA loan limits. When exceeding those limits, the loan becomes a jumbo loan and may come with stricter underwriting guidelines.

- Private Mortgage Insurance (PMI) – If the down payment is less than 20%, the borrower must pay PMI, the cost of which depends on the borrower’s overall profile. Once the borrower reaches 20% equity, PMI can be canceled.

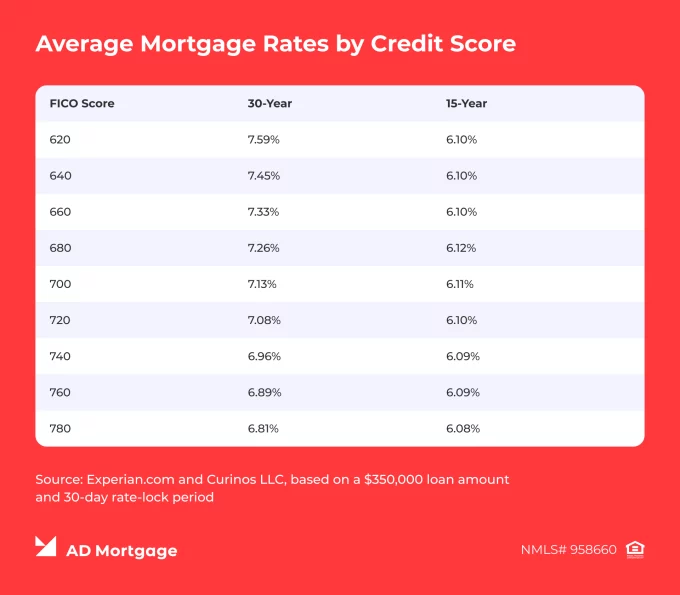

Minimum Credit Score for a Conventional Loan

For conforming conventional loans, lenders typically set 620 as a baseline threshold. However, the minimum qualifying score doesn’t guarantee approval or favorable loan conditions.

To achieve improved pricing and terms, borrowers are expected to have a conventional loan credit score of around 700-720 or above. Generally, a higher score results in better pricing, but it is not the only factor that leads to approval.

Let’s take a look at two borderline cases and ways brokers can handle them.

1. Borrower has a credit score of 620and a strong overall profile

While the score is relatively low, the file can be approved if other factors are clean. For example:

- Stronger reserves show the borrower’s financial stability

- DTI below 40% indicates a lower level of risk

- Stable employment and standard income documentation make the file simple and conservative

In this case, a mortgage originator can match their client with the Conventional Standard program by AD Mortgage, which offers competitive rates and flexible down payments starting at 3%.

2. Borrower has a credit score of 620 and a weak overall profile

High DTI, lack of reserves, high LTV, or recent negative credit events indicate weak repayment capacity. Combined with a low credit score, these risk factors can trigger automated underwriting system (AUS) findings that require manual underwriting or lead to denial.

Overall, such borrower profiles have a lower probability of approval under conventional guidelines. Instead of trying to match them with a conventional loan, brokers can advise their clients to improve their profiles and reduce risk layering.

Down Payment Requirements for a Conventional Loan

First-time homebuyers can qualify for a minimum conventional loan down payment of 3% if they meet credit score, occupancy, and other eligibility requirements. For repeat homebuyers, the down payment often starts at 5%, and most conventional loans fall within the 5%-20% range.

A higher down payment can help achieve better pricing and may serve as a compensating factor for a lower credit score. Additionally, when making a down payment of 20% or more, the borrower is not required to pay private mortgage insurance (PMI).

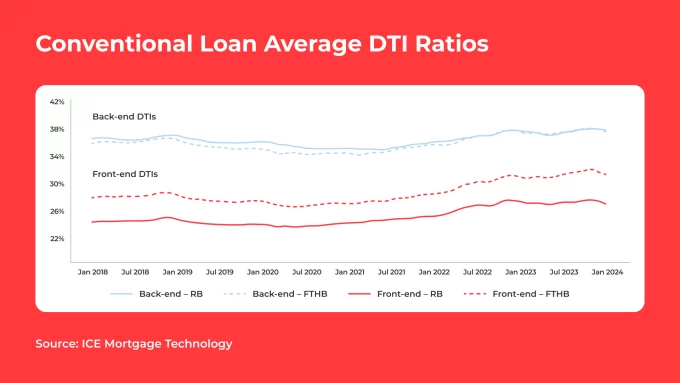

Debt-to-Income Ratio Requirements

Although the conventional loan Debt-to-Income (DTI) ratio is a sensitive variable, it is not sufficient on its own and should be evaluated in the context of the borrower’s overall profile.

Typical DTI limits for conventional loans are 43%-45%, but some lenders accept DTIs up to 50% with strong compensating factors. Generally, lower DTIs help offset risks associated with other variables and lead to easier approvals. Higher DTIs, on the other hand, might indicate risk layering and may require more careful underwriting.

Income, Assets, and Documentation Requirements

The lender needs to ensure the borrower’s cash flow is consistent, verifiable, and sufficient to cover monthly obligations. Therefore, lenders typically evaluate:

- Income Documentation – W-2 forms or pay stubs for salaried income, tax returns or bank statements for self-employed income, and other types of documentation are accepted

- Employment Consistency – Usually a two-year history is required. Frequent job changes might require an explanation

- Asset Sourcing – Demonstrates the legitimacy and stability of the borrower’s financial resources, serving as a backup for repayment

- Funds to Close – Down payment and closing costs must be liquid, documented, and traceable at closing

- Reserves When Needed – Often, three months of housing payment (PITIA) reserves are required. Strong reserves act as a compensating factor for higher-risk files

Clean, complete, and consistent documentation is key to moving the file forward quickly. To prevent back-and-forth conditions or delays, brokers must ensure that all borrowers’ assets are verified and properly sourced.

In borderline cases, additional attention must be paid to reserves. Strong reserves can offset weaknesses elsewhere in the file, such as higher DTI or lower credit scores, and improve approval likelihood.

Property Type and Occupancy Requirements

Conventional loan requirements vary based on property occupancy type:

- Primary Residence. These lower-risk loans typically offer the most flexible terms, including a minimum down payment of 3% for first-time homebuyers and 5% for repeat buyers, a 620+ credit score, DTI up to 50% with compensating factors, and often three months of PITIA reserves.

- Second Home. These loans have stricter requirements, such as a down payment usually over 10%, reserves of up to 6 months of PITIA, and tighter credit score expectations.

- Investment Property. In addition to higher interest rates, investment loans often require a 15%–25% down payment, a 680+ credit score, 6+ months of PITIA reserves, and more thorough review of income documentation.

Conventional loans are mostly designed for one-unit properties. Two-to-four-unit properties can still qualify as primary residences if the borrower occupies one unit, but they often require higher down payments, additional reserves, and stricter underwriting compared to single-unit homes.

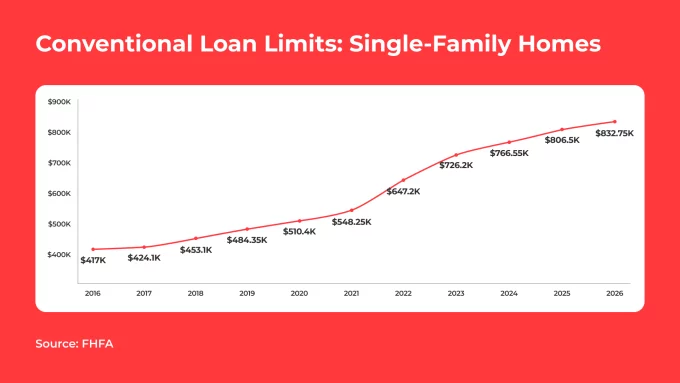

Loan Limits and Loan Size Requirements

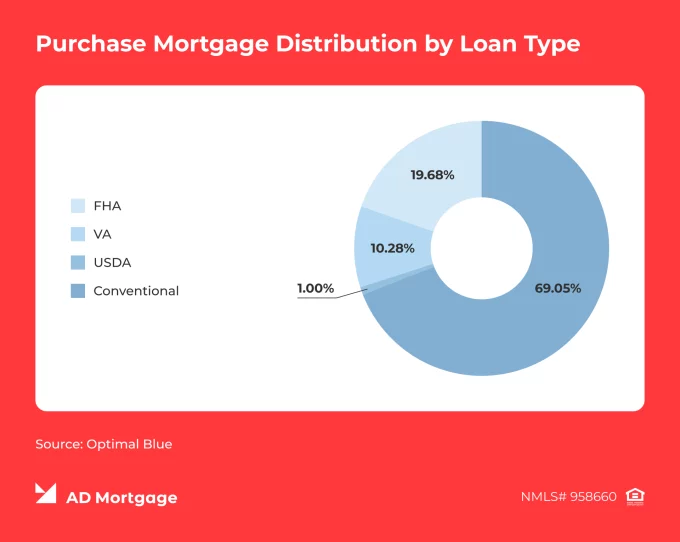

Many conventional loans are conforming, meaning they follow the Fannie Mae and Freddie Mac guidelines, and are therefore less risky for lenders and more affordable for borrowers. Conforming loans must stay within FHFA limits, which vary by county and are updated annually. In 2026, the baseline one-unit conforming limit is $832,750.

When a loan exceeds these limits, it becomes non-conforming, also known as a jumbo loan. Jumbo loans typically require higher credit scores, larger down payments, stronger reserves, and stricter underwriting, and they generally offer less favorable pricing.

Do Conventional Loans Require PMI?

Private Mortgage Insurance (PMI) is insurance that protects lenders in case of borrower default. Thanks to PMI, conventional loans with low down payments are available to borrowers who may not be able to put 20% down.

PMI is required if the borrower makes a down payment of less than 20% of the home’s value. PMI is typically paid monthly until the borrower reaches 20% equity – at which point it can be canceled upon request. When the borrower reaches 22% equity, PMI is automatically canceled.

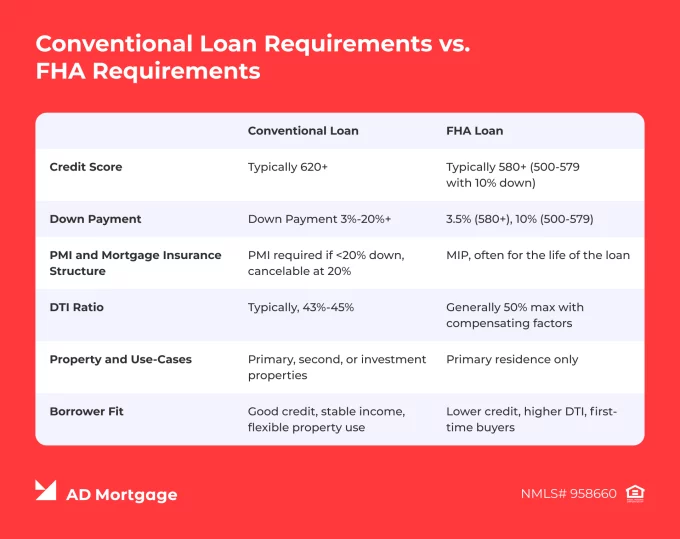

Conventional Loan Requirements vs FHA Requirements

Borrowers, especially moderate-income first-time homebuyers, often compare conventional loans to FHA loans to choose the best combination of terms and requirements. We have collected the common criteria for conventional and FHA loans in the comparison table below, including the preferred borrower fit for each.

Who Qualifies Most Easily for a Conventional Loan?

While conventional loans are flexible and can be used in different scenarios, there are some cases that align particularly well with conventional loan requirements:

- Borrowers with strong credit profiles

- Borrowers with stable income and well-documented assets

- Borrowers seeking lower down payment options who still meet conventional qualification criteria

- Borrowers comparing conventional vs. FHA loans based on PMI and overall mortgage insurance costs

- Borrowers aiming to stay within conforming loan limits

At the same time, mortgage originators should recognize borrower profiles that may require more careful analysis before selecting a loan solution:

- Borrowers with lower credit scores

- Borrowers with higher DTI ratios

- Layered risk scenarios

- Borrowers with larger loan amounts approaching or exceeding conforming limits (jumbo loans)

Common Misconceptions about Conventional Loan Requirements

Borrowers may not fully understand the complexity and nuances of conventional loans, so brokers play a key role in clarifying common misconceptions and educating clients. You can use the following talking points:

- ‘Conventional does not mean 20% down.’

- ‘A 620 credit score may be a common baseline, but it does not guarantee approval or favorable pricing.’

- ‘Conventional and conforming are related terms, but they are not identical.’

- ‘PMI does not mean a conventional loan is automatically a bad fit.’

- ‘Approval is based on the overall profile, not a single factor such as credit score or DTI.’

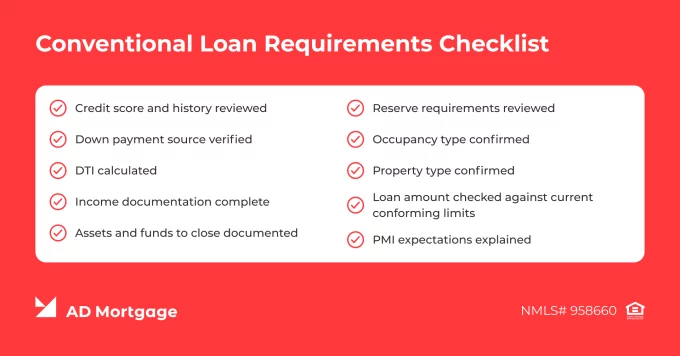

Conventional Loan Requirements Checklist

There are many small steps in the conventional loan workflow that brokers should remember. To make the process smooth and efficient, we have collected a handy checklist.

FAQ: Conventional Loan Qualifications

What Credit Score is Needed for a Conventional Loan?

Typically, lenders accept credit scores starting at 620. However, higher credit scores can help borrowers qualify for better pricing and more favorable loan terms.

Can You Get a Conventional Loan with 3% Down?

Yes. First-time homebuyers can qualify for a conventional loan with as little as 3% down if they meet other eligibility requirements. For repeat homebuyers, the minimum down payment is typically 5%, although most conventional loans fall within the 5%-20% range.

Do Conventional Loans Require 20% Down?

No. Most borrowers can qualify with a lower down payment. However, in some cases – such as a weaker overall borrower profile or when purchasing an investment property – a higher down payment of 15%-25% may be required.

What DTI Ratio is Allowed for a Conventional Loan?

Conventional loan DTI limits can vary by lender, but generally, DTIs up to 43%-45% are acceptable. With strong compensating factors, DTIs up to 50% might be allowed.

Do Conventional Loans Require PMI?

When putting less than 20% down, conventional loan PMI is required. When the borrower reaches 20%, PMI can be cancelled. When equity hits 22%, PMI is automatically canceled.

Are Conventional Loans Harder to Qualify for Than FHA Loans?

Conventional loans typically require higher credit scores and stronger overall financial profiles, so qualifying can be more challenging than FHA loans. However, conventional loans often offer more flexible terms and, in some cases, better long-term pricing.

What are the 2026 Conforming Loan Limits?

In most counties, the limit for one-unit properties is $832,750, while in high-cost areas, the limit increases to $1,249,125.

Can First-Time Homebuyers Qualify for Conventional Loans?

Yes. Conventional loans can be a great option for first-time homebuyers, as they offer low down payment options, favorable pricing, and flexible terms.

What Income Documents are Usually Needed for a Conventional Loan?

Lenders typically accept a wide range of income documentation, including pay stubs, W-2 forms, or VOEs for employed borrowers, and tax returns or bank statements for business owners or self-employed individuals.

Is a Jumbo Loan Still Considered Conventional?

Yes. However, jumbo loans are non-conforming and therefore may come with stricter requirements and higher pricing.

Fill out the short form and get a call from our AE

Struggling with a loan scenario?

Get a solution in 30 minutes!

Key Takeaways

- Conventional loan requirements in 2026 can vary due to lender overlays, but typically include a minimum credit score of 620, a DTI up to 43%-45%, and a down payment starting at 3% for first-time homebuyers and 5% for repeat buyers.

- Qualification does not depend on a single factor. Instead, underwriting evaluates the borrower’s overall profile to determine their ability to afford a mortgage.

- Conventional loans offer greater term flexibility and can be more affordable in the long run than government loans.

Conclusion

The Conventional Loan program page is designed to help you find the right mortgage solution for your client’s needs. If you want our expert support in matching the borrower with the right program, submit a scenario request and one of our managers will contact you within 30 minutes with a tailored solution.

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again