Post content:

Before your next borrower locks a rate, check their mortgage credit score. It may be costing them more than they think.

Having a FICO score below 760 on a $400,000 loan can mean paying $20,000 or more in additional interest before the loan is paid off. In high-cost states, that figure exceeds $40,000. It is only a fraction of a percent in APR, but most borrowers don’t realize it until they see the numbers.

AD Mortgage conducted a study analyzing how credit score affects mortgage costs across all 50 U.S. states and the District of Columbia. The findings provide brokers a concrete and data-backed way to explain credit impact to clients.

About the Study

AD Mortgage took the average credit score in each state and calculated:

- how much a borrower would save on a 30-year mortgage by improving that score to 760

- how long that improvement would realistically take

The table below shows the data sources behind those calculations.

Parameters Sources of Information Starting scores Average state-level FICO scores from Experian (September 2024) Target score 760, based on myFICO Loan Savings Calculator tiers that identify 760+ as qualifying for the best available rates Improvement rate A modeled pace of 20 FICO points per year. It is a realistic benchmark for borrowers actively working on their credit Home prices Zillow Home Value Index median values by state (December 2025) Loan structure 30-year fixed-rate mortgage with a 15% down payment, based on 2025 NAR data APR by credit tier Sourced from the myFICO Loan Savings Calculator as of February 4, 2026 Income data Median household income by state from the U.S. Census Bureau's American Community Survey

The savings shown reflects total interest saved over 30 years. Real results may differ depending on the borrower profile and market conditions.

How Does Credit Score Affect Your Mortgage?

A higher credit score usually means a lower mortgage rate, which results in less interest paid over the life of the loan. Beyond the interest rate, a higher score opens doors to larger loans and lower down payments. It also helps your borrower qualify for a broader range of mortgage programs in general.

Most lenders require a minimum score of around 620 for conventional home loans. For Non-QM programs, FICO score minimum requirements typically range between 620 and 700.

What AD Mortgage’s Study Found

Here are three key takeaways.

Borrowers Can Save Tens of Thousands Over 30 Years

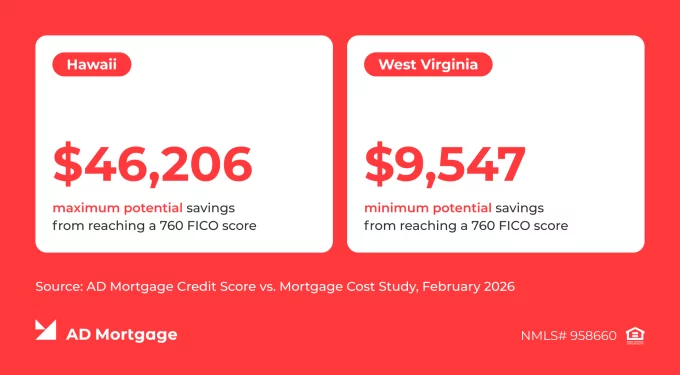

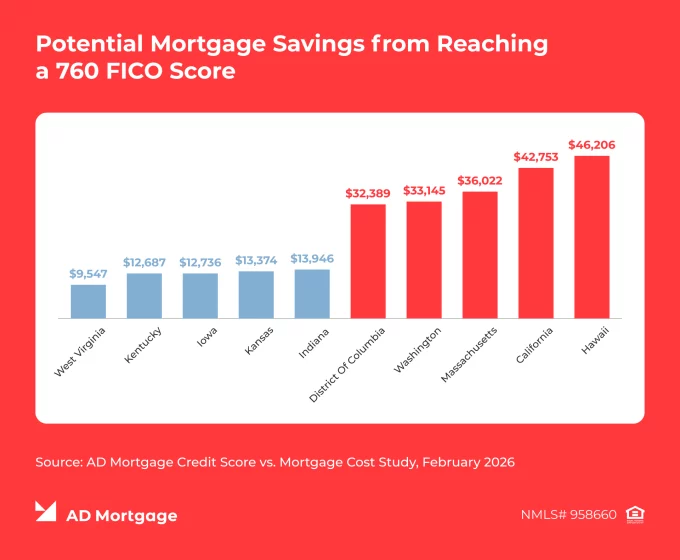

The study maps mortgage savings by credit score across all 50 states. Improving a credit score from the state average to 760 can save a borrower between $9,547 and $46,206 in total mortgage interest. Actual savings depend on local home prices and the starting credit point.

Hawaii leads with the highest potential savings at $46,206, driven by the state’s high median home values. California follows at $42,753, and Massachusetts at $36,022. Across most states, the typical savings range falls between $20,000 and $30,000. This figure resonates with borrowers when it is presented in dollar terms rather than rate percentages.

At the lower end, West Virginia borrowers stand to save $9,547, with Kentucky ($12,687) and Iowa ($12,736) also among the lowest. Largely, that is because more affordable home prices mean smaller loan amounts. Eventually, a smaller loan leaves less room for rate differences to add up over 30 years.

When speaking with clients, framing this as a concrete dollar amount changes how seriously they take the credit conversation.

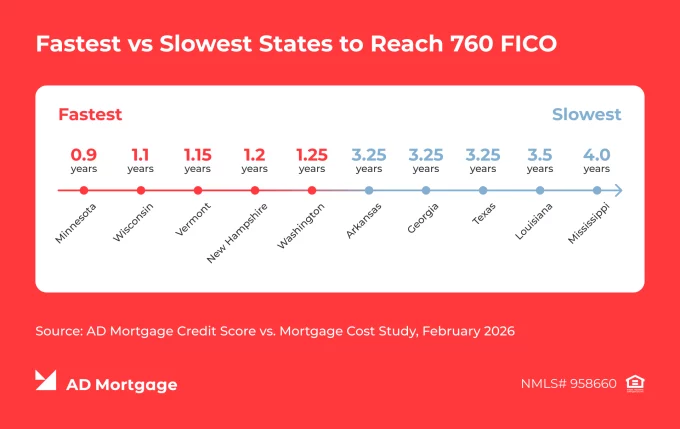

Reaching a 760 Score Can Take Under a Year, or Over Four

How long it takes to improve a credit score depends on where a borrower is starting from. The study assumes borrowers are making steady progress, gaining around 20 FICO points a year.

Borrowers in Minnesota have the shortest timeline: just 0.9 years (~10 months), thanks to an already high average state FICO of 742. Wisconsin (1.1 years, avg. FICO 738) and Vermont (1.15 years, avg. FICO 737) are close behind. For borrowers in these states, qualifying for prime rates is a short-term goal.

At the other end, Mississippi requires an estimated 4 years (avg. FICO 680), Louisiana 3.5 years (avg. FICO 690), and Georgia, Texas, and Arkansas each around 3.25 years (avg. FICO 695). Most states fall somewhere in the 1.5 to 3-year range, including Florida at 2.65 years.

This is useful context when deciding whether to encourage a borrower to wait or move forward now.

The Best Payoff is Not Always Where Savings Look Biggest

With a 760 credit score, mortgage costs can be tens of thousands of dollars lower. And total dollar savings are useful, but they do not tell the whole story. A $46,000 saving in Hawaii and a $17,000 saving in Mississippi are hard to compare directly because the cost of living and income levels are different.

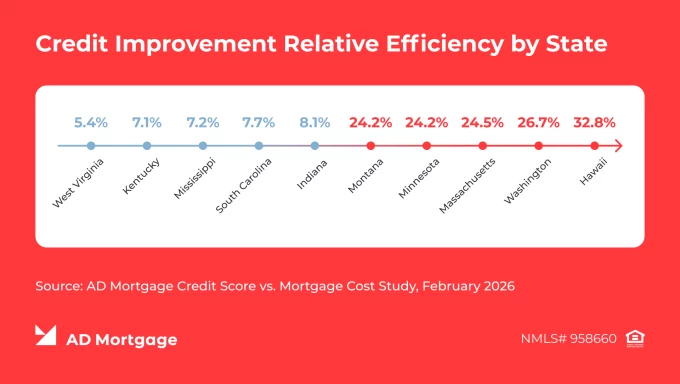

To make the comparison more meaningful, the study also looks at how much a borrower saves each year from improving their credit. It is expressed as a percentage of median household income in that state. This gives a clearer picture of where credit improvement has the most real-world financial impact.

Hawaii still leads at 32.8%, meaning the annual benefit of reaching 760 is equivalent to nearly a third of the median household income in the state. Washington (26.7%) and Massachusetts (24.5%) follow. What these three states also have in common (except for large savings) is relatively short improvement timelines. This means that the total savings are spread over fewer years, making the annual payoff higher.

West Virginia sits at the bottom at 5.4%. This is the result of a combination of lower home prices (smaller loan amounts) and a 2.9-year improvement timeline.

Quick Summary: Mortgage Savings by State from Improving Credit Score

The highlights below capture mortgage interest savings by state, showing where the opportunity is most significant or more limited.

- Highest total savings (30-year interest reduction): Hawaii ($46,206), California ($42,753), Massachusetts ($36,022)

- Highest savings relative to annual income: Hawaii (45.9% of median income), California (42.7%), Georgia (37.2%)

- Highest annual efficiency (savings per year as % of income): Hawaii (32.8%), Washington (26.7%), Massachusetts (24.5%)

- Lowest annual efficiency: West Virginia (5.4%), Kentucky (7.1%), Mississippi (7.2%)

- States with the fastest path to 760: Minnesota (0.9 years), Wisconsin (1.1 years), Vermont (1.15 years)

Researchers also looked at savings not in raw dollars but as a share of the loan amount. In seven states, borrowers with poor credit end up overpaying by more than 10.7% of their loan principal over the life of the mortgage. On a $200,000 loan, that’s over $20,000 lost purely due to a low credit score. These states are Alabama, Arkansas, Georgia, Louisiana, Mississippi, Oklahoma, and Texas.

An important note is that these are states with below-average home prices, yet they carry higher baseline interest rates (6.91%). You might expect cheaper housing to mean lower financial risk but the data suggests the opposite. In these markets, the relative penalty for having suboptimal credit is disproportionately large. In other words, the less expensive the home, the harder a weak credit score hits your borrower’s wallet in percentage terms.

For borrowers in these regions, improving a credit score before applying for a mortgage is arguably more impactful here than anywhere else in the country.

Why a Higher Credit Score Can Lower Mortgage Cost

Lenders use credit scores as one of the primary signals of borrower risk. A borrower with a stronger score is statistically less likely to default. Lenders reflect that in the APR they offer. The higher the perceived risk, the higher the rate.

At first glance, that rate difference may look small. But even a 0.28-point gap in APR adds up to over $20,000 in additional interest on a $400,000 loan over 30 years. The bigger the loan, the bigger the long-term impact. That is why credit score matters most in high-cost markets where loan amounts are larger.

Understanding the link between credit score and mortgage rates helps borrowers see why even a small score improvement matters. And when you explain this in dollar terms rather than rate percentages, the conversation becomes more effective.

Is It Worth Improving Credit Score Before Getting a Mortgage?

The answer here largely depends on the borrower, their needs, and their financial goals. However, the study provides brokers with the data to work through that question.

The case for waiting is strongest when the borrower is within 20 points of 760 and can realistically get there in 1–2 years. As a broker, you can guide borrowers on how to improve a credit score before buying a house.

Also, it is often worth the wait if potential savings are large, relative to their income, and there is no urgency to buy now. Good examples are Washington, Massachusetts, and Colorado, because borrowers there tend to improve faster and save more.

The case for buying now makes more sense when the borrower is 3+ years away from 760 and has already done everything they can to move the score faster. For instance, paid down balances and fixed report errors. At that point, waiting becomes a longer commitment with no guarantee of a faster outcome.

How Mortgage Professionals Can Use This Data

Max Slyusarchuk, CEO of AD Mortgage, explains: “A difference of 20 or 30 FICO points may seem small, but over the life of a mortgage, it can determine whether a borrower pays an extra $20,000 in unnecessary interest. Our goal with this report is to give lenders, brokers, and consumers actionable insight into how credit impacts true buying power.”

Here are some examples of how you as a broker can use AD Mortgage’s data in real client conversations.

- Convert score tiers into dollar amounts. Brokers who can break down mortgage costs by credit score and translate their FICO into a specific dollar figure give their clients a concrete reason to act.

- Stay in touch with borrowers who are not ready yet. Not every prospect is ready to apply for a mortgage immediately. Borrowers who are 1.5 – 2 years from 760 are worth staying in touch with. This data gives you a concrete reason to do that, with a specific timeline and a dollar figure to reference. Using a CRM like AD Mortgage’s free LEADer CRM will help you keep track of these potential buyers.

- Set realistic expectations around timing. When a borrower asks how long it will take to reach 760, this data illustrates a reasonable starting point for that conversation. For instance, a borrower in Florida at the state average of 707 is looking at roughly two and a half years of consistent work on their credit to get there.

Also, the data can either make the case for postponing the application, or show a borrower why waiting three or more years may not be worth it for their specific situation.

AD Mortgage combines publicly available datasets (including Experian FICO averages, Zillow home value data, myFICO APR tiers, and U.S. Census income figures) with modeled mortgage scenarios to produce state-level estimates. Mortgage lenders use credit scores to assess borrower risk. Higher scores usually qualify for lower APRs, bigger loan amounts, lower down payments, and a wider variety of available loan programs. According to AD Mortgage’s study, improving to a 760 FICO score can save a borrower between $9,547 and $46,206 in total mortgage interest over 30 years, depending on the state and loan size. Most borrowers fall in the $20,000 – $30,000 range. Yes, a FICO score of 760 or above usually qualifies borrowers for the best available mortgage rates. This threshold is used by the myFICO Loan Savings Calculator to define the top credit tier for mortgage pricing. AD Mortgage’s study models a 20-point annual improvement pace for borrowers actively working on their credit. At that rate, most states require 1.5 to 3 years to reach 760 from the state average. It depends on how far the borrower is from 760 and the potential savings in their state. In states where the improvement timeline is short and savings are high relative to income, waiting can make financial sense. In other cases, moving forward now and refinancing later may be a better path. A low credit score can affect whether a borrower qualifies at all, depending on the loan program. For borrowers who do qualify, the score also directly impacts the APR they receive, and therefore the total cost of the loan. The variation is driven by home prices and starting credit scores. Higher home prices mean larger loan amounts, which increases the impact of even a small rate difference. Also, in some states, borrowers start with lower average credit scores, which means higher initial rates and a longer path to reach 760. It makes the cost of waiting higher.

FAQ: How Credit Score Affects Mortgage

How does AD Mortgage conduct their studies?

How much does credit score affect mortgage rates?

How much can a higher credit score save on a mortgage?

Is 760 a good credit score for a mortgage?

How long does it take to improve your credit score?

Should you wait until your credit score improves before buying a home?

Does your credit score affect mortgage approval or just the rate?

Why do savings vary so much by state?

Conclusion

The FICO score determines how much your borrowers will pay over the life of the loan. The difference between an average state score and 760 can mean tens of thousands in additional interest, depending on where that borrower lives.

AD Mortgage’s state-by-state analysis puts concrete numbers behind that gap. For any credit score, mortgage savings can be estimated and shown to the borrower in dollars. With the help of our study, brokers are able to have credit conversations earlier and with data to back it up.

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again