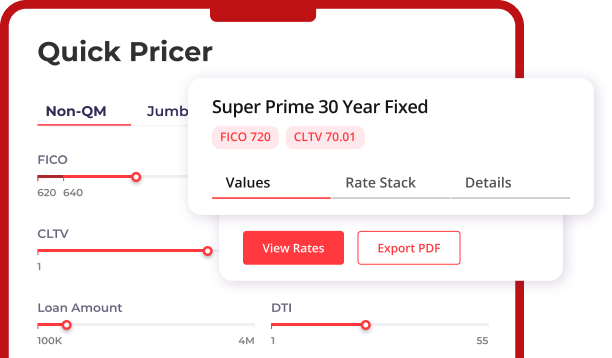

Available on Prime, Super Prime, and Apex Prime

An Asset Utilization loan lets borrowers qualify using liquid assets instead of employment income. No tax returns, pay stubs, or job verification required, and assets never need to be liquidated or pledged. AD Mortgage calculates qualifying income by dividing eligible assets by just 60 months — so $1.2 million in assets equals $20,000 in monthly qualifying income (many lenders divide by 84, yielding far less). Ideal for retirees, self-employed borrowers, entrepreneurs, high-net-worth individuals, and anyone with strong assets but variable income. Loan amounts up to $5 million with FICO from 620.

Program features

Struggling with a loan scenario? Push the button and get a solution in 30 minutes!

Write to us, we will contact you within 30 minutes.

As fast as

24 hr

As fast as

24 hr

As fast as

48 hr