Grow your business with DSCR,

Bank Statement, ITIN, and more!

As one of the top Non-QM mortgage lenders, we empower brokers with competitive non-qualified mortgage programs designed to close deals faster

Close DSCR loans with fast turn times

A perfect fit for self-employed borrowers

Expand your mortgage portfolio for borrowers without an SSN

Qualify Foreign Nationals seeking investment properties with minimal documentation and fast closings

See ProgramsNon-QM loans are suitable for the self-employed, investors, and foreign nationals

Including your favorites: 12/24 Month Bank Statement loans and DSCR loans

Non-QM loans skip the strict credit, down payment, debt-to-income (DTI) ratio requirements

Investment properties, second homes, and even unique scenarios

We do — as the #1 Non-QM Lender ranked by Scotsman Guide

At A&D Mortgage we offer the fastest turnaround times in the mortgage industry

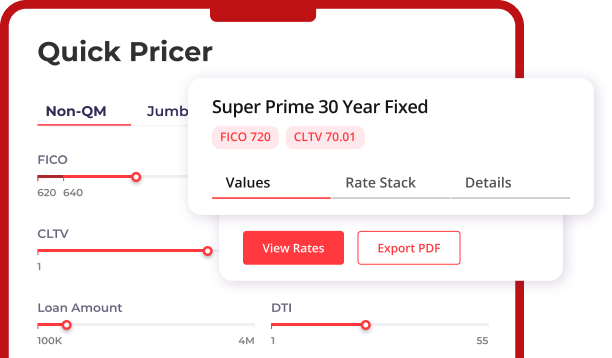

Easy to avoid with our AIM Partner Portal, providing a clear pipeline for every loan

“The demand for Non-QM products has surged,

particularly as more borrowers seek flexible options outside

conventional loans.

As the #1 Non-QM lender, we are proud

to offer diverse solutions

for borrowers who fall outside

traditional

qualification

standards.”

Leverage AIM — the Partner Portal with AI-powered features and tools for fast closings

Take advantage of all the features and tools to streamline your workflow

Partner with A&D Mortgage today and explore the benefits of non-QM lending with a team that understands your needs. From non-qualified mortgage solutions to tailored support, we’re here to help you succeed in the non-QM space

Tailored Non-QM home loans

for self-employed, investors,

and unique financial profiles.

Streamlined process

with clear

Non-QM loan requirements.

Dedicated team to guide you

through every step of Non-QM lending.

Innovations that keep you ahead

in Non-QM mortgages.

What is a Non-QM loan?

A Non-QM loan (also known as a non-qualified mortgage) is a type of home loan designed for those borrowers who can’t qualify for traditional mortgages. It is suitable for:

Non-QM products offer flexibility. They often come into play and help secure needed financing when Conventional options just don’t work.

What types of Non-QM loans are there?

Non-QM loans come in many types to suit a range of unique cases.

Self-employed people often pick Bank Statement loan first. Lenders look at 12/24 months of bank records to check the borrower’s income, instead of W-2s or pay stubs.

Real estate investors find DSCR loans perfect. These home loans focus on how much rent a borrower’s property brings in, not their personal earnings.

People who need a bigger loan often go for Jumbo loans. These apply to pricey properties that go beyond the usual Conventional loan caps. People with substantial assets, like savings or investments, can opt for asset-based loans. They can use these assets to qualify instead of providing standard income documentation.

AD Mortgage offers all these Non-QM loan types, and the choice is always yours to decide which loan type you would prefer.

Who offers Non-QM loans?

Typically, specialized non-qualified mortgage lenders like AD Mortgage offer Non-QM loans. We understand that not everyone has a steady income stream and traditional docs. That’s why we offer flexible solutions for different financial situations.

What about taxes and Non-QM loans?

Taxes for Non-QM loans depend on how a borrower uses the loan. If they are buying an investment property, their interest payments might be tax deductible. It is a good idea to consult a tax professional about your specific case.

What's the process for getting a Non-QM loan?

The process of getting a Non-QM loan is straightforward. Usually, it consists of these 5 steps:

What do I need to qualify for a Non-QM loan?

Non-QM loan requirements vary from lender to lender. Here is what AD Mortgage provides:

Credit score: At least 620

Combined Loan-To-Value (CLTV): up to 90

Proof of income: Bank statements, tax returns, or proof of rental

income

Down payment: From 10%

Debt-to-income ratio (DTI): Depends on the type of loan

How to apply for a Non-QM loan?

At AD Mortgage we created Artificial Intelligence in Mortgage (AIM) to streamline the Non-QM loan process, from submitting the application to closing the loan. AIM is our Partner Portal that helps partners grow their businesses. See the key features and tools of AIM:

Not a partner yet? Just fill in this form

Already have an account? Log in now

Looking for the basic steps to apply for a loan? Here they are:

1. Finding a lender

It’s a good idea to start by looking for reliable Non-QM lenders, like AD Mortgage, that understand and work with different financial situations.

2. Gathering documents

Next, it’s necessary to prepare documents, such as bank or investment account statements and tax returns, to show financial stability.

3. Submitting the application

Then, a borrower should work on their application with their chosen lender.

4. Getting approved

Once approved, a borrower can move forward confidently and close on their loan.

Why pick AD Mortgage for Non-QM loans?

At AD Mortgage, we get that everyone has a different story. Not everyone fits into the usual loan criteria. We’re all about giving Non-QM borrowers flexibility. Whether they’re a self-employed individual, a property investor, or have a unique situation, we can help. We offer good rates, fast approvals, and several Non-QM options to keep things simple.

Does AD Mortgage offer specials on Non-QM loans?

Of course we do! We run promotions for both non QM and conventional loans on a regular basis. Check out our website to stay updated on our current promotions and special offers.

How to start working with AD Mortgage?

It is easy – just fill out the broker package. Whenever you are ready, go to Broker Package page and submit the form.

Are Jumbo loans Non-QM?

Jumbo loans can be Non-QM if they go over the usual loan limits or do not stick to the regular rules. These kinds of loans are suitable for more expensive homes. They work well for borrowers with good financials who want more flexibility than typical loans offer.

The borrower wants to refinance a Non-QM loan. Is it possible?

It is possible. If your client wants a better rate, lower monthly payments, or to tap into their home equity, refinancing a Non-QM loan is a smart choice. AD Mortgage provides such an option. If a borrower’s financial situation has improved since the original loan, it’s worth checking out.

I want to learn more about the risks of using Non-QM loans

The transparency in everything is our priority, so let us dive deeper into some of the risks associated with using Non-QM loans:

The risk of financial overextension. Non-QM borrowers may have to spend more funds on interest rates, fees, and down payments.

The risk of losing the home. The borrower may face foreclosure if they cannot keep up with the payments.

Who are Non-QM loans for?

Non-QM loans are for people who don’t fit into the usual mortgage rules.

This includes:

What payment options are there for Non-QM loans?

Flexibility matters! Borrowers can choose from various payment plans.

They can go for fixed rates, adjustable rates, or interest-only payments. We will help borrowers find what works best for their budget.

I want to compare Non-QM loans to conventional loans, how are they different?

They are completely different from each other. The most crucial difference is that Conventional loans are governed by Fannie Mae and Freddie Mac guidelines. It means that Non-QM borrowers have to meet all the criteria to qualify. Instead of Conventional loans, Non-QM loans are more flexible and suitable for those who don’t follow traditional loan paths, e.g., self-employed or investors.

Tell me about the benefits. What are they for Non-QM loans?

Here is why Non-QM loans stand out:

1. Higher loan amounts

Non-QM loans include Jumbo options, making it possible to finance larger properties. At AD Mortgage we have a special program called Prime Jumbo, with loan amounts up to $3.5 million.

2. Flexibility

Multiple options to qualify. Not only can borrowers rely on traditional pay stubs, but they can also use bank statements, rental income, or even assets.

3. Accessibility

Have your clients already applied for a traditional loan but been turned down because they did not meet the requirements? Non-QM loans can be the perfect solution for their scenarios.

As you can see, Non-QM products can accommodate borrowers with specific needs.

How does equity work in Non-QM loans?

If you have equity in your home or investment property, you can use it to get cash. This money can help you:

Do Non-QM loans protect borrowers, and if so, how?

It depends on the lender. Basically, Non-QM loans don’t have the same protection as other mortgages, like Consumer Financial Protection Bureau (CFPB) for Conventional loans. But Non-QM lenders like AD Mortgage always keep things clear and fair. We have 20 years of experience with more than 8,500 partners. Before you commit to a loan, it is crucial to fully understand all terms, conditions, and risks. Make sure everything is clear to you.

I want to buy a second home or investment property. Can I get a Non-QM loan for these purposes?

Yes, you can. Non-QM loans are perfect for buying a second home or an investment property. Options like DSCR loans help real estate investors qualify based on rental income.

WHAT SKILLS DRIVE YOUR SUCCESS? TAKE A SURVEY & GET 300 LOYALTY POINTS