Military members might be interested in using a VA loan more than once. The reasons for that might include moving due to Permanent Change of Station (PCS) orders or a growing family. These loans are especially appealing in 2025 because property prices are high. Unlike other programs, a VA mortgage typically requires no down payment and offers better terms.

But can a veteran apply for a VA loan if they have already used one before? In this article, we provide you with a short clear answer, quick examples, and broker steps.

The Short Answer: How Many Times Can You Use a VA Loan?

VA loans can be used more than once. The ability to get a loan depends on the veteran’s eligibility and remaining entitlement. Therefore, in some cases, it is possible to hold two VA loans at the same time – for example, when buying a new primary residence without selling the previous one.

There are no limits on how many times a person can get a VA loan, as long as they qualify. The same rules apply to each new loan:

- A VA loan can be used only for funding a primary residence. No investment properties or secondary homes are allowed. The borrower must move into the new residence within 60 days after closing.

- The borrower must have a Certificate of Eligibility (COE), showing the size of their entitlement.

Entitlement 101: Full, Partial, and Bonus

When a mortgage lender provides mortgages, they want to ensure that the money will be repaid with interest. Therefore, a lender needs guarantees that the borrower will be able to make payments on time.

What Entitlement Guarantees

VA entitlement is the amount the Department of Veterans Affairs (VA) promises to repay the lender in case the borrower defaults. There are several types of entitlement:

- Full entitlement. Eligible borrowers who have never used a VA loan, or who have fully repaid a previous VA loan and had their entitlement restored, are entitled to a full VA benefit. This means that the VA guarantees up to 25% of the loan amount, regardless of its size and without county limits.

- Partial entitlement. When a borrower already has a VA loan, part of their entitlement is tied to that property. In such cases, applying for a second loan is allowed. Depending on the size of the remaining entitlement, the borrower might need to make a down payment to cover the difference.

- Bonus (second-tier) entitlement. This applies to larger loans and allows the VA to guarantee up to 25% of the loan amount for borrowers with full entitlement. For those with partial entitlement, the size of guarantee is calculated individually based on remaining entitlement and county limits.

By providing these guarantees, the VA shares the risk with the lender, but the same underwriting rules still apply. The lender checks the borrower’s income, credit history, debt-to-income ratio, and other factors to evaluate their ability to repay. Therefore, even though the loan is backed by the VA, it does not compromise underwriting requirements.

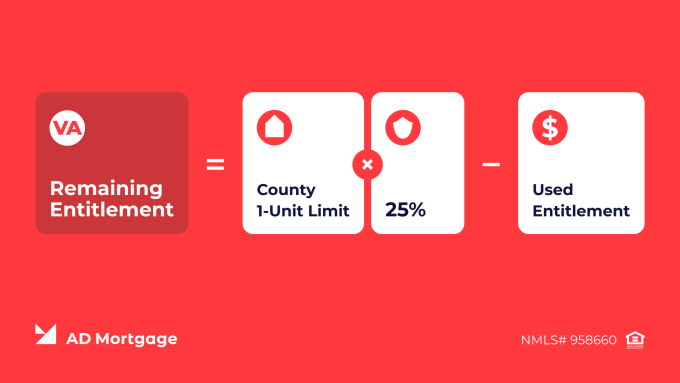

Calculating Remaining Bonus Entitlement: Quick Math

If the borrower has already used some entitlement before, lenders need to calculate remaining entitlement, showing how much VA guarantees for the new loan.

In that case, this simple formula is used:

This 3-step plan will help you better understand how this formula works in practice.

- Check the county 1-unit limit which is annually adjusted by the FHFA. In 2025, the limit is $806,500for most states.

- Check entitlement already used, which can be found in the COE. In our example it is $50,000.

- Put the numbers into the formula:

Remaining Entitlement = ($806,500 * 25%) – $50,000 = $151,625

This means that if the borrower applies for a $600,000 loan, the remaining entitlement is short by $650,000 * 25% – $151,625 = $10,875. The borrower needs to make a down payment of this amount to meet the VA requirement.

Broker Tip: Pull the COE early to quickly determine whether a down payment will be required.

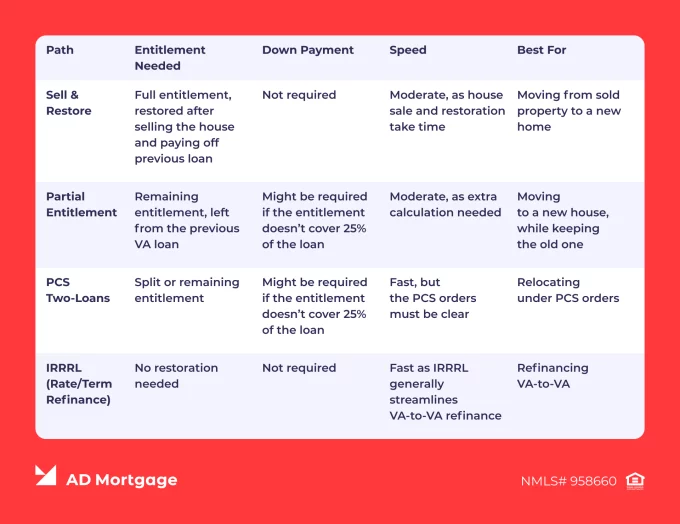

Four Common Reuse Scenarios

There are four common situations in which eligible veterans can reuse VA loans. Below, we give a brief description of these scenarios and the actions brokers need to take.

Sell with Full Entitlement Restored

If the borrower wants to sell their previous VA-financed property and restore the full entitlement, then they likely won’t need to make a down payment or face county limits.

Broker Steps:

- Check that the previous loan is paid off

- Request the VA restore the entitlement

- Verify eligibility and underwriting criteria for a new loan

- Proceed with the new VA loan without a down payment

Keep Current Home + Buy Again with Remaining/Partial Entitlement

The borrower might want to purchase a new house for living, while keeping their current property. In this case, a down payment might be needed if the remaining requirement doesn’t cover 25% of the loan amount.

Broker Steps:

- Calculate the remaining entitlement using the formula above

- Determine whether a down payment is needed

- Verify eligibility and underwriting criteria for the new loan

- Proceed with the new VA loan, a down payment might be required

Two VA Loans at Once (PCS/New Primary)

If the veteran has purchased a house and then must PCS to a new location, the new loan might overlap the prior one. In such cases, occupancy timing is important, as typically the buyer must move into the new house within 12 months, depending on the lender’s requirements.

Broker Steps:

- Confirm the overlap is due to a valid reason

- Calculate the remaining entitlement

- Check the occupancy window with lender’s requirements

- Verify eligibility and underwriting criteria for a new loan

- Proceed with the new VA loan, a down payment might be required

Restore Without Selling

If the prior loan is paid off but the property is not sold, the borrower might request a one-time restoration to use the entitlement again.

Broker Steps:

- Check that the previous loan is paid off

- Request a one-time restoration from the VA

- Check potential loan limits and lender restrictions for restoration without selling

- Verify eligibility and underwriting criteria for a new loan

- Proceed with the new VA loan, a down payment might be required

Comparison Table: Reuse Paths

In case the borrower is not sure what scenario is best for their situation, this comparison table can be helpful. Note that it includes typical terms for each path, which might differ in individual cases. For exact loan conditions, contact the lender.

A&D Mortgage VA Options for Your Next Deal

VA loans offer a significant opportunity for military members to purchase houses at affordable costs. A&D Mortgage provides two programs for VA loans, follow the links to learn more about their conditions.

- VA Standard: loans up to $2 million without down payment or PMI, minimum FICO score of 580, up to 100% CLTV, with temporary buydowns available.

- VA IRRRL: Streamlined refinance of loans up to $1.5 million to lower rate and reduce payment.

Check the entitlement and pricing on our AIM Partner Portal. We can also assist you in retrieving the COE.

Broker Tip: Use a temporary buydown to lower your client’s monthly payments in the first few years of the loan. The cost can be covered by seller credits within VA concession limits to help the borrower preserve cash at closing.

Quick Broker Flow: from COE to Clear-to-Close

- Pull the COE and check the remaining entitlement.

- Check the 25% guarantee and apply the county limit formula to see whether a down payment is required.

- Choose the reuse path: Sell & Restore, Partial Entitlement, PCS Overlap, or IRRRL for a VA-to-VA refinance.

- Price A&D VA product, structure seller credits, and confirm the funding fee status.

- Order VA appraisal if applicable, verify occupancy timeline, and submit the file for underwriting.

FAQ for Using a VA Loan More Than Once

How Many Times Can You Use a VA Loan?

Borrowers can use VA loans multiple times, as long as they are eligible and have enough remaining entitlement.

Can You Hold Two VA Loans at the Same Time?

Holding two VA loans is possible if the borrower has enough remaining entitlement and the new house is their primary residence. For example, this would be allowed due to a PCS move.

How do I Restore Entitlement?

To restore the entitlement, the borrower needs to sell the property, pay off the loan, and pull a new COE, or use a one-time restoration option. The less common way is to let another eligible borrower assume the loan.

What if I Used Entitlement and Want $0 Down Again?

To use the VA benefit and get a loan without a down payment, the borrower must restore the entitlement. Then, full entitlement will allow $0 down, but partial entitlement might require a down payment.

Does the County Loan Limit Affect my Remaining Entitlement?

Yes, the county limits outline the VA guarantee and therefore affect the required down payment.

Key Takeaways

- There are no lifetime caps on usage of VA benefits. Loan terms depend on the borrower’s entitlement.

- For those who already have a VA loan, the Sell & Restore option is the quickest way to get $0 down again.

- PCS overlap can allow simultaneous VA loans with proper occupancy.

- Running the 25% guarantee test early helps avoid surprise down payments.

- A&D’s VA lineup supports high balances and flexible credit – route your next VA file here.

Conclusion

VA loans are a great way for military members to purchase a primary residence without a down payment or PMI. Veterans can use this benefit multiple times, provided they meet specific criteria.

Brokers need to support their clients on this journey and A&D Mortgage is here to help. Follow the link to quickly check the COE and calculate an entitlement.

")