Post content:

")

Non-QM loans are a great opportunity for brokers, as they help serve a wider range of clients and often offer higher compensation for MLOs. However, there are Non-QM-specific features that are crucial to understand in order to keep files moving smoothly. Here are some of the key reasons brokers lose Non-QM deals and some advice on how to avoid them. Read on to better understand the challenges and solutions – and ultimately close more Non-QM deals.

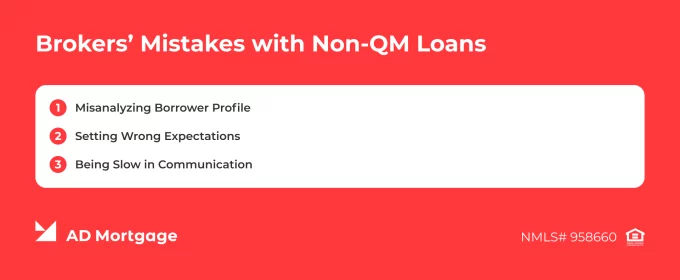

What Mistakes Do Brokers Make with Non-QM Loans?

We have analyzed how brokers work with Non-QM mortgages and identified the three most common oversights.

Misanalyzing Borrower Profile

Brokers should remember that conventional underwriting rules do not apply to Non-QM mortgages. Unlike QM loans that rely on automated underwriting systems, Non-QM loans require a manual review of the full borrower’s profile.

Applying QM logic to Non-QM scenarios may lead to delays during underwriting or the need to restructure the loan mid-process.

To select the right mortgage product, brokers must pre-qualify the borrower profile and evaluate the file holistically, including income documentation, cash flow stability, reserves, compensating factors, and other factors.

Understanding the borrower’s financial situation is crucial before matching them with the specific Non-QM loan program. At this stage, the broker should also check how the chosen solution benefits the borrower and whether it supports their long-term strategy.

Setting Wrong Expectations

Many borrowers are unfamiliar with Non-QM guidelines and might be frustrated by ‘surprises’ like prepayment penalties or the end of an interest-only period. When these features are not explained upfront, it results in client dissatisfaction or post-closing complaints.

To prevent this, brokers must proactively educate their clients. The central message to communicate to borrowers is that Non-QM loans are not rate-driven – instead, they are solution-driven. Non-QM loans are designed to address income complexity and documentation challenges and offer greater qualification flexibility, not just securing the lowest rate available.

Additionally, brokers must outline specifications of the Non-QM process, including more complex underwriting, higher risk-based pricing, and extended timelines.

Setting transparent expectations protects all parties and supports long-term relationships between the broker and the client.

As Polygon Research shows below, Non-QM and traditional loan amounts are about the same, but the income potential for Non-QM is better both for the initial loan and future restructuring. However, there is a significant difference between average monthly payments – $2,304 for traditional loans and $3,179 for Non-QM loans – and brokers should prepare their clients for potentially higher payments.

Being Slow in Communication

Closing Non-QM deals takes between 30 and 60 days on average, which is longer than conventional mortgages. In addition, due to more complex financial situations, borrowers are time-sensitive, so every day counts.

Therefore, brokers should pay extra attention to structuring the loan properly in advance, including:

- Calculating income and reviewing documentation

- Evaluating LTV and adjusting the down payment size

- Choosing the reserves strategy

- Comparing Non-QM programs terms and rules

Loan structure has a direct impact on both approval and pricing. Brokers should approach this step strategically, fully understanding the borrower’s goals and profile.

Moreover, keep in mind that the underwriter might require additional documentation. To avoid delays and client frustration, brokers should be proactive in communicating with borrowers and lenders and respond promptly to arising questions.

How Can Brokers Resolve Non-QM Issues and Close More Loans?

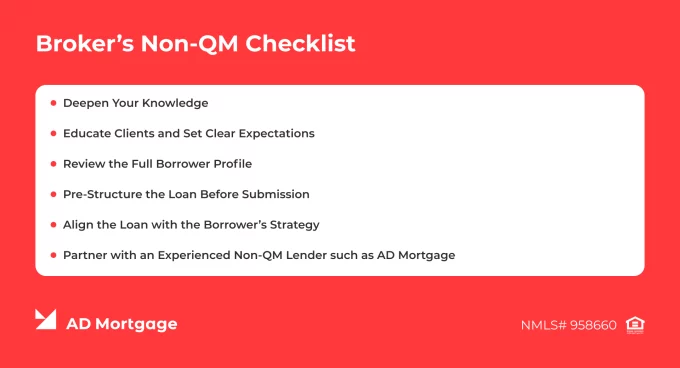

Understanding common mistakes is the first step in avoiding them. However, there are additional tips that can help you streamline the process and make it more efficient for all parties.

Educate Yourself – And Your Clients

For brokers to be able to guide borrowers efficiently, having a basic understanding of Non-QM mortgage programs is not enough. Deeper knowledge of terms and nuances helps save time and navigate the process without errors.

ADwise, a free 24/7 AI guideline assistant by AD Mortgage, quickly provides answers when you want to know more about property and loan requirements, lock policies, regulations, borrower eligibility, and other issues.

Apart from learning the information about Non-QM loans, it is also crucial to share it with your clients. Educate them about pricing, timeline, and requirements, and discuss how the mortgage solution aligns with their financial strategy. Clearly documented borrower expectations – this is what helps you avoid client dissatisfaction and complaints.

Pre-Structure the Loan

Carefully review the full borrower profile before locking the rate and submitting the file. Identify strong features and potential red flags internally and then structure the loan strategically, supporting the borrower’s long-term wealth plans.

Additionally, make the file easy-to-read so that the underwriter – prepare a thorough letter of explanation, arrange papers logically, include a concise summary, and highlight compensating factors clearly. These small touches make the underwriter’s work easier and show that you care.

Think Strategically

Non-QM loans are not rate-driven products, and simply chasing the lowest rate rarely delivers long-term value. Instead, brokers should structure Non-QM financing as part of the borrower’s broader financial plan.

Often, Non-QM loans serve as a transitional solution, with borrowers planning to refinance once their credit profile or documentation improves. Brokers should assist them in creating a clear exit strategy. This approach prevents draining all reserves for reduced rates right now and preserves the liquidity for future financial flexibility.

Partner with Experienced Lender

The lender is not merely a funding source, they are your core partner. Strong lenders guide brokers through nuances of Non-QM solutions, elevating their expertise and avoiding delays. Brokers and lenders are on one team, aiming to close clean files as fast as possible, helping those who can afford homeownership to fulfill their dreams. Therefore, choosing the right partner lender is crucial.

AD Mortgage is a top Non-QM U.S. wholesale mortgage lender that has over 20 years of experience in the mortgage industry. We offer flexible mortgage solutions, streamlined processes, and 24/7 partner support. Become a Partner today: Broker Package | AD Mortgage

Conclusion

Non-QM loans, compared to traditional lending, are more flexible and allow nonstandard profiles to qualify. Still, they require financial stability and the ability to repay the loan and include a full underwriting process.

Matching the borrower with the right Non-QM solution can be highly effective when it aligns with their long-term financial plan. Brokers should plan for future refinance opportunities and provide a clear exit strategy, ensuring the loan supports both immediate needs and future flexibility.

AD Mortgage provides a free tool, helping you quickly match your client profile with the mortgage program, tailored to their needs. Submit a loan scenario and the account executive will reach out to you within 30 minutes.

Choose among 20+ programs and get

Looking for a suitable loan program?

a detailed loan calculation

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again