Post content:

Borrowers often ask brokers why Non-QM loan rates are higher than conventional loans. The difference in pricing is driven by loan structure and market mechanics, not by the alternative underwriting process. This article explains how Non-QM loan rates are determined, helping brokers educate borrowers and set realistic expectations.

Why Are Non-QM Rates Higher?

Non-QM loan rates are typically higher because these loans fall outside standardized frameworks, rely on flexible underwriting, and are priced by private investors rather than government-backed channels.

The Short Answer Brokers Can Give Borrowers

Non-qualified mortgage rates are higher because of greater underwriting variability. While the borrower’s profile is rigorously verified, the process is more manual and requires specialized expertise, making it harder to standardize. Therefore, the risk of misjudging loan performance increases.

As a result, Non-QM loans often have higher servicing costs and limited liquidity in the secondary market. These factors influence interest rates, making them higher than conventional loans.

What Actually Drives Non-QM Loan Rates

While the short answer might be sufficient for the borrower, brokers should understand pricing in more detail. These are the five core reasons for higher Non-QM loan rates:

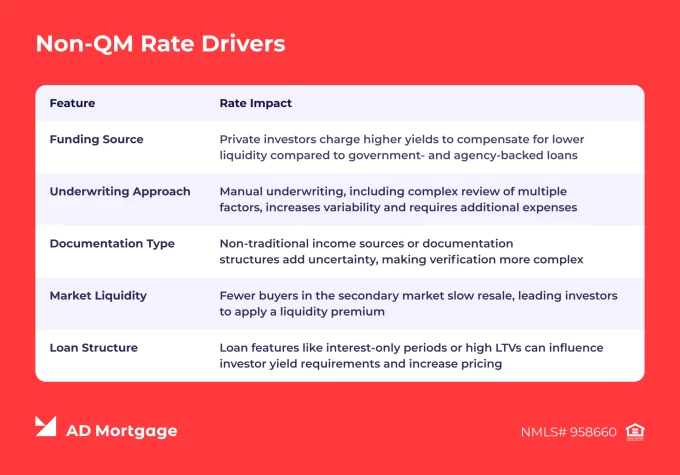

1. No Government or Agency Backing

Qualified Mortgages (QM) comply with Fannie Mae, Freddie Mac, FHA, or VA guidelines and have government or agency backing. Therefore, they are easier to sell in a secondary market, keeping investor demand high and interest rates lower.

Unlike QM loans, Non-QM solutions are funded by private investors and are not backed by the government or agencies. Because they are less liquid and harder to sell, investors require a higher yield to compensate for the additional risk, which results in higher interest rates for borrowers.

2. Flexible Underwriting Requires Manual Review

QM loans typically use automated underwriting, as they have standardized criteria that can be evaluated by the system, rather than a person. This approach reduces processing time and offers predictable outcomes for lenders and investors.

Non-QM loans evaluate the borrower’s profile as a whole, using more flexible underwriting guidelines. Experienced underwriters manually review alternative income documentation, compensating factors, and other features that cannot be processed automatically. The combination of time, expertise, and pricing risk leads to increased operational costs, which raises interest rates for borrowers.

3. Borrower Profiles Don’t Fit Standard Models

Non-QM loans are designed for borrowers that don’t fit into the strict QM criteria. They often have non-traditional income sources or documentation structures, which contributes to greater variability in loan performance.

To balance the uncertainty, investors increase the price slightly. This reflects the overall complexity of the situation, rather than additional risks.

4. Loan Structure Can Affect Pricing

Even if the borrower profile is strong, certain loan features can influence investor yield requirements and lead to pricing adjustments. While interest-only periods, high loan-to-value (LTV) ratios, or cash-out refinances do not automatically indicate higher risks, they still influence the interest rate.

5. Secondary Market Liquidity

Compared to government- or agency-backed loans, Non-QM loans are less liquid in the secondary market, which makes the resale less predictable for investors.

Because capital turnover is slower, investors apply a liquidity premium to loan pricing, contributing to higher interest rates.

Non-QM Rate Drivers at a Glance

If you need to briefly break down the main factors influencing interest rates, use the following table.

What Higher Rates Do Not Mean

Apart from the five reasons mentioned above that actually influence pricing, common misconceptions about Non-QM loans exist. Let’s address these myths.

- “Non-QM means no verification.” Non-QM loans do require full verification of the borrower’s profile to ensure that they are financially stable and have the capacity to maintain the mortgage.

- “Non-QM is subprime lending.” Subprime loans are often offered to high-risk borrowers with lower credit scores and poor history, who have a higher chance of default. Non-QM loans, on the other hand, involve thorough underwriting and require the borrower to demonstrate the Ability-to-Repay (ATR).

- “Non-QM is offered through temporary or unstable programs.” Trusted brokers offer transparent and reliable Non-QM solutions. With over 20 years of experience in the industry, AD Mortgage is recognized as a top Non-QM lender in the U.S.

When a Higher Rate Can Still Make Sense

For some borrowers or situations, Non-QM can be a beneficial tool. Brokers should quickly detect these scenarios to match their client with the right solution. So, in which cases do Non-QM loans work best?

- Borrower has a strong financial profile but does not meet strict requirements of traditional mortgages.

- Borrower needs a temporary solution, for example, before refinancing to QM loan.

- Borrower has a long-term planning mindset, and Non-QM loans can offer additional opportunities, such as investment flexibility and building equity.

Broker Explanation Box: Key Talking Points

- “Higher interest rates reflect greater flexibility, not lower standards. The underwriting is adaptable to various borrower scenarios.”

- “You are paying extra for the structure and additional opportunities, not because the loan is risky.”

- “A Non-QM loan can help work toward long-term financial goals while keeping future refinancing options open.”

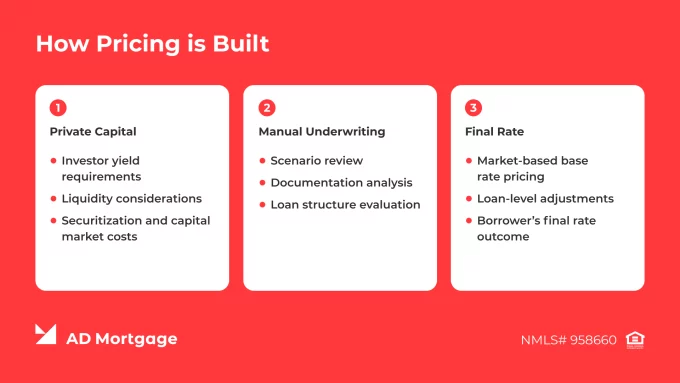

How AD Mortgage Helps Brokers Navigate Non-QM Pricing

AD Mortgage is a leading mortgage lender, recognized as a top Non-QM lender in the U.S. with over 20 years of experience. We offer a wide range of Non-QM loan programs enabling us to say ‘YES’ to our partners and their clients when other lenders don’t.

Take a look at what solution fits your client’s goals and expectations. Just submit a loan scenario and our experts will contact you with a tailored loan program within 30 minutes.

Typically, Non-QM loan rates are higher than traditional loans due to increased underwriting flexibility, lower secondary market liquidity, documentation types, and other factors. However, when used strategically, Non-QM loans can help support long-term financial goals. While Non-QM rates are generally higher than conventional loans, this is not always the case. Depending on the borrower profile, compensating factors, and market conditions, pricing can be comparable to traditional mortgages. The five key drivers of Non-QM interest rates are lender underwriting approach, private capital costs, documentation type, loan structure, and market liquidity. Yes. Non-QM loans include full underwriting, and borrowers must demonstrate the Ability-to-Repay (ATR). The difference from traditional loans is how the borrower profile is reviewed, not whether it is reviewed at all. Yes. Borrowers can refinance into another loan as long as they meet the qualification requirements. Therefore, Non-QM loans can be useful as a temporary solution and part of a long-term strategy. Brokers should educate clients on how Non-QM loans fit into their financial strategy. They should highlight that Non-QM loans provide additional opportunities for borrowers who do not qualify for traditional mortgages but still have strong financial profiles and demonstrate Ability-to-Repay (ATR).

FAQ: How Non-QM Loan Rates are Determined

Why are Non-QM Loan Rates Higher than QM?

Are Non-QM Rates Always Higher?

What Factors Affect Non-QM Pricing the Most?

Do Non-QM Loans Still Verify Ability-to-Repay?

Can Borrowers Refinance Out of a Non-QM Loan?

How Should Brokers Explain Non-QM Rates to Clients?

Fill out the short form and get a call from our AE

Struggling with a loan scenario?

Get a solution in 30 minutes!

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again