Post content:

Your most sophisticated clients expect not only an approval, but also a seamless experience. But in today’s landscape, a strong FICO is only half the story. Even with a 770+ score, a deal can get stuck in a loop of questions and delays that test your borrower’s patience. The key is not just “working harder” but using the right market levers.

Broker success is an AD Mortgage priority, and we want to help you avoid hidden pitfalls that can destroy a great deal. We have created this guide to give you peace of mind and the strategic edge you need to win more Non-QM Scenarios in 2026.

Tip 1. Choose Lender Wisely

When evaluating Non-QM lenders, rate is often the first question brokers ask, and it is an important one. In 2026’s competitive market, where borrowers have become more sophisticated and rate-conscious, pricing matters. But apart from that, there are three other factors that separate good Non-QM lenders from great ones. Let’s explore them in detail.

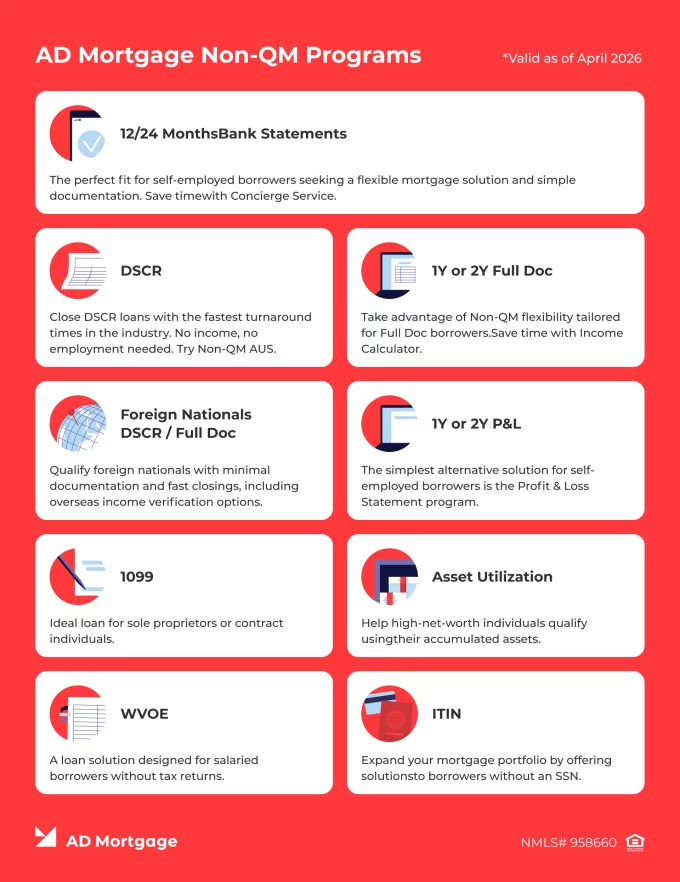

Unique programs

You don’t need an extensive roster of partners to succeed. By mastering just two or three key mortgage lenders and knowing exactly what makes them unique, you can stop guessing and start closing deals faster.

Some lenders can surprise you with programs or overlays that solve problems others won’t touch. For instance, while many lenders follow more traditional criteria, AD Mortgage DSCR loans can:

- Support No-Ratio DSCR financing up to 70% LTV

- Provide lending options for first-time investors

- Allow for the refinance of vacant properties

We provide financing solutions for Foreign Nationals, ITIN holders, and non-permanent residents – categories where traditional options are often limited. Understanding these specific “edge cases” is what transforms a declined application into a closed deal.

Exceptions

But even if, among the whole variety of programs, you have not found a “perfect match,” there are still chances to close the deal. To do that, exceptions might help.

Exceptions are cases when a lender allows a broker to deviate from standard guidelines if the rest of the borrower’s file is strong enough to compensate for that one weakness. Not all lenders offer them, but you should be interested in those who do.

“In some programs, the minimum loan amount can be pretty high. For instance, $400,000 dollars. And sometimes, the property costs exactly $400,000. Obviously, the borrower doesn’t need all this money but can’t ask for less. If you need a lower loan amount, you can ask for an exception already at the Disclosure step. Just ask your Account Executive for guidance.” – Kristina Vafe, Senior Underwriter, suggested.

The same logic can be applied to property characteristics, deal structures, or documents within Non-QM. Exceptions let you close deals that would otherwise fall through the cracks, often with less competition and more grateful clients.

Loyalty Program

“One of my favorite benefits at AD is Partner Points. I use that quite a bit. I save people underwriting fees, 3-day lock extensions.” – says Sam Gabay, Loan Officer from Merit Lending in Las Vegas.

Indeed, some lenders offer brokers to become part of the Loyalty Program, and participation increases the chances of a deal to be closed. For instance, brokers can spend loyalty points to accelerate the process or to cut the expenses on the appraisal credits.

In the first quarter of 2026, data shows that being an ADvantage Loyalty Program member is a massive competitive edge. Members are closing 38% more loans than non-members and getting deals to the finish line about 2 days faster.

Strategically, choosing a lender with the benefits mentioned above, you create a competitive moat that protects your broker-borrower relationship and allows you to win more Non-QM scenarios in 2026.

Tip 2. Avoid Common Mistakes

Even experienced brokers can make a mistake that can wreck a Non-QM deal. Not because they lack skill, but because Non-QM requires a different approach than conventional lending. Small missteps early in the process can snowball into conditions, delays, or denials weeks later.

The good news is that most of these mistakes are entirely avoidable once you know what to watch for. In this section, we will walk through three critical areas where brokers sometimes stumble, and we show you how to avoid them so more of your files make it to the closing table.

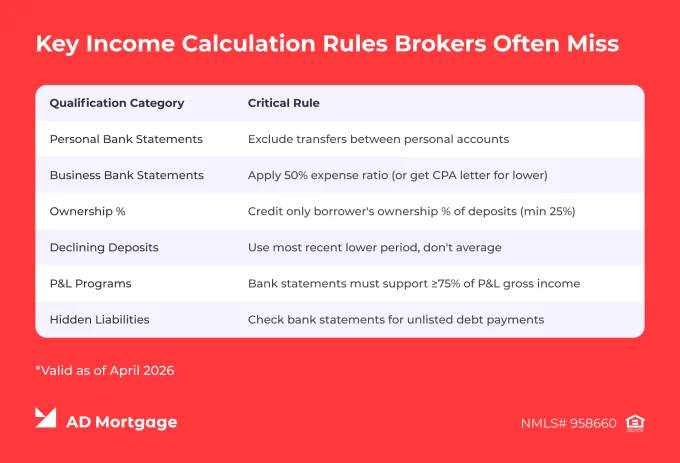

Don’t upload the unnecessary documents

Some brokers assume that more documentation equals a stronger file, but in practice, the opposite is often true.

“We see brokers trying to be helpful by submitting every document they have, but it often backfires,” – explains Kristina Vafe, Senior Underwriter, – “While we appreciate the effort, uploading everything at once forces us to spend hours sifting through the noise, which is usually counterproductive. Of course, this is different from an experienced broker who anticipates a borrower’s unique scenario and provides targeted, helpful files. But generally speaking, when it comes to Non-QM underwriting in 2026, less is often more.”

The solution is to know the program requirements before you submit, and only upload what is explicitly needed for that specific scenario.

Here is an example: if you are submitting a bank statement loan, there is a counterintuitive rule that some brokers get wrong: do not include tax returns or tax transcripts. The guidelines explicitly state they are not required – and if provided, they will make the loan ineligible for the bank statement program entirely.

Experienced brokers understand that underwriters appreciate files that are complete but targeted – such an approach speeds up the processing.

Don’t overstate income

It can be tempting to use the most optimistic version of a borrower’s income to qualify for a larger Non-QM loan, but in 2026, this is a high-risk move that often leads to declined files. A file might look perfect on the initial application (1003), but once the actual income documents arrive, the situation changes. Underwriters pay close attention to this point.

To be fair, the discrepancy is not always intentional. Sometimes, it stems from a misunderstanding between the broker and the borrower regarding what qualifies as usable income.

Therefore, to win more Non-QM scenarios, brokers should always read Non-QM guidelines carefully.

Don’t ignore AI tools

Brokers who ignore AI instruments are operating at a significant disadvantage, spending hours on tasks that technology now handles in seconds. Today, such tools can:

- Look up guidelines instantly and verify requirements

- Compare rates and help with calculations

- Double-check documentation standards

Also, AI can be useful for client communication, marketing, and business management purposes. For brokers looking to close more Non-QM deals in 2026, these tools are quickly becoming a competitive edge. And the list keeps growing every day.

Already Using AI? Tell Us How!

We are running a quick 3-minute survey on how mortgage professionals use technology in 2026, and we want your take. Everyone who completes it gets a free set of 5 AI prompts built specifically for broker marketing needs. These are ready to use with AI right away – no tech skills needed.

AD Mortgage partners also earn 300 ADvantage Loyalty Points, redeemable for appraisal credits, underwriting fee waivers, rush closings, and more.

Share your experience and pick up some useful tools along the way!

Tip 3. Keep Secondary Market in Mind

Most brokers don’t usually think about the secondary market. Yet it plays the key role in rates, mortgage programs, and general housing affordability. That is why ignoring it means missing opportunities that could help you close more deals and deliver better outcomes for your borrowers.

How secondary market impacts Non-QM mortgage rates

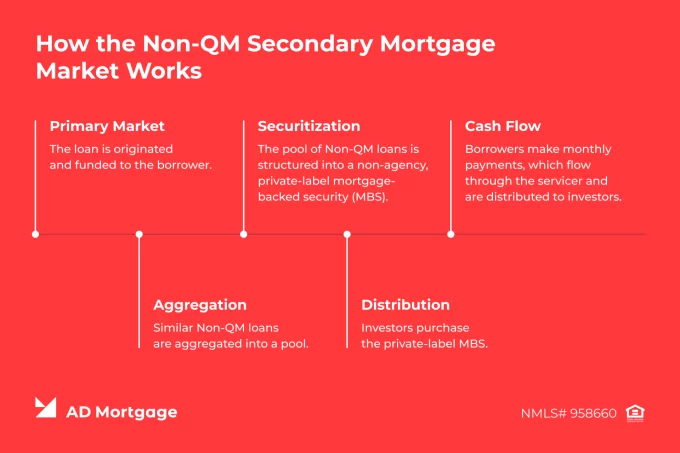

In Non-QM, lenders don’t just “set” rates. They price loans based on what private investors are willing to pay for mortgage-backed securities (MBS). Investors in the secondary market buy Non-QM loans because they offer higher yields compared to other assets. When investor demand for these securities increases, lenders can offer more competitive rates to brokers.

The secondary market provides the capital that allows Non-QM lenders to fund new deals. When the secondary market is “liquid” and active, you see a wider variety of programs (like DSCR or Asset Utilization) and faster funding times.

To provide the best value in 2026, a broker can read rating agency presale reports. They show which loans investors are currently willing to buy – the LTVs, credit scores, alternative income documentation in active securitization pools. If you structure deals that mirror what is in those pools, your lender has a clear and easy exit. That is another way to win more Non-QM scenarios in 2026.

Tip 4. Choose Your Borrower

As Dustin Owen, Certified Mortgage Banker, puts it: “I don’t need to get more leads if I can just get better leads”. This idea captures a shift happening in the 2026 Non-QM market: not every lead that comes through your pipeline is worth pursuing.

Non-QM has evolved past its subprime roots. In 2024, the average Non-QM borrower had a 776 FICO score, virtually on par with conventional conforming borrowers. Non-QM loans closed at an average 75% loan-to-value; thus, these are not risky deals. The borrowers driving Non-QM growth are now people with strong credit who don’t fit traditional income documentation. Their obstacle is not low creditworthiness.

This matters because better borrowers mean better economics. Deals with strong-credit borrowers close faster, at better pricing, and with fewer conditions.

You can see this when you are working with a 760 FICO self-employed consultant qualifying, for instance, for Bank Statement. That file has a high chance to close quickly – unlike a 600 FICO W-2 employee with late payments hoping Non-QM will overlook their credit issues. This one can burn weeks and may not close at all.

The most successful Non-QM brokers in 2026 are not chasing volume. On the contrary, they are qualifying leads based on whether the challenge is income documentation or credit behavior, and building pipelines around the first group, not the second.

Conclusion

To win more Non-QM scenarios in 2026, a broker needs to move with more precision. As the Non-QM market shifts toward high-credit, sophisticated borrowers, there is less room for error in how you calculate income and organize your files.

To take the guesswork out of your day, we offer a dedicated tool that pairs your client’s profile with the most suitable mortgage program. Instead of navigating complex guidelines alone, you can share your loan scenario with us. One of our Account Executives will personally follow up within 30 minutes to help you finalize the best path forward.

FAQ: Win More Non-QM Scenarios

What is the single most effective way to speed up Non-QM underwriting in 2026?

The fastest path to the closing table is submitting a “targeted” file rather than an unorganized volume of documents. By uploading only the specific documents required for the chosen program, you eliminate the “noise” that forces underwriters to spend hours sifting through unrelated files.

Are Non-QM loans risky?

Non‑QM loans are not automatically risky, but their overall risk level depends on how the loan is structured and how well it aligns with the borrower’s financial situation. Much of the uncertainty around Non‑QM comes from misconceptions or a lack of clarity around underwriting, documentation, and long‑term planning. For a deeper look at where real risks may arise and how they’re typically managed – we break it down in detail in our article.

What happens if a scenario falls outside standard guidelines?

It does not necessarily mean that the deal is over. AD Mortgage looks for ways to say “yes” through exceptions if the rest of the borrower’s profile is strong. Whether it is a unique property or a specific loan amount, reaching out to your AE early can turn a potential denial into a closed deal.

When and how should I request an exception for a non-standard scenario?

You can request an exception as early as the Disclosure step. Always consult your Account Executive for guidance to ensure the rest of the file is strong enough to compensate for the weakness.

How can I use the ADvantage Loyalty Program to prevent a deal from falling through?

Members can use loyalty points to cover 3-day lock extensions, waive underwriting fees, or rush the closing process. This provides the flexibility needed to handle last-minute delays that might otherwise destroy the deal.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.