Post content:

VA loans are one of the most powerful mortgage tools for eligible borrowers. Whether your client wants a standard loan, to refinance an existing mortgage, or borrow against their home equity, there are several types of VA loans that cover different needs.

To help clients find the best mortgage option, brokers need to understand the nuances of the programs available. This article provides a quick, broker-first breakdown of VA loan types and offers suitable AD Mortgage products.

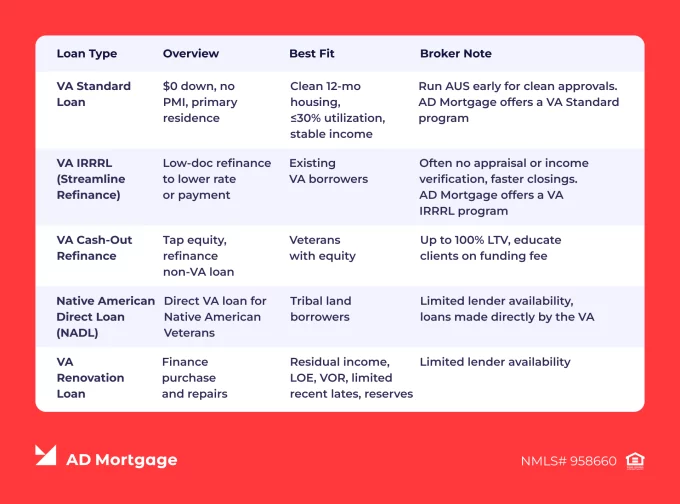

VA Loan Types at a Glance: Broker Table

This brief comparison table of VA loan types is a convenient tool for brokers to identify the differences and explain them to clients.

For any VA loan, keep eligibility requirements in mind. Borrowers should obtain a Certificate of Eligibility (COE), meet credit score standards, have sufficient residual income, and comply with lender guidelines.

Types of VA Loans in the Market Explained

To guide clients through the mortgage process efficiently, brokers need a deep, detailed understanding of each program. The following section breaks down VA loan types and highlights their key features.

VA Purchase Loan

This standard program allows eligible veterans to purchase a primary residence with no down payment and no private mortgage insurance (PMI). The VA’s Minimal Property Requirements (MPRs) apply to ensure that the safety, sanitation, and structural standards are met. Seller concessions can reach 4% of the loan amount and cover the funding fee or other allowable expenses.

VA IRRRL (Streamline Refinance)

Existing VA loans can be refinanced for lower rates or payments. This approach is not only cost-efficient, but also fast and straightforward, making the overall process more accessible. An IRRRL typically requires minimal documentation and, in most cases, no appraisal. Additionally, borrowers must provide a net tangible benefit (NTB) demonstrating the financial benefit of the refinancing.

VA Cash-Out Refinance

Eligible borrowers can tap their equity or refinance a conventional loan into a VA loan. While the VA allows up to 100% LTV, many lenders cap it at 90%. Borrowers need to keep in mind that a Cash-Out Refinance requires a full new appraisal, thorough underwriting, and a funding fee. This process is more traditional and extensive and should not be confused with the streamlined IRRRL.

Native American Direct Loan (NADL)

This program helps Native Americans buy, build, or improve houses on Federal Trust Land. NADLs are offered directly by the VA, not private lenders, and have limited availability. Nevertheless, the benefit can be highly valuable for eligible borrowers as it offers no down payment, no PMI, and a reduced funding fee.

VA Renovation Loan

Borrowers can finance (or refinance) both home purchases and the costs of home improvements or repairs in one loan. These loans are less common, so few lenders offer them. Additionally, the construction provider must meet the VA approval requirements.

VA Energy Efficient Mortgage (EEM)

By financing energy-efficient upgrades for their homes, borrowers can reduce utility costs over time and contribute to a more sustainable future.

AD Mortgage Programs

To support eligible military members in purchasing their homes, AD Mortgage offers a couple VA loan programs:

- VA Standard. Eligible veterans with a FICO score of 580 or higher who want to buy, build, or adapt a residential property can apply for loans of up to $2 million with no down payment.

- VA IRRRL. Existing VA loans can be refinanced for up to $1.5 million, with no appraisal required. The minimum FICO score is 580.

Broker Value: AD Mortgage provides fast turnaround times, flexible credit options, and direct support for brokers throughout the loan process. Join the AIM Partner Portal to optimize your workflow and implement smart technologies.

Broker Tips: Positioning VA Loans with Clients

Help your clients clearly understand both the positive and challenging aspects of VA loans. To do so, state and explain the following key points:

- VA loans offer $0 down payment and no monthly PMI. Additionally, the VA doesn’t set loan limits for eligible borrowers with full entitlement, compared to conforming loans which are capped by FHFA loan limits. Generally, VA loans offer greater flexibility in credit scores and better interest rates than conventional loans, so they are often a preferred option for eligible borrowers.

- The funding fee is obligatory, though exemptions apply for veterans with service-connected disabilities and surviving spouses.

- Clean VA files close as fast as conventional loans – part of a broker’s job is to debunk common myths and bring transparency to the mortgage process.

FAQ: Types of VA Loans

What are the Main Types of VA Loans?

Common VA loan types are the VA Purchase Loan, VA IRRRL (or Streamline Refinance), VA Cash-Out Refinance, Native American Direct Loan (NADL), and VA Renovation Loan.

Can VA Loans be Used for Investment or Vacation Properties?

No. The VA allows these benefits only for primary residences. Generally, the borrower must occupy the home within 60 days after closing.

What is the Difference Between VA IRRRL and Cash-Out Refinance?

A VA IRRRL is intended for refinancing an existing loan into better terms. A VA Cash-Out Refinance allows borrowers to tap into their home equity or refinance a non-VA loan into a VA loan. Additionally, the process differs. An IRRRL is streamlined and requires minimal paperwork, while a Cash-Out Refinance requires a new appraisal and involves extensive underwriting.

How Does the VA Funding Fee Work?

The VA funding fee is a one-time payment charged at closing that goes to the Department of Veterans Affairs to help sustain the program. Borrowers can pay the fee upfront or rolled into the loan, although some exemptions may apply.

Does AD Mortgage Offer All VA Loan Programs?

No. AD Mortgage offers the two most common VA loan programs – VA Standard and VA IRRRL.

Key Takeaways

- VA loans include Purchase, IRRRL, Cash-Out, NADL, Renovation, and EEM programs.

- Brokers should match a client’s goals with the right product and clearly explain the program’s requirements and conditions.

- AD Mortgage provides VA Standard and VA IRRRL programs with flexible terms and direct broker support.

Conclusion

There are several types of VA loans for different purposes such as buying, building, maintaining, or adapting a house. Borrowers might not be familiar with the nuances of each product, and it is the broker’s job to guide their clients through the loan process.

AD Mortgage is here to help brokers provide the best quality service. With the AIM Partner Portal, you can streamline your process with self-disclosure, a simple loan income calculator, and the industry-specific LEADer CRM.

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again

")