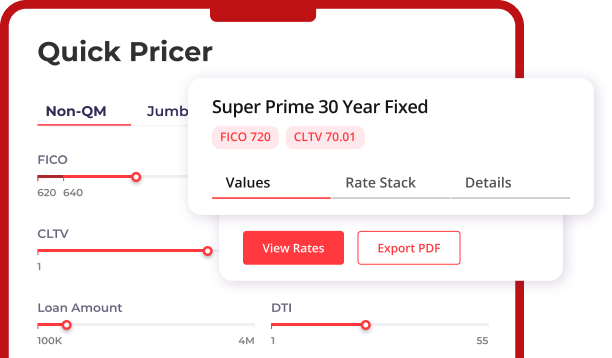

Available on Prime, Super Prime, and DSCR

Our ITIN home loan program lets your borrowers finance a home using an Individual Taxpayer Identification Number (tax ID number) instead of a Social Security Number. Built for brokers serving non-U.S. citizens and foreign nationals, ITIN mortgage loans open homeownership to qualified borrowers with no SSN — primary, second home, or investment. Grow your pipeline with a flexible ITIN loan program backed by 24-hour turn times.

Program features

Struggling with a loan scenario? Push the button and get a solution in 30 minutes!

Write to us, we will contact you within 30 minutes.

As fast as

24 hr

As fast as

24 hr

As fast as

48 hr