Home appraisal can be an issue when getting your loan closed. Depending on your lender’s requirements, they can be costly and frustrating if not done correctly the first time around.

Having a good idea of the ‘ins and outs’ of home appraisal can save you and your borrower a ton of headaches and some money. This step is necessary for the lender; however, some unexpected factors can directly affect a home appraisal.

As a mortgage professional, you need to be prepared for your clients, navigate the process of avoiding renegotiations, and that leads to earning client trust.

Why Appraisal Outcomes Matter to Brokers

So, why are appraisal outcomes crucial? The main point here is that a home’s appraised value influences several key components of a mortgage transaction, especially the Loan-to-Value (LTV) ratio. A high LTV caused by a low appraisal might lead to costly ripple effects. Additionally, borrowers may no longer qualify for the removal of Mortgage Insurance (MI). This involves ongoing monthly expenses that many borrowers didn’t expect.

Low appraisals may also affect rate-lock commitments. If the deal is delayed due to price disputes or renegotiations, the original lock rate may expire. This forces borrowers to pay extension fees or re-lock at a higher rate, which could be an issue in today’s rather unstable economy.

Besides, a difference between the appraised value and the contract price often ends up with tricky conversations between brokers, buyers, and sellers. This may lead to restructuring the loan, asking the buyer to bring more cash to the deal, or renegotiating the purchase price. All those things create unnecessary stress and delays.

All this means that a low appraisal can jeopardize a beneficial deal. That’s why proactive appraisal preparation is a critical tool for any broker looking to protect their pipeline and have smooth closings.

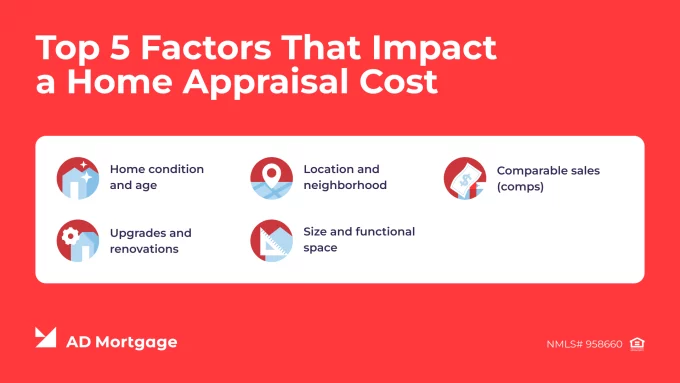

Top 5 Factors That Impact a Home Appraisal

Most mortgage professionals are very aware of home appraisal basics, but let’s cover them all just to be sure.

A home appraisal is a professional estimate of a property’s market value. It’s typically conducted during the mortgage process. Licensed appraisers include:

Home Condition and Age

Homes with updated systems such as HVAC, plumbing, and electrical, are more attractive to appraisers and potential buyers. Regular maintenance can prevent loss of value.

Older homes have their own particular charm and atmosphere, but they can also come with issues like outdated electricity systems or plumbing. Appraisers pay attention to age and overhauls made to older properties.

A well-kept exterior can enhance a property’s appraisal. Homes that look inviting often appraise higher.

Location and Neighborhood

Homes located near schools, parks, malls, and public transportation tend to get higher appraisals. It happens because families value access to quality education and convenience in their daily lives.

The safety and aesthetics of a neighborhood can considerably impact property values. Appraisers often look at crime rates, community engagement, and green spaces.

High-demand areas typically experience rising property values. Appraisers take into consideration local market trends, such as the popularity of neighborhoods and their possible growth in the future.

Comparable Sales (comps)

Appraisers check recently sold properties in the area that are comparable in size, age, and condition. This analysis helps to set the property’s value baseline.

Typically, in a seller’s market with exceeded demand supply, property values may rise. In contrast, if there are more homes than buyers in a buyer’s market, property values may decrease.

Appraisers consider such factors as interest rates, employment rates, and consumer confidence to gauge market stability.

Upgrades and Renovations

Some upgrades can yield a higher return on investment. Kitchens and bathrooms are often those spots where renovations can repay.

Energy-efficient upgrades such as new windows, insulation, and smart home technology can positively influence appraisals.

The quality of renovations matters. High-quality materials used in redesign can boost a home value, and vice versa; DIY projects of poor quality can detract from it.

Size and Functional Space

No wonder larger properties have higher appraisals. Appraisers take into account the total living area and how it compares to similar properties within the area.

A well-designed layout can upgrade a property’s value: open floor plans are more in demand, and homes with awkward layouts may be appraised lower.

Obviously, the number of bedrooms and bathrooms impacts pricing, as well. More rooms provide an opportunity to accommodate larger families, that’s why they appeal to a broader market.

Purchase Appraisal vs. Refinance Appraisal

Purchase appraisal and refinance appraisal are almost alike, as they are both used to assess a home’s value. However, don’t miss an important detail: the buyer can’t attend an appraisal, but the homeowner is allowed to attend it. This might be their advantage.

If the homeowner attends, they can highlight the best parts of the home and any work they’ve done. The homeowner’s involvement could help the appraiser set a higher property price.

Home Appraisal Cost

Home appraisal costs can differ by state and property size, while the fee can vary between $300 and $1,200. Most are around $600-$1,000, with costs mostly based on the geographical area of the home.

How Long Does a Home Appraisal Take?

The home appraisal process usually takes about 7-10 days to complete. Don’t neglect some simple yet essential steps to prevent delays and support a smoother mortgage experience. Read our article to learn even more about how long an appraisal takes.

The physical visit by a home appraiser takes about an hour, depending on the size of the client’s property. Although, there are other steps involved. The assigned appraiser will study trends, local county records, and recently sold similar homes in your client’s area, so-called “comps.”

Once your appraiser compiles and analyzes all the information and data, they will present a final report on the property’s value.

Understanding the Home Appraisal Process

The home appraisal process is essential in both home purchases and refinances. For a home purchase, the lender typically orders the appraisal to ensure the property’s value matches the loan amount. In a refinance, the lender also orders the appraisal to verify current market value and determine equity.

What Hurts a Home Appraisal?

Several factors can hurt a home appraisal and lower your property’s market value. Low-value comps such as recent sales of similar homes in the area can drag down your appraisal, especially if the market has softened. Poor maintenance, visible wear and tear, or unresolved repairs reduce a home’s perceived condition. Outdated systems, like aging HVAC, plumbing, or electrical, may signal future costs to buyers. Additionally, location limits, such as proximity to busy roads, declining neighborhoods, or limited amenities, can negatively impact value. Understanding these issues helps homeowners prepare and protect their equity.

Top Home Appraisal Tips: The Broker Checklist

Help your clients secure a strong home valuation with this proven appraisal prep checklist. As a rule, a higher appraisal results in smoother financing and more beneficial loan terms.

Do a DIY Pre-Appraisal Walk-Through

Before the appraiser arrives, walk around the property as if you were the appraiser. Look for visible damage, deferred maintenance, or signs of wear that could affect value.

Research & Provide Better Comps

Don’t rely solely on appraisers’ data. Deliver your own selection of recent, high-value comps that match the subject property in size, condition, and location.

Boost Curb Appeal Fast

First impressions matter. Encourage homeowners to mow the lawn, clean up clutter, and refresh exterior paint or landscaping for an instant visual upgrade.

Tackle Easy Mechanical Fixes

Ensure basic systems like lights, toilets, HVAC, and smoke detectors are fully functional. Small repairs signal good maintenance and prevent value deductions.

Document Upgrades & Permits

Gather receipts, photos, and permit records for renovations and updates. Highlighting added value through improvements can significantly influence the appraisal.

Highlight Neighborhood Amenities

Remind appraisers of nearby schools, parks, shopping, or transit options that enhance lifestyle and property desirability.

Coach Borrowers on Attendance Etiquette

Instruct borrowers to be present but not pushy. They should be available to answer questions, yet respectful of the appraiser’s process. A professional tone makes the right impression.

Use this checklist to proactively manage appraisals and avoid surprises at closing.

Special Appraisal Scenarios

Some properties demand a bit more attention during the appraisal process. Unique or rural properties like farms, custom homes, or off-grid buildings can be harder to value due to their unusual features and limited comparable sales. New construction appraisals must factor in plans, costs, and speculative value, often before the home is finished.

Government-backed loans like FHA and VA come with specific appraisal guidelines, including stricter condition requirements and safety standards. Understanding these special scenarios helps brokers set the right expectations and avoid costly delays in underwriting or closing.

Looking for a suitable loan program?

Choose among 20+ programs and get

a detailed loan calculation

Loan Calculator

Programs

Case Study: Appraisal Challenges on a Rural Property with a VA Loan

A borrower applied for a VA-backed loan to buy a custom-built log home located in a rural area of Montana. The property sat on 20 acres, including a private well and solar power system, and had limited nearby comparable sales.

Appraisal Issues Identified

Lack of Comps

The nearest property sold with similar features was over 10 miles away and differed significantly in design and land use. The appraiser was forced to stretch the “comparable” definition, using homes that didn’t fully reflect the subject property’s unique value.

VA Minimum Property Requirements

VA guidelines require the home to be safe, sound, and sanitary. The off-grid solar system raised red flags regarding utility stability. The appraiser noted concerns about whether the power setup met MPR standards.

Custom Features and Adjustments

The log construction, upgraded hardwood finishes, and geothermal heating system were not standard for the area. The appraiser struggled to assign accurate dollar adjustments due to a lack of market data.

Resolution Steps

The lender worked with a VA-approved appraiser to request a Reconsideration of Value (ROV), submitting builder invoices and an energy efficiency report to justify the home’s value.

Additional comps were provided by the borrower’s agent, including a custom home just over 15 miles away that had recently closed.

The appraiser issued a revised value that still came in lower than the contract price. However, it was high enough for the borrower to proceed by negotiating a small seller concession.

Outcome

The sale closed successfully after a $10,000 price reduction and the borrower’s agreement to cover closing costs. The lender accepted the revised VA appraisal, and the borrower moved forward without needing appraisal gap coverage.

Takeaway

Special appraisal scenarios, especially in rural or custom-home markets, require extra documentation, flexibility, and communication. Understanding VA guidelines and preparing for limited comps can help brokers navigate these complex cases.

Handling A Low Appraisal

When a home appraisal comes low, it can threaten to derail the deal, but brokers have options. Start by assembling a rebuttal packet with better comps, photos, and a detailed list of upgrades. Submit a reconsideration of value request to the lender for a second review.

If the value still fails to satisfy, try to fill appraisal gap coverage either through extra cash from the buyer or lender-approved solutions. Use renegotiation scripts to guide calm, fact-based conversations between buyers and sellers. Proactive handling of a low appraisal can keep deals on track and protect your clients’ interests.

The Bottom Line

A strong home appraisal is the result of smart preparation and meticulousness when it comes to details. The following article and the checklist can help you, as a mortgage professional, guide your clients through every key step: from pre-appraisal walk-throughs to proper documentation and neighborhood insights.

Be proactive. It helps avoid delays, supports accurate valuations, and keeps deals moving smoothly to close.

Enhanced Broker Portal

that makes your job easier

- All operations at your fingertips

- Easy-to-use intuitive interface

- Integrated AI technology

Show Me How

FAQs

1. How long does an appraisal take?

Typically, 5-10 business days can vary based on location and property type.

2. Can sellers attend the appraisal?

Yes, they can. However, it’s more common for agents or buyers to attend. Attendance is not obligatory but can be beneficial when done professionally.

3. How often do appraisals come in low?

Industry data shows about 5-10% of appraisals fall short of the contract price, especially in competitive markets.

4. Are appraisals required for all loans?

Most loans require them, but some refi’s may qualify for appraisal waivers (if supported by DU/LP findings).

5. What’s the difference between a desktop and full appraisal?

Desktop appraisals rely on digital data and don’t require a site visit. Full appraisals include physical inspection.

6. Can you challenge an appraisal?

Yes, but only through the lender’s official dispute process, which is usually by submitting additional comps or correcting factual errors.