Post content:

Brokers know the frustration of a deal that should work but doesn’t fit a lender’s rigid box. While the industry waits for the rules to change, brokers are the ones bridging the gap for their clients. This daily struggle is where the real market lives.

AD Mortgage believes that true leadership is not about finding ‘workarounds’ for these systemic gaps. It is about listening to these real-world insights and treating them as blueprints for innovation rather than inconveniences. The result is that the burden is transformed from an individual struggle to a collective solution.

And this philosophy is not an abstract theory. On the contrary, it’s the approach that brought Max Slyusarchuk recognition as an Industry Titan.

Max Slyusarchuk Named Industry Titan for Broker-Centered Leadership

Max Slyusarchuk, CEO of AD Mortgage, has been recognized as an Industry Titan by National Mortgage Professional – an award that celebrates mortgage leaders whose expertise, perseverance, and professionalism have left a lasting mark on the industry.

The Award reflects a commitment to partnership where broker challenges became company priorities. Moreover, it recognizes a model where broker complaints became operational roadmaps, when listening translated directly into action.

In 2025, brokers consistently identified three problems: uncertainty in Non-QM manual underwriting, poor control of compliance timelines, and appraisal delays. These were industry-wide pain points. What made the difference was how they were addressed.

Max’s response was to eliminate them systematically, one after another.

- The Non-QM AUS solved the uncertainty of manual underwriting. For years, brokers waited days for unpredictable decisions on their Non-QM files. This system replaced manual reviews with AI-driven loan decisions delivered in under five minutes. It shifted the process from waiting for an answer to knowing it almost instantly.

- Self-Disclosure resolved compliance delays. Previously, brokers spent too much time chasing documents while deadlines were missed. The AIM Partner Portal now allows brokers to generate disclosure packages with e-signatures in about one minute. By mid-2025, this tool accelerated timelines by 95% and gave brokers control over their schedules.

- The Appraisal Center eliminated the chaos and unpredictable delays. Previously, fragmented communication left brokers without the updates they needed for borrowers. This system brought structure: brokers now select from approved AMCs with auto-filled orders and reviews completed in one to two days.

Each solution addressed a specific pain point brokers had been managing alone. Together, they reset industry expectations for efficiency and reliability through quiet and systematic problem-solving.

Why This Pattern Works: Evidence from Industry Evolution

The biggest shifts in mortgage lending have always followed the same playbook: brokers identify gaps, leaders listen and adapt, markets evolve. Max’s Industry Titans Award recognizes leadership that helps apply this proven approach to the everyday operational challenges brokers face.

Here’s how this pattern played out at the industry level.

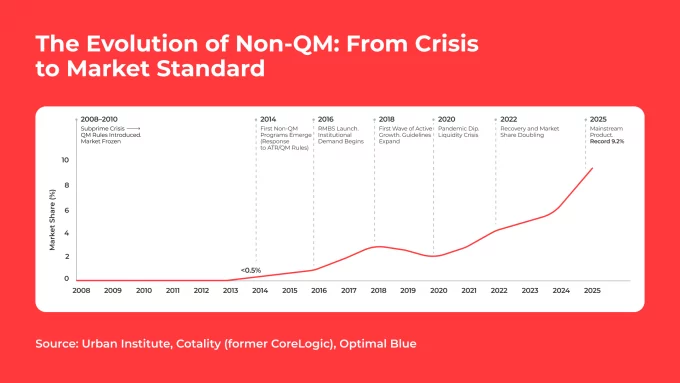

1. The Evolution of Non-QM

Non-QM didn’t expand by accident. After the 2008 Subprime Crisis, mortgage standards tightened, and regulators introduced Qualified Mortgages to establish safer lending practices. But as standards became stricter, creditworthy borrowers found themselves excluded. These were self-employed individuals, freelancers, contractors whose income structures didn’t align with traditional documentation requirements.

Brokers immediately recognized this gap. They repeatedly submitted applications for borrowers with strong cash flow, solid credit scores, and demonstrated ability to repay. Yet these borrowers couldn’t qualify under existing guidelines.

Declined applications signaled that current frameworks were excluding viable borrowers, and the industry responded. Lenders widened guidelines and introduced flexible documentation options. What began as persistent broker feedback about underserved borrowers evolved into an entirely new segment of the mortgage industry.

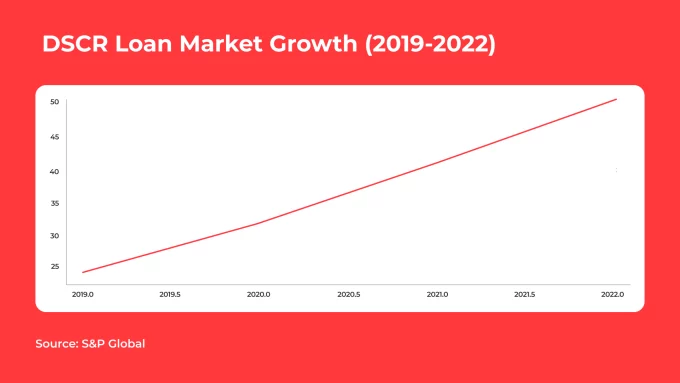

2. DSCR Became More Universal

DSCR loans followed a similar trajectory. Initially considered niche products for sophisticated investors, and they played only a minor role in the mortgage industry. But brokers working with real estate investors encountered the same pattern: creditworthy clients with strong rental properties couldn’t qualify through traditional personal income verification.

The pandemic accelerated shifts in work culture and housing demand. Investor activity surged as rental property acquisitions increased. Brokers consistently presented these investment scenarios, demonstrating clear market demand for alternative qualification methods. And lenders responded by expanding DSCR programs far beyond their original scope.

The Same Pattern, Applied at Every Scale

Both Non-QM and DSCR followed the same playbook: brokers identified the gaps, lenders adapted, and the entire market benefited. This pattern doesn’t only work at the industry level. It works just as powerfully when individual leaders adopt the same principles at the operational level, where brokers feel the impact in every transaction.

This is exactly what Max Slyusarchuk’s Industry Titans Award recognizes. While Non-QM and DSCR show the pattern at market scale over decades, Max demonstrated it at the operational level in real time, systematically solving the problems brokers voiced, measuring success not by announcements but by adoption. And as a result, brokers were finally heard in ways that actually improved their business.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.