What Is a Conventional Loan? Broker Guide to Requirements, Down Payment, PMI, and Borrower Fit

April 01, 2026

‘What is a conventional loan?’ – to answer this question briefly: these are mortgages that are not insured or guaranteed by the government. Conventional loans are the most common type of mortgage, representing around 70% of the market.

In this article, we describe these loans in detail, highlight the difference between conforming and non-conforming conventional loans, and share the best-fit borrower profiles.

What is a Conventional Loan?

Conventional loans are mortgages offered by private lenders – companies such as AD Mortgage, banks, or credit unions – and are not issued or backed by the government like FHA, VA, or USDA loans.

Because the lenders take on all the risk, conventional loans generally have stricter credit criteria and may require a larger down payment for borrowers with weaker financial profiles. However, borrowers with strong credit and stable income can often access more favorable terms and save money in the long run.

The term ‘conventional’ might sound confusing to some borrowers, making it seem like a default option, when in reality, conventional loans come with strict qualification standards.

How Does a Conventional Loan Work?

Overall, the conventional loan process is similar to other types of mortgages.

The mortgage lender originates the loan. Depending on the type – conforming or non-conforming, which we will touch on later – the loan requirements might follow standardized rules or lender-specific overlays. Typically, underwriting evaluates credit, income, assets, DTI, down payment, property, loan amount, and other factors to determine the borrower’s ability to repay the loan.

If the loan meets agency criteria, it can be sold to Fannie Mae or Freddie Mac on the secondary market. Otherwise, the loan can also be sold, but to private investors and institutions. In either case, the loan functions the same for the borrower.

The borrower’s responsibility is to make monthly payments covering principal and interest, along with any escrowed costs such as taxes and insurance. This is often referred to as PITI.

Types of Conventional Loans

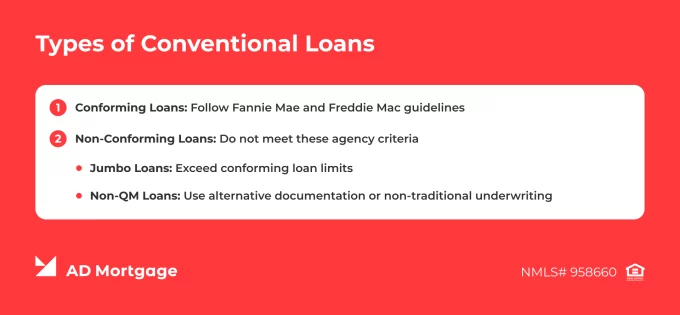

Depending on whether the loan meets agency guidelines, conventional mortgages are divided into two categories:

Conforming conventional loans are mortgages that follow guidelines set by Fannie Mae and Freddie Mac. These rules cover requirements such as maximum loan limits, credit scores, and documentation standards. Because these loans are easier to resell on the secondary market, they are considered less risky for lenders. Therefore, they typically come with more favorable pricing and better rates. >AD Mortgage currently offers a wide variety of conforming loan programs, including Conventional Standard, Freddie Mac HomeOne for first-time homebuyers, Fannie Mae HomeReady, Freddie Mac Home Possible, and refinancing options.

Non-conforming conventional loans are mortgages that do not meet these agency criteria – including jumbo (exceeding conforming limits) and Non-QM loans (falling outside standard underwriting). Usually, these loans offer larger loan amounts or allow borrowers with non-traditional credit to qualify. Due to higher risks for lenders, non-conforming loans are typically more flexible but come with higher rates. Review the AD MortgageNon-QM mortgage page and AD Power Jumbo for non-conforming loan offerings.

Conventional Loan Requirements

As conventional loans are not guaranteed by the government, lenders set their own requirements to manage risk. Additionally, these requirements help evaluate the borrower’s financial profile accurately and ensure that they are able to repay the loan.

While the requirements vary by the lender, there are common guidelines and overlays that we explore further.

Conventional Loan Credit Score

It is often possible to qualify with a score as low as 620. However, as with other loans, a higher score means better terms. Apart from the score, the lender evaluates credit history as a whole, including payment history, negative events, and outstanding debts.

AD Mortgage’s programs offer additional flexibility in credit score requirements, as some of them allow non-traditional credit sources, use FICO per AUS, or consider compensating factors.

Conventional Loan Down Payment

Some programs allow a down payment as low as 3% of the home purchase price – for example, the Freddie Mac HomeOne program for first-time homebuyers. However, most programs require a down payment of 5% to 20%, depending on the borrower profile.

Additionally, when making a down payment of 20% or more, the borrower is typically not required to pay private mortgage insurance (PMI), which otherwise adds to the monthly mortgage payment.

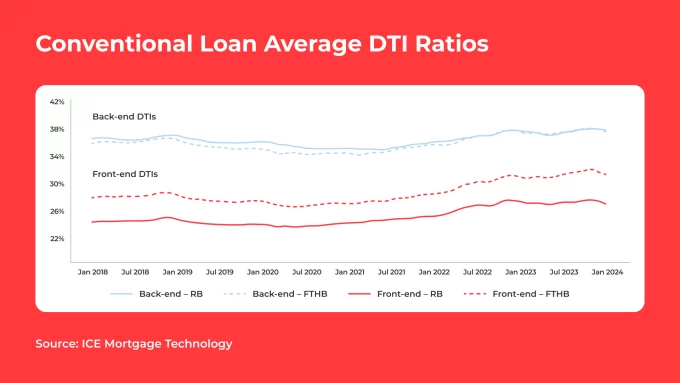

Conventional Loan Debt-to-Income (DTI) Ratios

The DTI is a key parameter in assessing whether the borrower can afford the loan. Lower DTIs generally indicate greater financial stability and are considered lower risk for lenders.

Conventional loans typically allow DTI ratios up to 43%-45%. Many AD Mortgage programs accept DTI per AUS, meaning that the ratio may be higher when supported by compensating factors.

Conventional Mortgage Income, Assets, and Documentation

To evaluate a borrower’s financial situation, the lender reviews their income documentation. For conforming loans, traditional documentation – such as pay stubs, W-2 forms, and tax returns – is typically required. Non-QM loans may accept alternative documentation, including bank statements and profit-and-loss statements.

In addition to income documentation, lenders verify the borrower’s assets, including savings and investment accounts, to ensure there are sufficient funds for the down payment, closing costs, and required reserves.

Conventional Mortgage Property Standards

Conventional loan property requirements are mostly the same as other types of mortgages. The home must meet basic safety, livability, and structural standards to serve as adequate collateral for the loan.

The appraisal, and sometimes a property inspection, is performed to establish the market value of the home and ensure that the property can be resold if necessary.

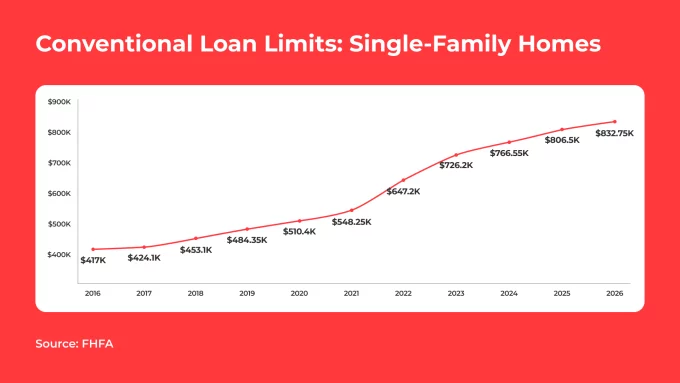

Conventional Loan Limits and Loan Amounts

The Federal Housing Finance Agency (FHFA) sets conventional loan limits and updates them annually. In 2026, the limit for one-unit properties in most counties is $832,750, while certain high-cost areas, such as some counties in Hawaii, can exceed $1,250,000.

Loans that fall outside these limits are called jumbo loans and usually require higher credit scores, larger down payments, and stronger reserves.

Loan amounts depend on a variety of factors, including program guidelines, lender overlays, the borrower’s credit history, down payment size, and compensating factors.

Do Conventional Loans Require PMI?

Private mortgage insurance (PMI) is specific to conventional loans and protects lenders in case the borrower defaults. Typically, PMI is required if the down payment is less than 20% of the home value.

It is important to note that the PMI on conventional loans is not permanent – unlike mortgage insurance premium (MIP) for FHA loans, which are often paid for the entire loan term. Once the borrower reaches 20% equity in the home, PMI can be canceled upon request, and when the borrower reaches 22% equity, it is canceled automatically.

Therefore, when explaining the PMI to their clients, brokers should stress the following key points:

If a borrower makes a 20% or higher down payment, PMI is typically not required.

Once the borrower reaches 20% equity in the property, PMI can be canceled.

PMI costs typically range from around 0.3% to 1.5% of the original loan amount per year.

Conventional Loan vs Government-Backed Loan

Loan programs are designed for different financial situations, and a broker’s goal is to match clients with the right solution. While exact requirements vary by lender, the table below summarizes general guidelines for each loan type. Loan options should be considered as part of the borrower’s overall financial strategy, ensuring they are beneficial not only at closing but also in the long run.

Conventional Loan

FHA Loan

VA Loan

USDA Loan

Credit Score

Typically 620+

Typically 580+ (500-579 with 10% down)

Typically 620+

Typically 640+

Down Payment

3%-20%+

3.5% (580+), 10% (500-579)

0%

0%

Insurance and Funding Fee

PMI required if <20% down, cancelable at 20%-22%

MIP, often life of loan

Funding fee, no monthly MI

Guarantee fee

Property and Use-Cases

Primary, second, or investment properties

Primary residence only

Primary residence only

Primary in eligible rural areas

Borrower Fit

Good credit, stable income, flexible property use

Lower credit, higher DTI, first-time buyers

Eligible veterans and spouses

Low-to-moderate income buyers in eligible areas

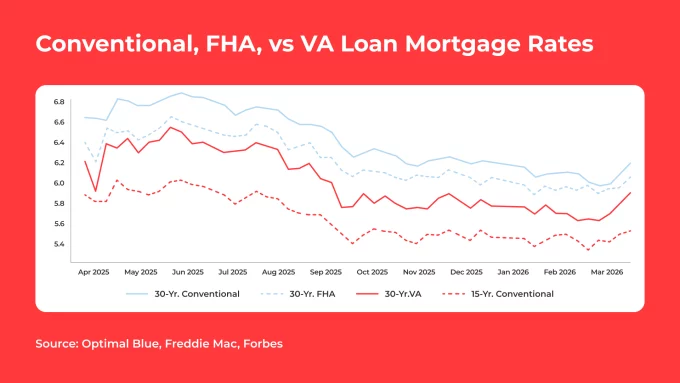

The following graph shows the rate dynamics for 15- and 30-year conventional loans, as well as FHA and VA mortgages. However, it is crucial to remember that these loans are not solely rate-driven, and each option comes with its own associated costs, which should also be considered when making a decision.

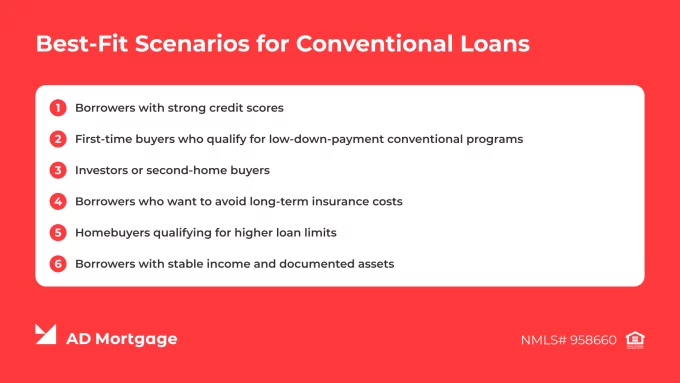

Who is a Conventional Loan Best for?

Conventional mortgages can be a smart financial decision for some borrowers. Check out the following list of the best-fit borrower scenarios. Do you have any clients like these?

Borrowers with strong credit scores

First-time buyers who qualify for low-down-payment conventional programs

Investors or second-home buyers

Borrowers who want to avoid long-term insurance costs

Homebuyers qualifying for higher loan limits

Borrowers with stable income and documented assets

In addition to these ideal borrower profiles, some clients may still qualify for conventional loans but require closer evaluation:

Borrowers with lower credit scores, who may need a larger down payment or strong compensating factors

Borrowers with limited reserves, even if they have stable income and low DTI

Borrowers seeking more flexible qualification guidelines, who may benefit from exploring Non-QM loan options

Pros and Cons of a Conventional Loan

When matching the mortgage program with your client’s case, consider not only the advantages but also the peculiarities and potential drawbacks. Surely, the perception of these factors varies significantly depending on the borrower’s current situation and future goals.

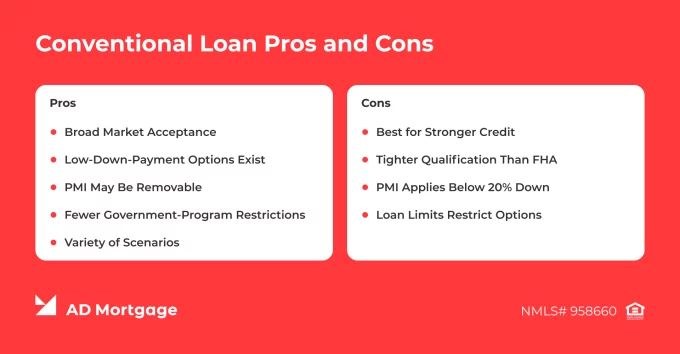

Conventional Loan Pros

Broad Market Acceptance. Conventional loans are popular mortgage options and are highly liquid on the secondary market. Therefore, lenders usually offer competitive pricing, flexible guidelines, and streamlined timelines, compared to less common options.

Low-Down-Payment Options Exist. A down payment as low as 3% of the home value is allowed in some programs, especially for first-time homebuyers.

PMI May Be Removable. When the borrower reaches the 20% equity in the home, PMI can be canceled upon request, and it is removed automatically at 22% equity. This reduces monthly costs in the long run, making conventional loans more cost-efficient in some cases.

Fewer Government-Program Restrictions. Compared to FHA, VA, and USDA loans, conventional loans often come with fewer limitations on borrower eligibility, property location, income thresholds, and other factors.

Variety of Scenarios. Borrowers can use conventional loans for primary residences, second homes, and certain investment properties, depending on program requirements and lender overlays.

Conventional Loan Cons

Best for Stronger Credit. While low-credit borrowers can qualify, those with better credit can achieve better terms and lower rates. Credit scores below 620 are often not accepted, unlike some government-backed loans.

Tighter Qualification Than FHA. Due to higher risk for lenders, income, DTI, and documentation requirements are often stricter.

PMI Applies Below 20% Down. When making a down payment of less than 20%, the borrower must make PMI payments until building 20% of equity.

Loan Limits Restrict Options. FHFA caps conforming loans, while jumbo loans usually require larger down payments and stronger credit and reserve profiles.

Common Broker Talking Points

‘Conventional does not automatically mean 20% down – there are programs with down payment as low as 3% for first-time buyers, and 5% for other borrowers.’

‘Conventional loans are not the same as conforming – they are simply non-government-backed loans and include both conforming and non-conforming mortgages.’

‘FHA loans are not always cheaper overall. They require MIP for the life of the loan, while PMI on conventional loans can be removed only once you reach 20%-22% equity.’

‘Crossing conforming limits does not mean financing is impossible – it just shifts the approach, and we may explore jumbo or other non-conforming options to meet your needs.’

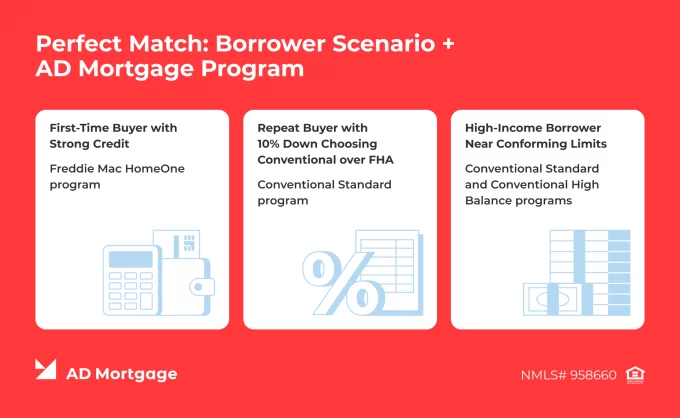

Example Borrower Scenario

There are a variety of conventional loan programs, so it might be challenging for mortgage originators to match their clients with the right option. We have created a list of common scenarios and paired them with the loan programs.

First-Time Buyer with Strong Credit

The borrower would benefit from the Freddie Mac HomeOne program by AD Mortgage, which offers a minimum down payment of 3%, loan amounts up to $832,750, and up to 97% LTV.

Repeat Buyer with 10% Down Choosing Conventional over FHA

Compared to FHA loans, a conventional mortgage allows to remove monthly insurance after building equity, which contributes to lower monthly costs over the life of the loan and often lower overall costs. The Conventional Standard program is a great fit in such a case, offering competitive rates and FICO per AUS.

High-Income Borrower Near Conforming Limits

In this case, it is more efficient for the borrower to stay within conforming limits, rather than move to jumbo territory, to get lower rates and easier qualification. Both Conventional Standard and Conventional High Balance programs offer attractive pricing, various property uses, and FICO per AUS.

FAQ: Conventional Mortgage Meaning

What is a Conventional Loan in Simple Terms?

Conventional loans are mortgagesnot backed by the government. Instead, they are offered by banks, credit unions, and private lenders.

Is a Conventional Loan Government-Backed?

No.Conventional loans are not insured or guaranteed by the government.

What Credit Score Do You Need for a Conventional Loan?

Typically, a credit score of at least 620 is required.

Do Conventional Loans Require 20% Down?

While a higher down payment allows borrowers to qualify for better terms, there are programs accepting down payments as low as 3%-5%, depending on the borrower’s profile and program requirements.

Do Conventional Loans Have PMI?

Yes. When putting less than 20% down, PMI is required until the borrower reaches 20%equity in the home.

What is the Difference Between Conforming and Non-Conforming Conventional Loans?

Conforming conventional loans follow guidelines set by Fannie Mae and Freddie Mac, while non-conforming loans do not meet agency criteria.

Is a Conventional Loan Better than FHA?

Borrowers with stronger profiles – including higher scores, lower DTI, and significant reserves – can benefit from conventional loans in the long run and often get more favorable conditions than FHA loans.

Can First-Time Homebuyers Get a Conventional Loan?

Yes. A conventional loan for a first-time homebuyer can be a smart option, as it may require as little as 3% down with a strong credit score and overall financial profile.

What are the 2026 Conforming Loan Limits?

In 2026, the limit for one-unit properties is $832,750 in most counties. The complete list of conforming loan limits can be found on the FHFA website.

Is a Jumbo Loan a Conventional Loan?

Yes. Jumbo loans are conventional mortgages because they are not backed by the government, even though they exceed conforming loan limits.

Key Takeaways

Conventional loans are non-government mortgages. Banks, private companies, or credit unions issue and service this type of loans. They include conforming loans – which follow guidelines set by Fannie Mae and Freddie Mac – and non-conforming loans – which do not meet agency criteria.

Conventional loan requirements vary by lender and program but often include down payments of 3%-20%, credit scores starting at 620, and DTI ratios up to 43%-45%. Borrowers need PMI when they put less than 20% down. They can cancel it once they reach 20% equity. The lender automatically cancels PMI when the borrower reaches 22% equity.

For borrowers with stronger credit, conventional loans can be beneficial due to their flexibility, potential for lower long-term costs, and competitive rates.

Conclusion

Conventional loans are versatile tools to have in a broker’s portfolio. Whether your clients are purchasing their first house or seeking a jumbo loan for investment purposes, AD Mortgage has you covered.