Conforming loan vs. Conventional loan – the difference between the two types might not be clear upfront. This article helps brokers understand the key parameters of these mortgages and match each option to the individual borrower scenario. Also, we explore non-conforming solutions and identify which loan files can benefit most from them.

Key Takeaways

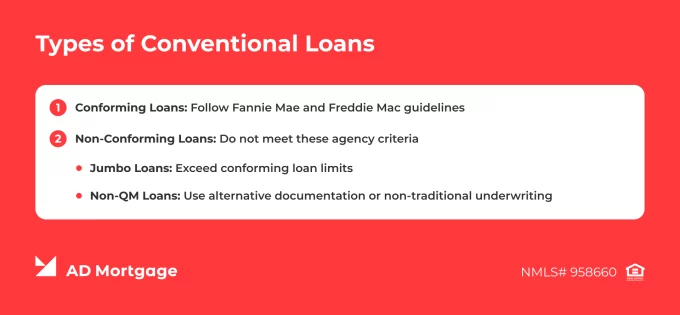

- Conforming and conventional loans are not the same. Conventional loans are non-government-backed loans that include conforming mortgages – loans that follow agency criteria.

- Conforming loans feature a standardized underwriting process and must fall within FHFA loan limits. Borrowers often choose these loans for lower pricing, wider availability, and traditional underwriting.

- Non-conforming loans are conventional loans that do not meet Fannie Mae and Freddie Mac guidelines. These include jumbo loans and Non-QM solutions. Borrowers may benefit from greater flexibility, more product options, and financing solutions for investment scenarios.

Is a Conforming Loan the Same as a Conventional Loan?

No, conventional and conforming loans are not interchangeable terms. Conventional loans are a broader category, which includes non-government-backed loans. Conforming loans are a subcategory of conventional loans, including those non-government-backed loans that meet the guidelines of Fannie Mae and Freddie Mac.

What Makes a Conventional Loan Conforming?

The conventional loan is conforming if it meets the following conditions:

- Agency Guidelines – The loan must follow Fannie Mae and Freddie Mac standards, which regulate eligibility and underwriting.

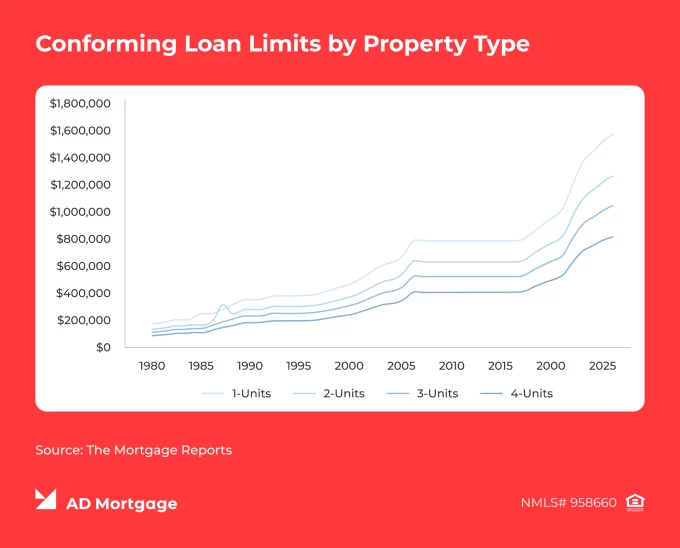

- Loan Limits – The loan amount must fit within limits set and updated annually by the FHFA, which vary by property type and county.

- Borrower Profile – The underwriting criteria must fit the applicable framework, and the borrower must meet acceptable thresholds for credit score, debt-to-income ratio (DTI), and documentation.

The loan limits are the most important factor, as they change each year, and it is important that your clients get the most up-to-date information. As of 2026, the conforming loan baseline for one-unit properties is $832,750 in most U.S. counties and $1,249,125 in high-cost areas.

What Makes a Conventional Loan Non-Conforming?

When a conventional loan does not meet agency criteria, it is considered non-conforming. Most often, that happens when the loan exceeds the conforming loan limit and becomes a jumbo loan.

However, non-conforming status is not only about limits. It can also include Non-QM scenarios with other qualification criteria or product characteristics such as:

- Credit profile issues (lower credit scores or recent credit events)

- Income complexity (freelancers, self-employed borrowers, gig workers, etc.)

- Occupancy types (second homes or investment properties)

- Loan structure (interest-only, DSCR loans, and other non-traditional features)

Therefore, non-conforming loans can provide greater flexibility for eligible, creditworthy borrowers. Brokers should carefully structure the loan in accordance with their client’s long-term goals and current capacity.

Conforming vs Non-Conforming: What Changes for the Borrower?

While both are conventional, conforming and non-conforming loans cover different borrower needs. Conforming loans are more standardized and offer more affordable financing for eligible borrowers. Non-conforming loans provide greater flexibility and therefore can be beneficial for people with non-traditional income, complex financial profiles, and investment goals.

| Conforming Loan | Non-Conforming Loan | |

|---|---|---|

| Loan Limits | Set annually by the FHFA. In 2026, 1-unit limit in most counties is $832,750 | No governmental limits, only lender overlays |

| Qualification Standards | Defined by agencies, more strict | Defined by lenders, more flexible |

| Down Payment | Minimum of 3% for first-time buyers and 5% for repeat buyers | Typically, 10%-25% |

| Reserves | Usually 2-6 months | Higher, may require 12+ months |

| Pricing | Lower rates due to lower risk and higher liquidity | Higher rates due to lack of agency backing |

| Product Flexibility | Standardized product options | Greater variability, including interest-only, DSCR, Non-QM, or investor-focused programs |

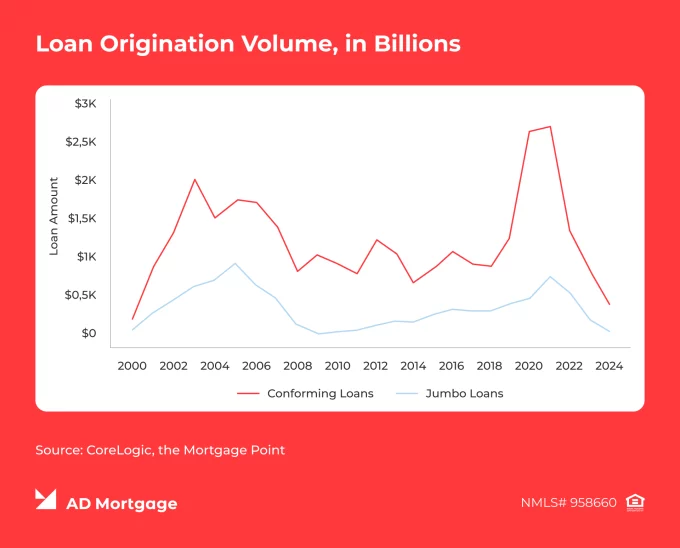

Jumbo Loans and Why They Matter Here

Jumbo loans are the most obvious examples of non-conforming loans. They exceed the conforming limits, but the key difference is not in pricing itself – it is in different underwriting rules.

Typically, jumbo loans feature tighter requirements, including more careful profile review, higher down payments and reserves, and stricter qualification guidelines. Brokers should clearly state this point: jumbo loans do not just fall outside conforming limits; they also follow a different underwriting process.

Which Borrowers Fit Conforming Conventional Loans Best?

Which clients should you match with conforming programs? These five cases can benefit most from conforming solutions:

- Borrowers who fall within local conforming limits

- Borrowers with strong credit and low debt-to-income ratios

- Borrowers with standard W-2 income and documented assets

- Borrowers seeking a standard, straightforward agency-eligible loan

- Borrowers looking for widely available agency-backed financing

Which Borrowers May Need a Non-Conforming Solution?

While conforming loans are more standardized and fit a broad audience, non-conforming loans are a more flexible option for borrowers whose profiles fall outside agency guidelines. The list below breaks down the most common best-fit scenarios:

- Borrowers whose loan amounts exceed conforming loan limits

- Borrowers with more complex income or asset profiles

- Borrowers needing more customized solutions

- Borrowers whose scenarios fall outside standard agency eligibility

Conclusion

How can brokers easily explain the difference between conventional, conforming, and non-conforming loans? Conventional is the broader category that includes a conventional subset that fits agency rules, and non-conforming loans are those that fall outside those rules.

Visit our Conventional Loan program page to find the solution that fits your client’s profile best. If you need any help with matchmaking, submit a loan scenario – and receive a tailored solution within 30 minutes.

FAQ: Conforming Loan vs Conventional Loan

Is a Conforming Loan a Conventional Loan?

Yes & No. Conventional loans are all non-government-backed loans, and conforming loans are a subset of them that meet Freddie Mac and Fannie Mae guidelines. All conforming loans are conventional loans, but not all conventional loans are conforming.

What is a Conforming Loan?

Conforming loans are non-government-backed loans that fall within Fannie Mae and Freddie Mac guidelines.

What is a Non-Conforming Loan?

Non-conforming loans are conventional loans that do not meet agency criteria, such as jumbo loans and Non-QM solutions.

What is the Difference between Conforming and Conventional?

Conventional loans are a broader category that includes loans not backed by government agencies. Conforming loans are a subset of conventional loans and meet agency criteria.

What Makes a Loan Non-Conforming?

A non-conforming loan is a conventional loan that does not meet agency criteria because it exceeds loan limits, allows a wider range of property types, features more flexible underwriting guidelines, or meets other exceptions.

Is a Jumbo Loan a Non-Conforming Loan?

Yes. Jumbo loans exceed conforming loan limits and follow different underwriting criteria.

What is the 2026 Conforming Loan Limit?

The 2026 conforming loan limit for one-unit properties in most counties is $832,750, and the high-cost-area ceiling is $1,249,125.

Are Conforming Loans Easier to Qualify for than Non-Conforming Loans?

Generally, no. While conforming loans have stricter credit score and income requirements, non-conforming loans feature more flexible qualification criteria. However, non-conforming loans might require a higher down payment and higher overall costs.

Can a Conventional Loan be Non-Conforming?

Yes. For example, jumbo and Non-QM loans are conventional and non-conforming.

Why Do Brokers Care about Conforming Loan Limits?

Exceeding conforming loan limits moves the loan into jumbo territory, completely changing the loan structure and the underwriting process.

Choose among 20+ programs and getLooking for a suitable loan program?

a detailed loan calculation