Often, the discussion around conventional loan credit scores is limited to the 620 threshold. However, there are many nuances beyond this number that brokers should explain to their clients to help them set realistic expectations and structure appropriate loan scenarios.

Key Takeaways

- While 620 is a common baseline for conventional loans, it does not guarantee favorable pricing and terms. 620-score files usually require more detailed underwriting, which can lead to longer timelines and potential lender overlays.

- Higher credit scores generally provide greater flexibility, smoother approvals, lower PMI, and better pricing. In some cases, taking time to improve a credit score may be worthwhile.

- When comparing conventional loans with FHA or Non-QM options, brokers should consider the total cost of the loan. Conventional loans can be more affordable in the long run, especially for borrowers with stronger credit profiles.

What is the Minimum Credit Score for a Conventional Loan?

Lenders typically require a minimum credit score of 620 for conventional loans. However, some programs, including jumbo loans or loans with manual underwriting, may require higher scores or impose stricter eligibility rules.

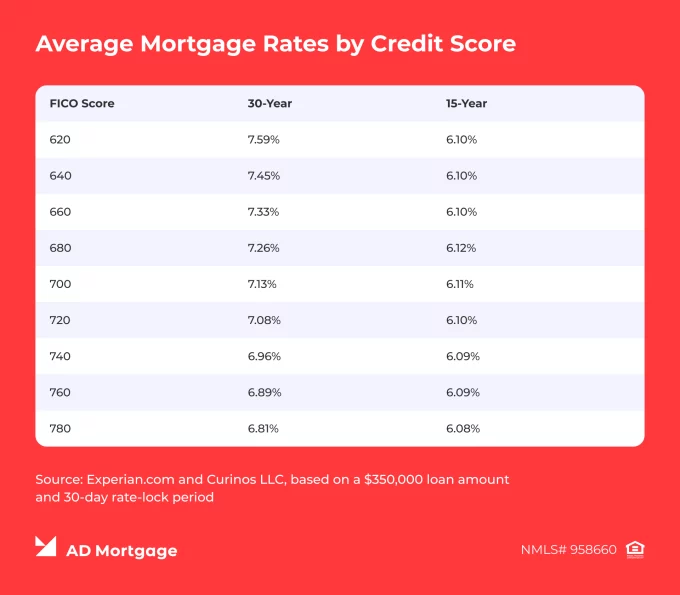

The following chart shows how credit scores can affect rates based on rates sources from Experian.com on March, 2026.

Is 620 Enough for a Conventional Loan?

Yes, 620 meets the baseline for conventional loans, but it does not guarantee smooth approval or the best pricing. Borderline scores may trigger manual underwriting, additional reviews, or delays.

Stronger credit generally leads to better rates and loan terms and positions borrowers as well-qualified rather than just eligible.

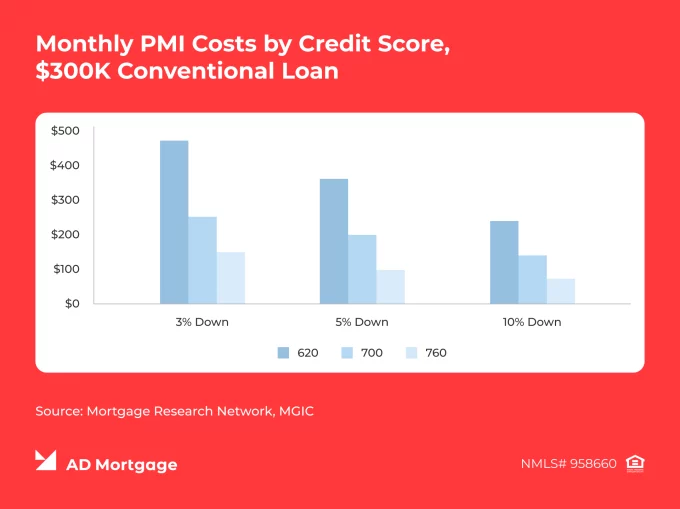

How Credit Score Affects Pricing, PMI, and Flexibility

Stronger credit scores influence multiple aspects of a loan. They generally support better pricing, lower PMI rates, quicker and smoother applications, and greater overall file flexibility.

Lower scores can still qualify, but borrowers may face more friction and less favorable terms. Brokers should help clients understand how credit affects these factors and whether improving their score is worth the potential benefits.

What Else Matters Besides Credit Score?

The most important idea to communicate is that credit score is not the only factor. Loan files are evaluated as a whole, and the following variables are closely considered:

- Down Payment

- DTI

- Income Stability

- Reserves and Assets

- Occupancy

- Property Type

- Underwriting Method

Conventional vs FHA vs Non-QM Credit Score Requirements

Conventional, FHA, and Non-QM loans do not have universal minimums. Instead, credit score requirements vary by lender and program. The table below outlines common thresholds and can serve as a starting point for brokers and their clients.

| Loan Type | Credit Score Requirements | Considerations |

|---|---|---|

| Conventional Loan | Typically 620+ | Higher score results in better pricing and terms |

| FHA Loan | Typically 580+ with 3.5% down and 500-579 with 10% down | Pricing tends to be more consistent across different credit scores |

| Non-QM Loan | Typically 620+ | Lower scores may be considered with strong compensating factors |

When a Borrower Has No Credit Score or Limited Credit

Most conventional loans rely on traditional credit scores for AUS approvals. No-score or limited-score profiles are not typical for standard conventional execution. Many of these files need separate handling – such as manual underwriting or alternative credit documentation.

These cases should not be confused with 620 baseline cases. Files with 620-score are established for conventional scenarios, while no-score files are evaluated under different criteria.

For borrowers with no or limited credit, brokers should carefully select the lender and structure the loan accordingly, setting realistic expectations around more complex underwriting and potentially less favorable terms.

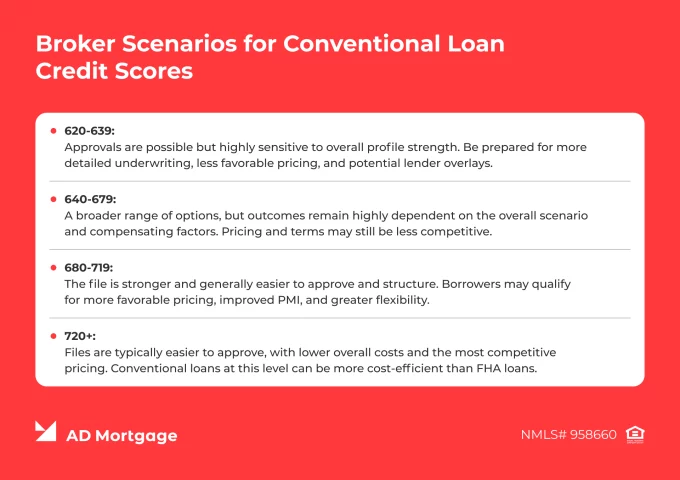

Broker Scenarios: How to Explain Score Ranges

Clients can often get lost in conventional loan credit requirements. This short breakdown helps guide borrowers through the nuances and set clearer expectations:

- 620-639: At this entry level, approvals are possible but highly sensitive to overall profile strength. Borrowers should be prepared for more detailed underwriting, less favorable pricing, and potential lender overlays.

- 640-679: Borrowers gain access to a broader range of options, but outcomes are still highly dependent on the overall scenario and compensating factors. Pricing and terms may still be less competitive.

- 680-719: The file is stronger and generally easier to approve and structure. Borrowers may qualify for more favorable pricing, improved PMI, and greater flexibility.

- 720+: At this top-tier level, files are typically easier to approve, with lower overall costs and the most competitive pricing. In many cases, conventional loans at this level can be more cost-efficient than FHA loans.

Conclusion

For over 20 years, AD Mortgage has supported our partners and offered them a wide range of mortgage programs. Visit our Conventional loan program page to choose the solution that matches your client profile best.

FAQ: Conventional Loan Credit Score Requirements

What is the Minimum Credit Score for a Conventional Loan?

The commonly cited conventional loan minimum credit score is 620. It may be enough for approval, but not necessarily for favorable pricing or terms.

Can You Get a Conventional Loan with a 620 Credit Score?

Yes. However, these borderline files often require closer review and may result in less favorable terms.

Is 640 a Good enough Credit Score for a Conventional Loan?

Conventional loan 640 credit score can provide access to a wider range of programs, but pricing is typically not optimal. Scores of 680+ often lead to more favorable terms.

Does a Higher Credit Score Lower PMI on a Conventional Loan?

Yes. PMI costs can vary widely – usually between 0.3% and 1.5% annually. Also, higher credit scores generally help reduce the cost.

Is FHA Easier to Qualify for than Conventional?

Typically, yes, due to more flexible credit requirements. However, FHA loans may result in higher long-term costs, especially for borrowers with strong credit profiles.

Can You Get a Conventional Loan with No Credit Score?

In some cases, yes. However, this usually requires additional documentation, alternative credit, and closer underwriting review.

Does Manual Underwriting Require a Higher Score?

Not necessarily. However, manual underwriting typically involves stricter overall requirements.

What Matters More than Credit Score for a Conventional Loan?

Factors like down payment and DTI ratio can be equally or even more important, as they directly reflect the borrower’s ability to repay the loan.

Choose among 20+ programs and getLooking for a suitable loan program?

a detailed loan calculation