Post content:

Brokers often compare conventional loans to FHA loan programs when choosing the solution that best matches a borrower’s needs. What is the real difference between these two options?

The common answer to this question is that FHA loans are government-backed and more flexible for borrowers with lower credit scores or higher debt levels. Whereas conventional loans are not government-backed and often fit borrowers with stronger credit profiles better. However, this perception is an oversimplification. Matching a borrower to the right mortgage solution requires reviewing their full financial profile, rather than relying on just a few variables.

Key Points

- Both conventional and FHA loans are valuable solutions for brokers to have in their portfolios. They serve different types of borrowers and both have their advantages and drawbacks.

- FHA loans typically require a credit score of 500-579 with a 10% down payment, or 580 and above with a 3.5% down payment, and include upfront and ongoing Mortgage Insurance Premiums (MIP), often for the life of the loan.

- Conventional loans generally accept DTIs up to 43%-45% and credit scores starting at 620, with higher scores resulting in better terms and pricing. The down payment can range from 3% to over 20%, and PMI is cancelable once 20% equity is reached.

Conventional Loan vs FHA: Quick Answer

The choice between conventional and FHA loans should be based on the borrower’s full financial profile, long-term goals, and current risk factors. While the ‘high credit score = conventional, low credit score = FHA’ logic is common, it is too basic of an approach for this complex decision. Further in the article, we explore FHA vs. conventional loans in detail.

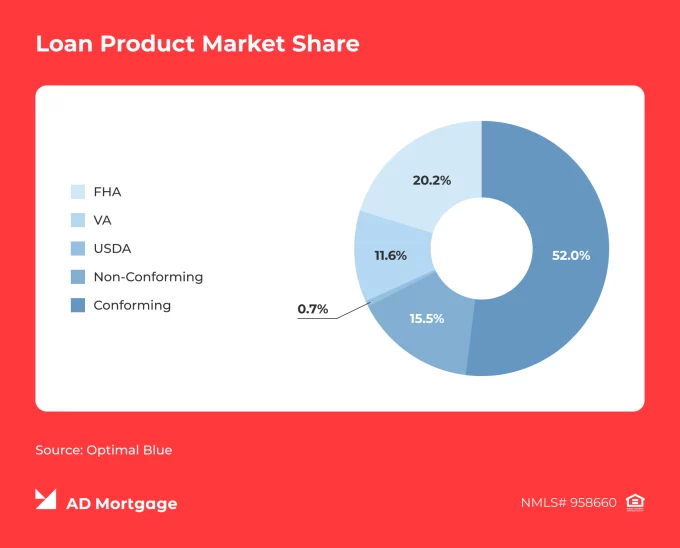

What is a Conventional Loan?

Conventional loans are non‑government‑backed mortgages issued and serviced by private mortgage lenders, credit unions, or banks.

There are two types of conventional loans.

Conforming loans follow the guidelines set by Fannie Mae and Freddie Mac and are therefore more liquid in the secondary market. Non‑conforming loans do not comply with these guidelines, often due to higher loan limits.

Overall, conventional loan terms and requirements vary by lender but often include a credit score of 620 or higher, debt-to-income (DTI) ratios under 43%-45%, and at least three months of reserves. In the long run, they may come with lower overall costs and more flexible conditions compared with government-backed loans.

What is an FHA Loan?

FHA loans are mortgages issued by private lenders but backed by the federal government and insured under the Federal Housing Administration (FHA) guidelines.

Due to government backing, FHA loans are less risky for lenders. For this reason, they are more accessible to borrowers and typically require a smaller down payment and lower credit score. However, they can be more expensive over the life of the loan because of higher mortgage insurance costs and, in some cases, slightly higher interest rates.

Side-by-Side Comparison Table: FHA vs Conventional Mortgage

As with most mortgages, requirements vary by lender and program. There is also no single ‘best option’ or ‘right choice’ for everyone as each loan type suits different borrower situations.

We have compiled common guidelines in this comparison table to make a broker’s job easier. You can also share it with clients to clearly explain the key differences between these two types of loans.

| FHA Loan | Conventional Loan | |

|---|---|---|

| Minimum Credit Score | Typically 580+ (500-579 with 10% down) | Typically 620+ |

| Down Payment | 3.5% (580+), 10% (500-579) | 3%-20%+ |

| Mortgage Insurance | MIP, often for the life of the loan | PMI required if <20% down, cancelable at 20% equity |

| Debt-to-Income Ratio | Up to 50% with compensating factors | Typically, 43%-45% |

| Appraisal | FHA-specific appraisal, including property condition standards | Standard home appraisal |

| Occupancy | Primary residence only | Primary, second, or investment properties |

| Loan Limits | Vary by county | Conforming loan limits set by Fannie Mae/Freddie Mac, higher for jumbo loans |

| Long-Term Costs | Can be higher due to ongoing MIP and possibly higher interest rates | Can be lower if PMI is canceled and interest rate is favorable |

| Refinance Options | Standard and streamline refinance with reduced documentation requirements | Standard refinance (rate-and-term, cash-out) |

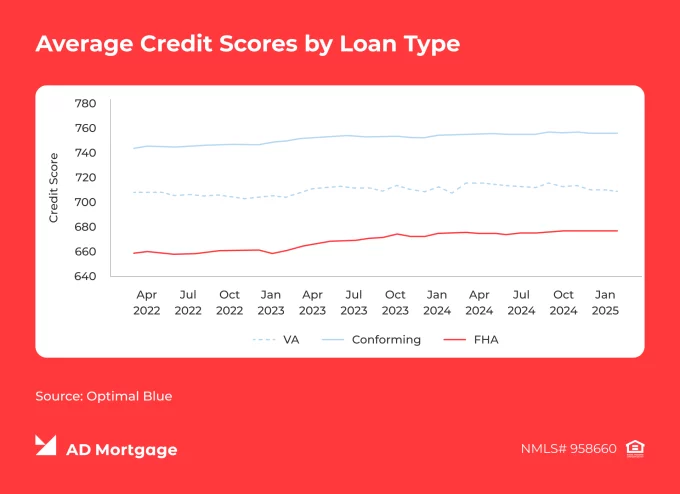

Credit Score and Qualification Flexibility

FHA vs. conventional credit score requirements can be difficult to compare, as these loan types follow different approaches.

Conventional loans are generally more sensitive to credit scores. While lenders often accept FICO scores as low as 620, higher scores help borrowers achieve better pricing. In addition, lower scores may still be accepted if strong compensating factors are present.

FHA loans require a minimum score of 580 for 3.5% down and 500-579 with 10% down. However, they are more consistent in pricing, even for borrowers with lower credit scores.

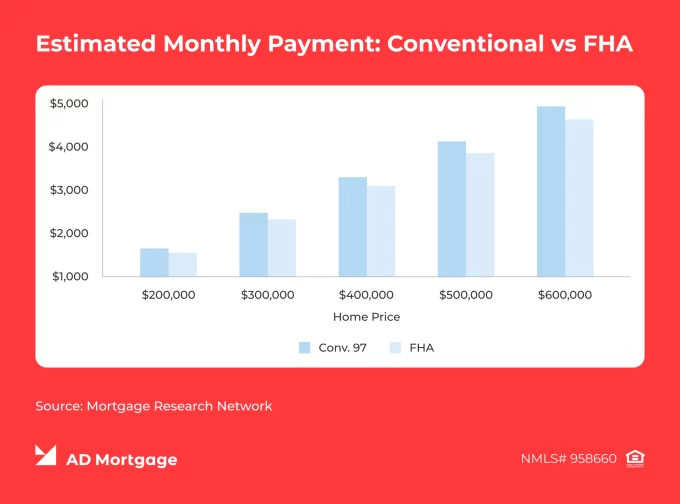

Down Payment Differences

Minimum down payment requirements for conventional loans can vary significantly depending on the borrower’s profile. High-credit-score, low-DTI borrowers can put as little as 3% down for a first-time home purchase and 5% for a repeat purchase. However, a higher down payment of 5%-20% may be required for borrowers with weaker credit profiles. Borrowers who put down more than 20% are typically exempt from paying Private Mortgage Insurance (PMI).

FHA loans require a minimum down payment of 3.5% if the credit score is 580 or higher. For credit scores between 500 and 579, a higher down payment of 10% is needed.

Despite the lower down payment requirements, FHA loans should not automatically be considered cheaper than conventional mortgages. Down payment is only one piece of the picture – mortgage insurance and other factors also need to be carefully reviewed when making a decision.

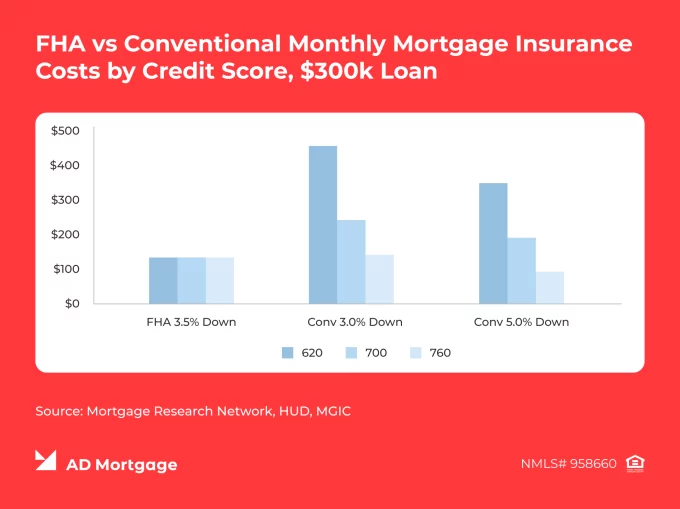

Mortgage Insurance: PMI vs MIP

Both conventional and FHA loans include mortgage insurance, but in different forms:

- Conventional loans require Private Mortgage Insurance (PMI) when the down payment is less than 20%. PMI costs vary based on the borrower’s profile and lender overlays, and the insurance can be removed once the borrower reaches 20% equity upon request. It is automatically canceled when the loan reaches 22% equity.

- FHA loans include both upfront and ongoing Mortgage Insurance Premium (MIP). The upfront MIP is typically 1.75% of the loan amount and can be financed into the loan. The ongoing MIP amount depends on the loan scenario and is paid monthly for the life of the loan when the down payment is less than 10%, or for at least 11 years if the down payment is 10% or more.

This is often the point at which many higher-credit borrowers shift toward conventional loans, even if FHA appears more accessible upfront. Brokers should highlight mortgage insurance costs early to help set realistic expectations and guide borrowers toward the most cost-effective option.

DTI and Overall Approval Flexibility

Conventional loans typically allow Debt-to-Income (DTI) ratios of 43%-45% – however, some lenders accept up to 50% with strong compensating factors. FHA loans allow DTIs up to 50% or higher, provided the profile is strong and clean.

Overall, FHA loans usually work better for borderline qualification scenarios, while conventional loans perform better when the borrower is financially stable and looking to optimize pricing.

Property Standards, Occupancy, and Use

The two loan types approach property standards differently. Conventional loans focus on market value and overall condition, while FHA loans are stricter, emphasizing safety and livability.

In terms of occupancy, conventional loans allow primary residences, second homes, and investment properties, providing complete flexibility. FHA loans are limited to primary residences only.

As a result, conventional loans offer more flexibility and can create opportunities for investment, whereas FHA loans are best suited for primary residences.

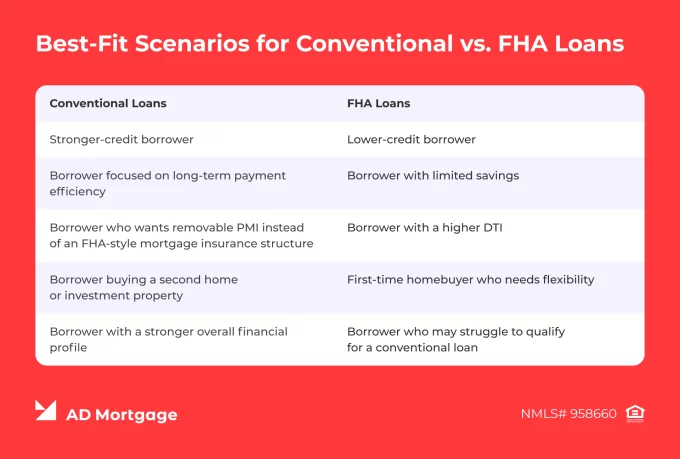

Which Borrowers Fit FHA Best?

FHA loans are great for clients who want to qualify now, rather than saving money in the long run. Below are borrower scenarios that might benefit from FHA solutions. Do you have any clients like these?

- Lower-credit borrower

- Borrower with limited savings

- Borrower with a higher DTI

- First-time homebuyer who needs flexibility

- Borrower who may struggle to qualify for a conventional loan

Which Borrowers Fit Conventional Best?

Conventional loans are best suited for borrowers who already qualify comfortably and want to optimize long-term costs and loan structure. The following scenarios benefit the most from this option:

- Stronger-credit borrower

- Borrower focused on long-term payment efficiency

- Borrower who wants removable PMI instead of an FHA-style mortgage insurance structure

- Borrower buying a second home or investment property

- Borrower with a stronger overall financial profile

Bottom Line: Which Loan is Better?

There is no single ‘better’ version in a conventional vs. FHA comparison – it depends on the borrower’s profile and goals.

FHA loans can be a great choice when qualification is the priority, as they allow borrowers with lower credit scores or weaker financial profiles to qualify.

Conventional loans are often the better fit for borrowers with stronger profiles who want lower long-term costs or more flexibility with property types.

Check Out Our Conventional and Government Promo

Whether you choose conventional or government solutions, AD Mortgage knows that every basis point matters. That is why we offer improved pricing for our partners: 25 bps off all Conventional and Government Purchase Loans for every lock date from April 1 through May 31.

How can approved partners lock the promo rate?

- Log in to the AIM Partner Portal

- Lock an eligible Conventional or Government Purchase loan through May 31

- Done – the improved pricing applies automatically

Conclusion

Don’t know which mortgage solution will be most beneficial for your client? Submit a loan scenario, and AD Mortgage’s experts will reach out within 30 minutes with a tailored loan program.

FAQ: Difference Between FHA and Conventional Loan

Is FHA Easier to Qualify for than Conventional?

Often, FHA loans are easier to qualify for, thanks to lower down payment and credit score requirements. However, they may come with higher overall costs compared with conventional loans.

Is FHA or Conventional Better for First-Time Buyers?

First-time homebuyers with lower credit scores may prefer FHA loans, which allow a 3.5% down payment and generally offer quicker qualification. Borrowers with higher credit scores might choose conventional loans, which can require as little as 3% down and offer lower mortgage insurance costs over time.

Do Conventional Loans Always Require 20% Down?

No. First-time homebuyers can qualify for a conventional loan with a down payment as low as 3%, and repeat buyers can qualify with as little as 5% down.

Which is Cheaper Long-Term: FHA or Conventional?

Generally, conventional loans are more cost-effective for borrowers with strong credit profiles, primarily due to cancelable PMI. However, FHA loans may be more beneficial for borrowers with lower credit scores, as they offer more flexible qualification requirements and lower minimum down payments.

Do Sellers Prefer Conventional over FHA?

FHA loans require a more detailed appraisal that often takes more time, so sellers generally prefer buyers using conventional loans.

Is FHA Better for Low Credit Scores?

Usually, yes. FHA loans accept credit scores as low as 500 with a 10% down payment, compared to 620 or higher for conventional loans.

Can You Buy an Investment Property with FHA?

No. FHA loans are limited to primary residences only.

When Should a Borrower Refinance from FHA to Conventional?

When a borrower reaches 20% equity, refinancing into a conventional loan allows them to cancel FHA mortgage insurance costs. Additionally, if their credit score has increased to 620 or higher, they may qualify for better interest rates and overall pricing.

Looking for a suitable loan program?

Choose among 20+ programs and get

a detailed loan calculation

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again