Post content:

Michigan has one of the most active mortgage markets in the country. For anyone looking to build a career in the industry, becoming a mortgage loan originator (MLO) is a strong place to start.

The licensing process in Michigan takes several months when everything goes right. Yet, one missed form or skipped deadline can stretch that timeline considerably while costing you real money. But you won’t be going through this alone. AD Mortgage put together this guide to walk you through every step and fee, so you know what’s coming next.

ADD US AS A PREFERRED SOURCE ON GOOGLE

Why Becoming a Michigan MLO is a Good Decision

Before walking through the paperwork, it is worth asking whether this career makes sense in Michigan specifically. Few states offer a stronger home-field advantage – here is why.

“The new meaning of Motown is Mortgage Town. With so many large lenders here, the future of industry innovation and direction is being shaped right in this state,” says Eric Clark, VP TPO Account Executive at AD Mortgage. “For anyone with career aspirations in management, there’s a ton of opportunity to grow and build invaluable skills in its most pivotal role: working with the borrower, where you learn all the fundamentals of the mortgage industry.”

Eric is not the only one who’s seen this firsthand. Brennen Moloney, SVP Business Development of AD Mortgage, shares his experience of starting his career as an MLO in Michigan several years ago:

“Working directly with borrowers gave me the sales, emotional intelligence, and communication skills to succeed in later chapters of my career. What I love about this industry is that there are many ways to succeed, depending on your strengths – some people are naturally good at math, others are better at relationship building. If you play to your strengths, you’ll be able to find success!”

Eric and Brennen built different careers, but they both point to the same thing: Michigan rewards persistence and a willingness to keep learning.

Michigan is the Mortgage Capital of the US

As Eric Clark mentioned earlier, Metro Detroit is home to some of the largest mortgage lenders in the country, and now – including AD Mortgage. Here, companies continuously hire and train MLOs. You can attend regular industry events and develop a professional network quickly. You’ll be building a career in the state where much of the modern mortgage industry is run.

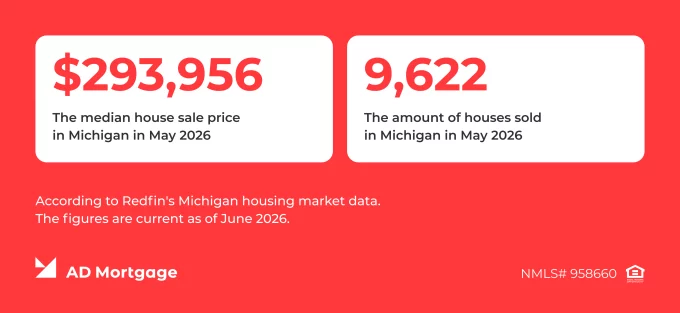

The housing market supports the case as well. Redfin’s Michigan housing market data put the median sale price at $293,956 in May 2026, up 5.4% year over year, with 9,713 homes sold that month. The state represents a combination of steady price growth and an affordable base. Buyers here can still realistically transact, and nearly all of them need financing to do it.

Salary of the Mortgage Loan Officer in Michigan

Salary is usually the first question, so here are the numbers.

For employed MLOs, Salary.com data for Mortgage Loan Officer in Michigan (entry-level, <1 years of experience) shows a median annual base salary of $50,114 as of June 1, 2026, with the top 10% earning above $59,790. Base pay, however, is only part of the picture in this profession. Many originators earn most of their income on commission.

According to Glassdoor data (based on 681 self-submitted salaries for Michigan as of April 2025), mortgage loan officers with less than one year of experience earn between $71,000 and $123,000 per year, including base pay and bonus. More experienced MLOs, with 4 – 6 years in the profession, earn roughly $87,000 to $156,000 annually.

Understanding the Terminology

People searching “how to become a mortgage broker in Michigan” usually mean either the individual license, or for a company. Let’s clarify the difference.

The individual license – the one that most readers want – is for a mortgage loan originator, often called a mortgage loan officer. This is the person who takes loan applications and negotiates terms for profit.

In Michigan’s legal framework, a mortgage broker can refer to either an individual or a company. But most commonly, it is the company that employs or contracts with originators.

Michigan Mortgage Loan Originator (MLO) License: Quick Facts

| Regulator | Michigan Department of Insurance and Financial Services (DIFS) – the agency that issues and oversees your license. |

| Licensing system | All applications run through the Nationwide Multistate Licensing System (NMLS). |

| Pre-license education | 20 hours of NMLS-approved coursework, two of which must cover Michigan law (NMLS state education requirements). |

| Exam | SAFE MLO National Test with Uniform State Content – Michigan has no exam of its own. |

| State application fee | $200 – 225 operating fee for the 2026 licensing year (DIFS fee schedule). |

| Total estimated cost | Approximately $600 – $1000. It covers the state fee, the $110 SAFE test, the $36.25 FBI background check, the $15 credit report, the NMLS processing fee, and a pre-licensure course ($200 – $400, varies by provider). |

| Renewal deadline | December 31 each year through NMLS, with continuing education completed first. Late renewals cost $25 a day, up to $1,000 (DIFS renewal requirements). |

| Governing statute | Mortgage Loan Originator Licensing Act 75 of 2009 – the legal foundation for everything in this guide. |

How to Receive Your MLO License in Michigan: Step by Step

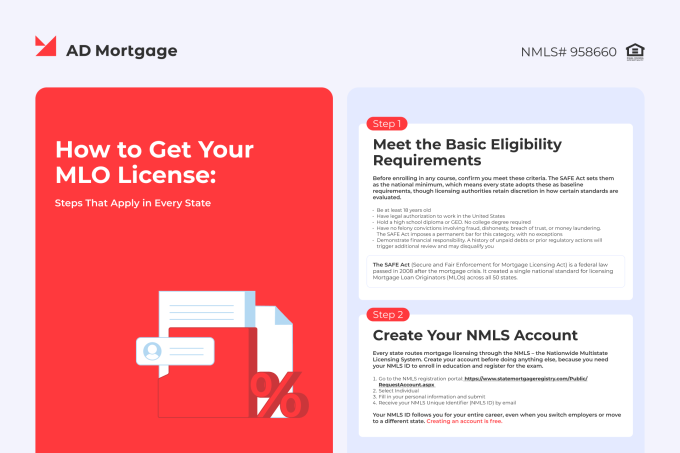

Federal Requirements

Every state shares the same federal baseline, so this section is brief:

- Create an NMLS account at the NMLS Resource Center

- Complete 20 hours of NMLS-approved pre-licensure education (PE)

- Pass the SAFE MLO Test (National Component with Uniform State Content)

- Submit fingerprints for an FBI criminal background check

- Authorize a credit report through NMLS

- Complete Form MU4 (Individual Form) in NMLS

- Obtain sponsorship from a licensed company to activate your license (your NMLS record must show you as “Authorized to Represent” your employer)

For a detailed walkthrough of each federal step, including deadlines and costs, download our complete MLO licensing guide.

Michigan MLO License Requirements

The following requirements are specific to Michigan and may not apply if you’re seeking licensing in another state.

1. Include two hours of Michigan-specific education in your 20 PE hours

Michigan requires that 2 of your 20 pre-licensure hours cover Michigan mortgage law, per the NMLS state-specific education requirements for Michigan. Most providers bundle this into their Michigan PE packages but confirm before you enroll. Also, be sure to note that a license lapsed for three years or more requires retaking the full 20 hours of education – this is required by SAFE Act.

2. No separate state exam

Michigan uses the SAFE MLO National Test with Uniform State Content, so passing the national exam satisfies the requirement – there is no standalone Michigan test component.

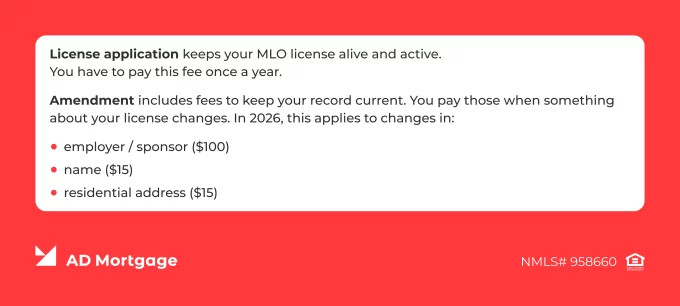

3. Pay the $225 Michigan operating fee

Per the DIFS fee schedule for the January 1 – December 31, 2026 licensing year, the license application operating fee is $225, paid through NMLS. Keep this PDF on hand – it also lists amendment fees, such as $100 for a change of employer or sponsor.

4. Secure a surety bond

A surety bond is a financial guarantee (not insurance for the broker) which protects consumers and the state if an MLO violates licensing rules or causes financial harm. If a valid claim is filed, the surety company pays out, but the MLO must then reimburse that amount in full.

Michigan requires every MLO to be covered by a surety bond. If your sponsoring employer’s company bond (Form FIS 2137) covers you, you’re all set. If not, you file an individual bond (Form FIS 2135). Note that in 2026, both forms just outline the requirements – the bond itself is submitted electronically through NMLS.

The bond amount is $10,000 for first-time applicants, rising to $25,000 once you close $12 million or more in loans in a calendar year, and $50,000 at $24 million or more.

5. Get sponsored by a Michigan-licensed employer

Your license remains in pending status until a licensed Michigan mortgage company sponsors you through NMLS. The sponsorship request comes from the employer, and DIFS reviews and approves it. Once approved, you are officially licensed and can originate Michigan loans.

If anything in your application raises questions, you can reach out to the DIFS Consumer Finance Licensing Unit at 877-999-6442.

Need to Renew Your MLO License?

Michigan MLO licenses expire every December 31, and renewal runs through NMLS. Per the DIFS renewal requirements, you must complete 8 hours of NMLS-approved continuing education (CE) before requesting renewal. Michigan does not require any state-specific CE hours – the standard 8-hour national course satisfies the requirement.

Michigan MLOs have access to two industry organizations that combine continuing education with networking and professional development:

1. MMLA (Michigan Mortgage Lenders Association)

MMLA is the exclusive trade group representing the interests of Michigan’s mortgage industry, founded in 1929. It’s an ongoing membership organization (similar to a trade union or chamber of commerce for this specific industry).

MMLA members receive a 25% discount on NMLS-approved CE and PE courses, as well as FHA/VA/USDA and compliance training, through the association’s education partner.

2. OCN (Originator Connect Network)

OCN is a company that organizes trade show-style conferences for mortgage industry professionals across the country. Each event combines an exhibit hall (banks, tech vendors, service providers), educational sessions, and networking.

At the Motor City Mortgage Expo in Detroit on June 19, 2025, hosted by OCN, attendees who completed the exhibit hall passport earned entry to a free NMLS renewal class – and AD Mortgage was on site connecting with Michigan brokers. Similar events take place in the state each year.

How to Receive a Mortgage Brokerage License in Michigan

For originators planning to open their own firm, a brokerage is a separate company-level license under the Mortgage Brokers, Lenders, and Servicers Licensing Act 173 of 1987, and the most common starting point is the 1st Mortgage Broker License. The key steps:

- Form your business entity and create a company (Form MU1) record in NMLS.

- Pay the fees set in the DIFS fee schedule under the MBLSLA – a $700 broker operating fee plus a $450 investigation fee (broker-and-lender authority is $1,000, and broker-lender-servicer is $1,500).

- Meet the surety bond requirement that applies to your license type and activities, and proof of financial stability (a minimum Net Worth Of $25,000) – bond forms and details are available on the DIFS mortgage licensing page.

- Have at least one licensed and sponsored Michigan MLO on staff to originate, and provide DIFS with the required disclosures about your control persons and any other professional licenses they hold.

- Renew annually – per the DIFS 1st Mortgage FAQ, company licenses expire December 31 and must be renewed on or before December 15, with annual financial statements due within 90 days of year end for brokers.

The company license involves more documentation than the individual license, but for originators with a solid book of business, it is a well-established path.

FAQ: Become a Mortgage Loan Officer in Michigan

What's the difference between a mortgage loan officer and a mortgage broker in Michigan?

Michigan law treats mortgage loan officers and mortgage brokers as entirely separate categories.

A mortgage loan officer, formally a mortgage loan originator (MLO), is an individual who works directly with borrowers, taking applications and negotiating loan terms. This is a personal license, tied to one specific person, and it’s governed by the Mortgage Loan Originator Licensing Act (MLOLA) 75 of 2009.

A mortgage broker, on the other hand, usually refers to the business entity (legally, it can also refer to the individual, though less commonly) – the company an MLO works for or is sponsored by. Broker licenses are issued to firms, not individuals, under a different statute: the Mortgage Brokers, Lenders, and Servicers Licensing Act (MBLSLA) 173 of 1987. So if you’ve been researching “how to become a mortgage broker,” what you’re actually pursuing most of the time is the individual MLO license. The company-level broker license comes into play only if you eventually own or operate a brokerage yourself.

How long does it take to become a mortgage loan officer in Michigan?

The timeline depends on how quickly you move through each required step. Most candidates complete the process in about 6 to 14 weeks, though some move faster. You’ll need to finish 20 hours of NMLS-approved pre-licensing education (commonly done in 4 to 14 days), pass the SAFE MLO exam, and clear a background check and credit report through NMLS.

From there, your application sits in pending status until a sponsoring employer confirms your affiliation in NMLS. That step is often the biggest wildcard, since it depends entirely on your employer’s timing. Once everything is submitted and verified, DIFS typically processes applications within one to two weeks.

How much does a Michigan MLO license cost?

Expect approximately $600 – $1000 in total: the $200 – 225 state operating fee, the $110 SAFE test, the $36.25 FBI background check, the $15 credit report (NMLS fee schedule), the NMLS processing fee, and a pre-licensure course that typically costs $200 – $400 depending on the provider.

Do I need a college degree to become an MLO in Michigan?

No. There is no degree requirement. You need the 20 hours of pre-licensure education, a passing score on the SAFE test, and clear background and credit checks.

Does Michigan have its own licensing exam?

No. Michigan uses the SAFE MLO National Test with Uniform State Content, so one national exam covers the requirement. You do, however, need 2 hours of Michigan-specific content within your 20 education hours.

Do I need my own surety bond?

Only if your sponsoring employer’s company bond does not cover you. In that case, you file an individual bond (Form FIS 2135) – $10,000 for first-time applicants – electronically through NMLS.

When do I renew my Michigan MLO license?

Every year through NMLS, with all 8 CE hours completed before you submit. DIFS asks that renewals be received by December 15 (a recommended deadline). The actual legal cutoff is December 31. Renewals requested after December 31 incur a $25-per-day late penalty, up to $1,000.

Conclusion

Becoming a licensed MLO in Michigan is an achievable goal. The first concrete step is opening your NMLS account and enrolling in a Michigan-approved course. Everything else follows from there.

Once you are licensed, where you place your business matters as much as the license itself. AD Mortgage works with Broker Partners nationwide as a wholesale lender, offering a full range of programs – Conventional, FHA, and a complete Non-QM lineup. We back it all with the technology and support new originators need to close more loans.

Last reviewed: June 2026. Not legal advice. Licensing requirements and fees are subject to change. Always verify current requirements directly with the Michigan Department of Insurance and Financial Services and the NMLS Resource Center before beginning your application.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.