What happens with the loan file on the lender’s side? Neil Childs, Operations Lead at AD Mortgage, breaks down the process step by step and shares tips for brokers on how to close loans efficiently. Together with Serena Diaco, AD Mortgage Sales Trainer, they discuss mortgage workflow, common issues, and process nuances.

Disclosure: Base Point of the Mortgage

The lender begins working on the loan upon receiving a completed Loan Application (LA) from the broker or directly from the borrower. Under TRID requirements, the Loan Estimate (LE) and other initial disclosures must be provided to the borrower within three business days, setting the basis for the entire mortgage process.

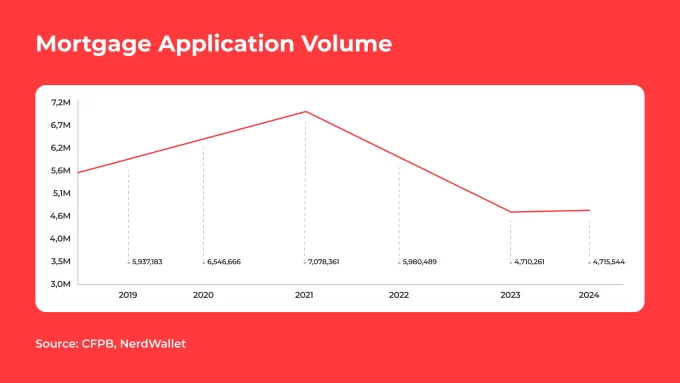

From 2019 to 2024, the number of applications dropped mainly because of dramatic interest rate growth in 2022. However, the share of approvals and denials stayed at the same levels, and in 2024, accounted for 71% and 8%, respectively.

Neil highlights what brokers should pay close attention to:

‘I think the biggest key point when submitting a file is making sure we have all our fees accurate, that we’re disclosing everything accurately.’

Underwriting: Loan Decision Process

After the borrower acknowledges the disclosures, the file moves to underwriting, where the lender carefully reviews the profile and assesses whether the loan meets guidelines. The factors evaluated depend on the loan type and lender’s requirements, but typically include:

- Credit score, history, and overall creditworthiness

- Income stability and the debt-to-income ratio

- Employment history

- Assets, funds, and reserves

- Property value, marketability, and condition

As a result of the underwriting review, the lender issues a decision – which may be Approval, Suspended, or Denial – and conditions that the borrower must fulfil to secure the loan. Brokers should anticipate the lender’s requirements and act proactively to reduce condition cycles and avoid delays.

‘Making sure that we have as much information as possible is going to make the whole process go a lot smoother from an underwriting perspective.’

– Neil Childs

Closing: Culmination of the Mortgage

Closing is often seen by borrowers as the final stage of the mortgage. While this is not actually true and servicing continues long after, closing is in fact the execution point – it is the moment when the mortgage becomes a legally binding transaction.

On the lender side, the closing team prepares final documents, the main of which being Closing Disclosure (CD), and coordinates the process with the settlement or title agent. The borrower signs documents – in-person or online through eClosing – and the closing costs are covered according to requirements and agreements.

Among the most common issues during the closing process, Neil mentions rushes:

‘If we ever need a rush, we always want to make sure the borrower is ready and able to close. We see probably about half the time that we are getting rushes requested that perhaps the borrower isn’t even ready to close at that time.’

Post-Closing: Final Inspection

After the borrower signs, the lender verifies the signed package and then the loan is funded. However, the reviews do not stop there, as Neil explains:

‘The main goal with post-closing is to make sure we have a full file for delivery to either our investor or the agency.’

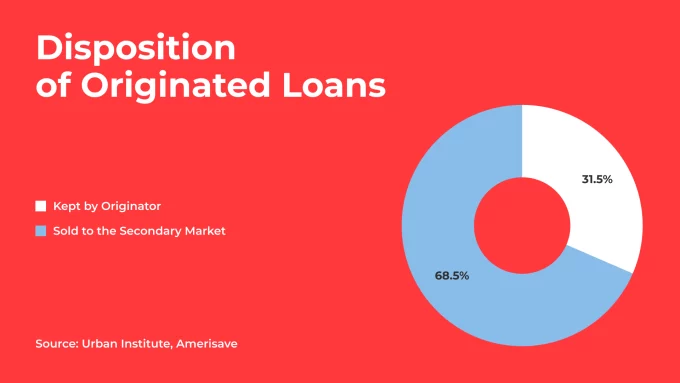

The Quality Control team checks that the loan is accurate, complete, and compliant. At this stage, the loan is prepared to be sold on the secondary market or kept in the lender’s portfolio. If the QC team misses defects like incomplete documents or unrecorded liens, the loan may be considered ineligible for sale, and the lender may be forced to buy it back.

Servicing: Handling the Mortgage

Servicing is the ongoing management of the mortgage, done by the originator or a third-party servicer. What does handling the mortgage actually mean? Typically, it includes the following functions:

- Collecting and processing payments, including principal, interest, taxes, and insurance

- Managing escrow accounts, distributing property taxes and homeowner’s insurance

- Handling borrower inquiries

- Monitoring delinquency and initiating loss mitigation or foreclosure when needed

- Reporting and issuing billing statements, annual tax forms, and other documents

Operations Team: Behind the Whole Process

The operations team supports other departments throughout the whole mortgage process. Neil highlights the importance of collaboration:

‘There’s a ton of coordination in the mortgage life cycle for the fulfillment process. What’s important is that we’re all on the same page. All our different departments within operations work together, and any changes we make are not impacting another group down the line.’

AD Mortgage is a mortgage lender that helps our partners win. Our teams bring a ‘can do’ attitude to every situation, ensuring you offer the best-fit solutions for your clients. Become a partner today for award-winning technology and lending solutions that move your business forward: