Post content:

Every loan you close has a mortgagee clause in the file. It shows up on title commitment, hazard and flood policies at processing, again when the loan is sold, and at every annual renewal after that. And there’s still no single standard that works everywhere.

In this guide, you will find key details about the mortgagee clause: the anatomy of each component, wording templates, underwriter insights on what causes rejections, and answers to the questions that come up most often at the desk.

ADD US AS A PREFERRED SOURCE ON GOOGLE

Why Brokers Get the Mortgagee Clause Wrong and What It Costs

The mortgagee clause is one of the most consistently mishandled items in the mortgage pipeline for several reasons:

- High Compliance Risk. Underwriters and post-closing quality control audit the clause rigorously. A rejection requires re-submission, which delays closing.

- Frequent Format Confusion. Abbreviations, Mortgage Electronic Registration Systems (MERS) notation, and servicer vs. investor naming are potential failure points that look invisible at first glance.

- Insurance / Title Company Agent Friction. Some agents don’t understand investor requirements or resist making corrections. A single call asking for a revision can take days to resolve.

- Post-Closing Servicing Transfers. When loans are sold to the secondary market, the mortgagee clause on the insurance policy may need to be updated. Some brokers don’t know whose job that is, or when it needs to happen.

Insurance errors are a common cause of closing delays, because lenders must make sure the policy meets investor requirements before the loan can be purchased.

Copy-paste ready AD Mortgage’s official mortgagee clause

What is a Mortgagee Clause?

A mortgagee clause is a provision that establishes an independent insurance contract between the property insurer and the loan owner – first the lender, later potentially an investor. Because the contract is independent, borrower or third party actions can’t cut off the loan owner’s coverage. Whether the borrower damages the property or disputes a title claim, the loan owner still gets paid.

You might also meet such terms as “standard mortgagee clause” or “union mortgagee clause” – these are synonyms.

While the mortgagee clause protects the investor or end beneficiary, it names the address of the servicer – the company that manages the loan and handles insurance documentation. Often, it’s the same institution, but servicers can change over the life of a loan. When that happens, the mortgagee clause needs to be updated on every document it appears on.

Is the Mortgagee Clause Just an Address?

No. The mortgagee clause is a legal mechanism with three functional components: the lender’s legal entity name, the ‘Its Successors And/Or Assigns’ (ISAOA)/ “As Their Interests May Appear” (ATIMA) designation, and the servicer’s mailing address. Each component serves a distinct legal purpose – we discuss it in detail in the Terminology section.

Important! When you receive an underwriting condition referencing the mortgagee clause, it sometimes looks like this:

“Mortgagee clause must be: A&D Mortgage, LLC ISAOA/ATIMA, PO Box 2807, Daytona Beach, FL 32120-2807 and must contain the loan #.”

The loan number here is a separate requirement. It needs to appear on the insurance policy, but it is not part of the mortgagee clause itself. So, if your condition is specifically about correcting the mortgagee clause, the loan number is most likely already correct and doesn’t need to be touched.

Instead, focus your review on the usual suspects: the lender name, entity suffix (LLC, N.A., etc.), ISAOA/ATIMA, and any spelling errors.

Mortgagee Clause for Title vs. Property Insurance Documentation

If you have chosen AD Mortgage and close loans with us regularly, you will need two different mortgagee clauses during the loan process.

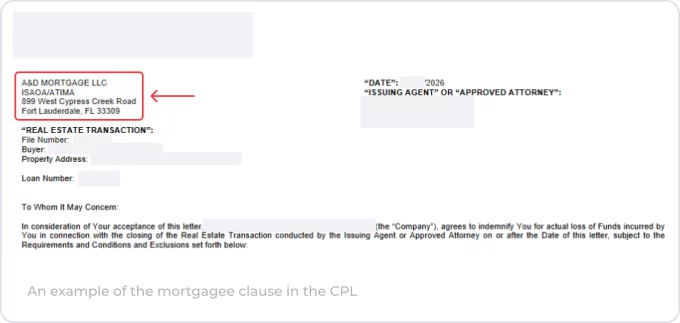

Title Documentation

Title insurance covers legal risks like liens, ownership disputes, or recording errors. These risks directly threaten the lender’s security interest in the property. The mortgagee clause names the lender as an insured party on the title policy, so if a title claim comes up, the lender has clear protection.

You will need to transfer the mortgagee clause to the title company representative to receive the title commitment and closing protection letter.

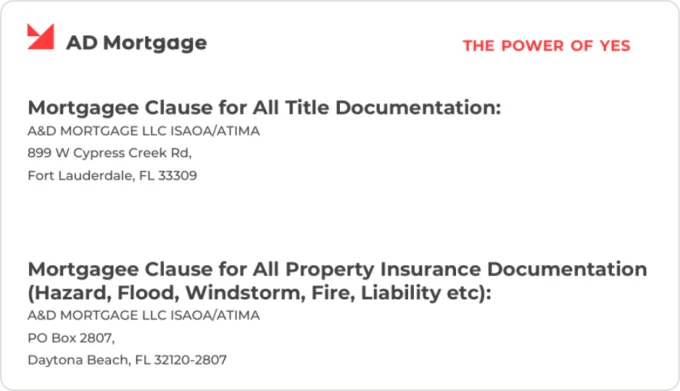

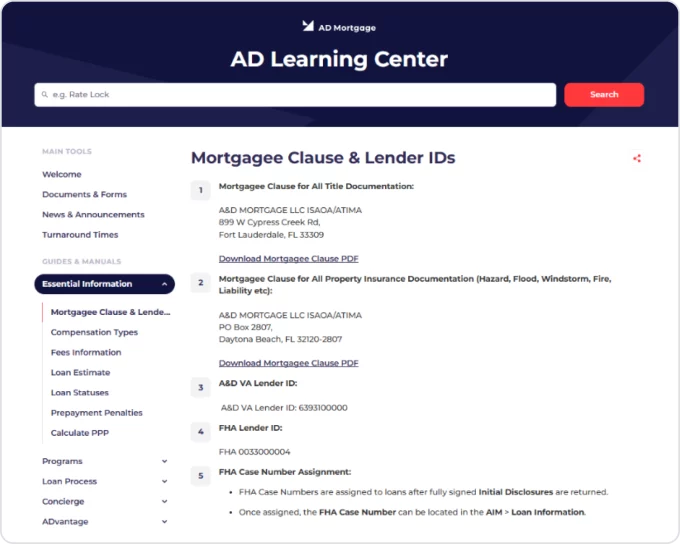

| Mortgagee Clause in AD Mortgage Title Documents |

|---|

| A&D MORTGAGE LLC ISAOA/ATIMA 899 W Cypress Creek Rd, Fort Lauderdale, FL 33309 |

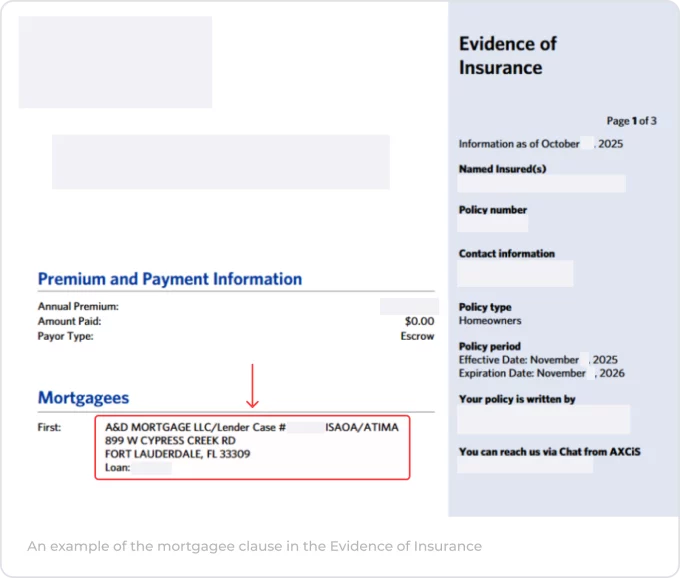

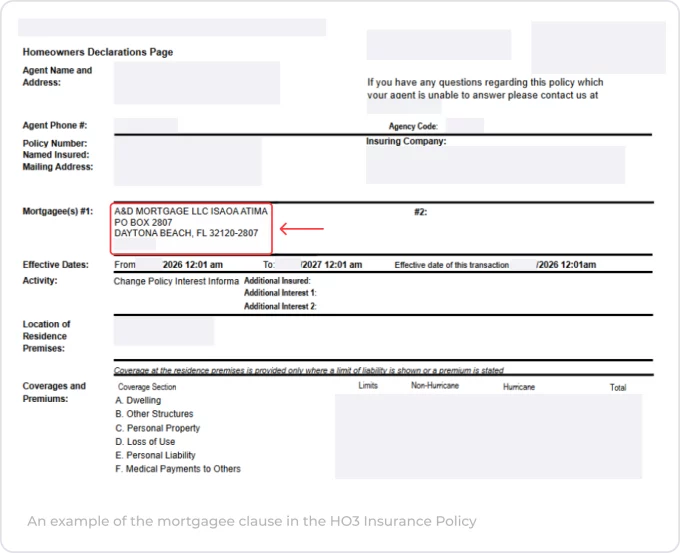

Insurance Documentation

While title documents cover legal risks, hazard, flood, and other policies address physical ones. Since these policies protect the collateral behind the loan, investors who buy loans from lenders require a mortgagee clause on all of them. That clause names the lender as an insured party and directs any payout to them if a covered loss occurs.

Without a correct mortgagee clause, the insurance company can deny that coverage entirely, which puts both the lender and the investors at risk. That’s why underwriters verify it thoroughly on every file.

The address on the mortgagee clause should match the servicer’s designated insurance correspondence address. For instance, it can be a P.O. Box set up specifically to receive insurance documents. Using the corporate headquarters or a branch address (without checking where the insurance correspondence is processed) is a common error.

| Mortgagee Clause in AD Mortgage Insurance Documents |

|---|

| A&D MORTGAGE LLC ISAOA/ATIMA PO Box 2807, Daytona Beach, FL 32120-2807 |

Mortgagee Clause Terminology

| Standard Format |

|---|

| [LENDER LEGAL ENTITY NAME], ISAOA/ATIMA [P.O. BOX OR MAILING ADDRESS] [CITY, STATE, ZIP CODE] |

The mortgagee clause follows the standard three-line U.S. address format (with slight variations): entity name on the first line, street address or P.O. Box on the second, and city, state, and ZIP code on the third. Technically, all of this information could appear on a single line, but three lines are the universally accepted convention, and insurance carriers expect it that way.

Components of the Mortgagee Clause

| Entity name | Identifies who holds the protected interest and ensures the correct party receives proceeds. |

| ISAOA, stands for “Its Successors And/Or Assigns” | Allows the lender to transfer its insurance rights to another institution when the loan is sold on the secondary market. |

| ATIMA, stands for “As Their Interests May Appear” | Extends the clause coverage to any party with a financial interest in the property, including the loan servicer and downstream investors, even if they are not explicitly named. |

| Address | Routes all insurance correspondence (cancellation notices, renewals, bills, and more) to the party responsible for monitoring compliance. |

Mortgagee vs. Mortgagor

The mortgagee is the lender – the bank or financial institution that provides the funds to purchase the home. The mortgagor is the borrower. The mortgagor retains ownership of the property but gives the mortgagee a lien on it as security for the loan.

The mortgagee clause on the insurance policy protects the mortgagee, i.e. the lender. The mortgagor (the borrower) purchases and maintains the insurance policy, but the lender’s rights under the clause are independent of the borrower’s conduct.

Some mortgagees hire servicing companies to administer loans on their behalf, but even in those cases, the mortgagee is still considered the lender, not the servicer.

Mortgagee Clause vs. Loss Payee vs. Additional Insured

All three designations add a lender to an insurance policy, but they protect against different risks and appear on different types of policies.

| Designation | Description |

|---|---|

| Mortgagee Clause | Protects the lender's financial interest in the property. It creates an independent contract between the lender and the insurer, so the lender's claim survives even if the borrower voids their own coverage through fraud, arson, or a policy violation. This designation is appropriate for mortgage loans. |

| Loss Payee | Also directs property insurance proceeds to the lender, but without independent protection. If the borrower's claim is denied, the loss payee's claim can be denied as well. Loss payee is often used for auto loans and equipment financing. |

| Additional Insured | Is a liability designation. It extends the borrower's liability coverage to the lender for third-party claims, for example, if someone is injured on the property and files a lawsuit. It applies to liability policies such as Commercial General Liability (CGL) and does not give the lender any rights to insurance proceeds following a casualty loss. |

How It Works: Mechanics of the Mortgagee Clause

Homeowner’s Insurance

- The broker passes the lender’s exact mortgagee clause wording to the borrower’s insurance agent.

- The insurance agent adds the mortgagee clause to the policy. This activates the lender’s collateral protection.

- If a covered loss occurs, the borrower files a claim with the insurance carrier.

- The insurer assesses the damage and processes the payout according to the loss amount. All insurance correspondence is directed to the servicer named in the mortgagee clause.

When the servicer changes, the outgoing servicer notifies the new servicer and the insurance carrier that the mortgagee clause must be updated. It is in the new servicer’s interest to ensure the policy reflects the correct clause. But monitoring this process after closing is not the broker’s responsibility.

Title

- The broker provides the lender’s exact mortgagee clause wording to the title company. For Florida transactions, AD Mortgage offers AD Title – an in-house title solution available for both owner-occupied and investment properties. AD Title handles the mortgagee clause as part of the closing process with seamless communication.

– For new orders, email orders@adtitle.com

– To review current orders, email closings@adtitle.com - The title company adds the mortgagee clause to the title package, which is then sent to the broker and submitted to underwriting.

- The underwriter reviews the title package to confirm that all required risks are identified and covered, and then approves it alongside the other documents in the file.

- By the time of closing, the final title policy is already in place. At that point, the lender has full confidence in the collateral from a title standpoint, which is why the title package, including the mortgagee clause, is not modified at closing.

The Most Common Mortgagee Clause Mistakes Brokers Make

These errors have been identified by AD Mortgage’s Underwriting Team – the people who review mortgagee clauses on every file.

- Missing ISAOA/ATIMA.

- Using the wrong lender name or entity. Often pulled from an old template, the clause lists an outdated name or drops the entity suffix entirely.

- Doubling up ISAOA/ATIMA and the spelled-out version. Some brokers include both: “ISAOA/ATIMA, its successors and/or assigns, as their interests may appear.” Only one form should appear – either the abbreviation or the full phrase.

- Incorrect or missing address. This includes the wrong street name, wrong ZIP code, a completely different address, or no address at all.

“For the title commitment, omitting the address is acceptable. But in the Closing Protection Letter, the address must be present and must be correct.” – AD Mortgage Underwriting Team.

- Incorrect channel resulting in an inaccurate lender name. The lender named in the mortgagee clause depends on the origination channel. For wholesale loans, AD Mortgage must be named. For correspondent loans, the correspondent lender’s name goes on all insurance and title documents.

- Typos from manual retyping. These include misspelled “ISAOA,” incorrect PO Box, incorrect city or ZIP. To avoid mistakes, we recommend copy-pasting the clause directly from the official source.

How to Correctly Insert the Mortgagee Clause into the File

As a broker, you don’t add the mortgagee clause to the title commitment, hazard insurance policy, or any other insurance document yourself. Those documents are prepared by the title company and the insurance carrier. Your responsibility is to make sure their representatives have the exact, correct mortgagee clause wording before they finalize the paperwork.

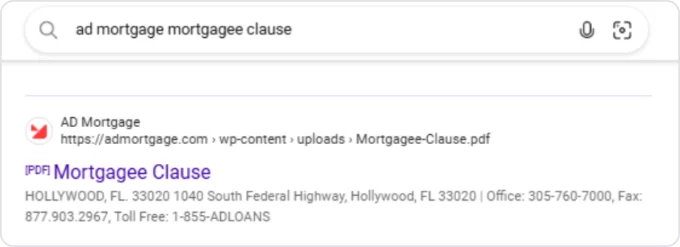

How to Find Mortgagee Clause on Lender’s Site

If you work with AD Mortgage regularly, it’s worth keeping the mortgagee clause somewhere easy to find. Bookmark this page, or search “AD Mortgage mortgagee clause” – the first result will take you directly to the official PDF, which you can also save for future use:

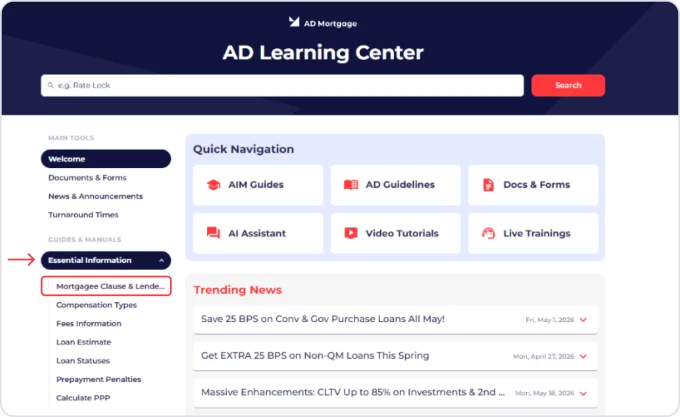

You can also find the Mortgagee Clause directly in the AIM Portal:

- Click the Learning Center tab at the top of the page

- Select Essential Information on the left

- From the dropdown, choose Mortgagee Clause & Lender IDs

This will open a dedicated page with the mortgagee clause and lender IDs, both of which your title and insurance companies may need when preparing loan documents.

Additional Recommendations from the Underwriters

Our underwriting team works with mortgagee clause errors every day. Here is their practical advice for brokers who want to get it right.

Send copy-paste text to insurance agents, not verbal instructions. When requesting a correction from the HOI agent, send the exact clause in plain text so they can paste it directly into their system. This eliminates transcription errors on their end and speeds up turnaround.

Keep a standardized email template for agent revision requests. A short, ready-to-send email with the correct clause pre-filled saves time on every correction and ensures consistency across your files.

FAQ: Mortgagee Clause

Why is a mortgagee protection clause required?

The house is the collateral for the loan. If the property is destroyed and no mortgagee clause exists, the lender has no guaranteed path to recover its financial interest from the insurance payout. The mortgagee clause creates an independent contract between the insurer and the lender, ensuring the lender is paid regardless of the borrower’s actions. Without it, lenders would not be able to issue mortgage loans at scale.

Does the mortgagee clause change depending on the loan type?

No, it doesn’t. Whether you’re closing a conventional, DSCR, or a jumbo loan with AD Mortgage, the clause wording doesn’t change based on the product. However, it does change depending on the document type (title vs. insurance documentation) and on the channel (with correspondent channel loans, the correspondent lender is named, not AD Mortgage).

Does MERS replace the lender name, or go alongside it?

MERS neither replaces nor goes alongside the lender name in the mortgagee clause. For instance, per Fannie Mae’s Selling Guide, if the mortgage is registered with MERS and MERS is named as the original mortgagee of record, MERS must not be named as mortgagee or loss payee on any property insurance policy.

Do punctuation, capitalization, or line breaks matter?

Such requirements are not specified anywhere. What matters is that all required elements are present and accurate. Minor formatting differences like commas or line breaks are generally not grounds for rejection.

Does “Its Successors and/or Assigns” need to be included?

Yes, it’s a requirement. “ISAOA” must follow the lender’s name. It’s acceptable to spell it out in full – “Its Successors And/Or Assigns” – or to use the abbreviation. “ATIMA” (As Their Interests May Appear) is usually included alongside “ISAOA”. The most common format is ISAOA/ATIMA with a forward slash, though a space (ISAOA ATIMA) or comma (ISAOA, ATIMA) are also used in practice.

Can abbreviations (LLC, N.A., FSB) be used or must they be spelled out?

Abbreviations are standard and should be used, as they are part of the lender’s official legal name as filed. The abbreviation must match the legal entity name exactly. For AD Mortgage, the correct form is A&D Mortgage LLC. “LLC” is part of the legal name and must appear.

Can a loan close if the clause has a minor typo?

It depends on what “minor” means. Punctuation differences generally don’t prevent closing, but an incorrect entity name, wrong entity suffix, or wrong address are not treated as minor – these are substantive errors that must be corrected before funding.

Are there state-specific formatting rules brokers should know?

For the clause format itself – no. The three-line structure (entity name + ISAOA/ATIMA + address) is driven by investor guidelines, not state law, and applies uniformly across all states.

What if the clause lists the wrong entity name?

It must be corrected before the loan can be funded or purchased by the investor. Lenders have complex legal names, which is why we recommend always requesting the exact wording directly from the lender rather than relying on a remembered or templated version. For AD Mortgage, the correct entity name is A&D Mortgage LLC.

Who updates the clause when the loan is sold to an investor?

It depends on who services the loan after the sale. If the lender sells the loan and doesn’t retain servicing, its servicing department sends a notification to the new servicer indicating that the mortgagee clause needs to be updated in their favor. From that point, the responsibility passes to the new servicer, and the former servicer no longer controls or monitors whether the update is completed.

How are mortgagee clauses handled if the original lender merges or closes?

When a merger occurs, insurance administrators must identify “successor by merger” situations and update the mortgagee clause to reflect the new entity’s correct legal name and address. The ISAOA language in the clause provides transitional protection (it automatically extends coverage to successors and assigns), but the policy should still be formally updated to reflect the new entity name. This is handled at the servicing level, not by the broker.

What to Do If You Have Questions About the Mortgagee Clause

Contact your AE. Your Account Executive is your first point of contact for any loan-specific questions, including mortgagee clause requirements.

Reach out to Partner Support. For general process and technology questions, the Partner Support team is available weekdays 8 a.m. – 9 p.m. EST. You can:

- Email partnersupport@admortgage.com

- Call (855) 510-5100 Ext. 3

- Or even use the Live Call option to share your screen with a specialist via Zoom for step-by-step guidance.

Use the AD Learning Center. Once logged into the AIM Partner Portal, you can access the Learning Center for tutorials, guides, and step-by-step instructions.

Ask the AD Mortgage AI Assistant. Which is available 24/7. Click the red chat button in the lower-right corner of admortgage.com. For guideline and policy questions specifically, ADwise is a dedicated AI tool.

Conclusion

The mortgagee clause is a small but load-bearing detail that appears on every loan and in multiple documents. Getting it right the first time leads to fewer conditions and a smoother experience for everyone involved. When in doubt, copy-paste it from the official source, or reach out to your AE or Partner Support if anything is unclear.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.