Is a first-time home buyer conventional loan possible? Yes, but is it the preferred option? Not necessarily. In this article, we share a short guide for brokers on how to present conventional loans for their clients who take their first steps in achieving homeownership.

Key Takeaways

- Conventional loans can be a useful option for first-time homebuyers, as they may qualify for conventional loan programs with down payments as low as 3%.

- AD Mortgage offers a wide choice of conventional loan programs, including options for first-time borrowers – including Freddie Mac HomeOne and Freddie Mac Home Possible.

- Conventional and FHA loans can both benefit first-time buyers, depending on their credit and financial profile.

ADD US AS A PREFERRED SOURCE ON GOOGLE

Can First-time Homebuyers Get a Conventional Loan?

Yes. Conventional loans are available to first-time homebuyers, not only repeat borrowers. Some first-time buyers may qualify with a down payment as low as 3%, if they meet lender requirements for credit, income, and other factors.

How Much Down Payment Does a First-time Buyer Need for a Conventional Loan?

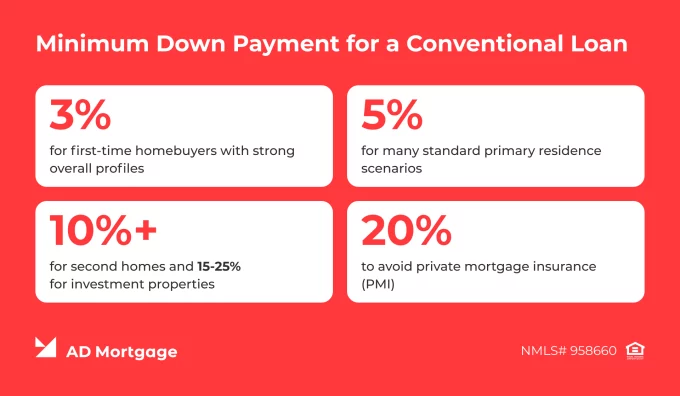

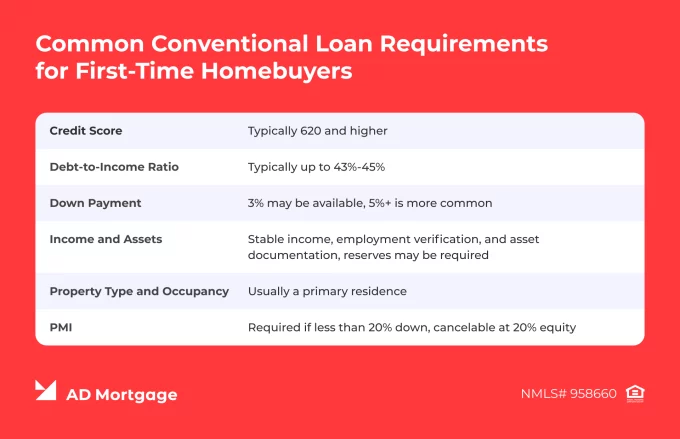

While first-time borrowers can put down as little as 3%, this typically requires a strong overall file. Often, lenders may require a higher down payment of around 5%, which is a common baseline for conventional primary residence loans for both first-time and repeat buyers. In some cases – such as low credit scores, recent credit events, or riskier properties – a down payment of up to 10% or even 20% might be required.

A key thing to mention when talking about conventional loan down payments is private mortgage insurance (PMI). This insurance protects the lender from losing money if the borrower defaults and must be paid until the borrower reaches 20% equity. PMI can then be canceled upon request, or it is automatically canceled at 22% equity.

What Does a First-time Buyer Need to Qualify?

Lender requirements for first-time homebuyers are generally similar to those for repeat buyers. However, certain programs, such as Freddie Mac HomeOne, are designed specifically for those who are purchasing the property for the first time and offer lower down payments. Additionally, first-time buyers can benefit from down payment assistance programs available in their area.

Conventional vs FHA for First-time Buyers

When purchasing their first property, borrowers often compare two mortgage options – Conventional vs. FHA loans. While these solutions have similar features, such as lower down payments, their differences are what must be considered closely.

A common misconception is that FHA loans are the best option for first-time homebuyers. In reality, both conventional and FHA loans can be favorable for first-time purchases, but they typically suit different borrower profiles.

| Conventional Loans | FHA Loans | |

|---|---|---|

| Minimum Credit Score | Typically 620+ | Typically 580+ (500-579 with 10% down) |

| Down Payment | 3% available, 5%+ common | 3.5% available for 580+, 10% for 500-579 |

| Debt-to-Income Ratio | Typically 43%-45% | Up to 50% with compensating factors |

| Mortgage Insurance | PMI required if <20% down, cancelable at 20% equity | MIP, often for the life of the loan |

| Long-Term Costs | Can be lower if PMI is canceled and interest rate is favorable | Can be higher due to ongoing MIP and possibly higher overall costs |

| Refinance Options | Standard refinance (rate-and-term, cash-out) | Standard and streamline refinance with reduced documentation requirements |

| Best Fit Scenario | Borrowers with stronger credit profiles who want lower long-term costs | Borrowers with lower credit scores or weaker financial profiles who want more flexible qualification requirements |

Special First-time Buyer Conventional Options

AD Mortgage is an experienced wholesale lender that offers a wide range of loan solutions, helping partners match their clients with the right scenarios. Our Conventional loan offerings include programs tailored to first-time homebuyers:

- Freddie Mac HomeOne is specifically designed for first-time borrowers and features loan amounts up to $832,750, minimum down payment of 3%, and FICO as per AUS.

- Freddie Mac Home Possible is designed to help low- and moderate-income buyers achieve homeownership, with loan amounts up to $832,750, and a minimum down payment of 3%.

- Fannie Mae HomeReady helps creditworthy, low- and moderate-income borrowers seeking to purchase or refinance a home, with loan amounts up to $832,750, minimum down payment of 3%, and FICO as per AUS.

Common Misconceptions to Address

- ‘First-time buyers have to use FHA.’ → No. First-time borrowers can use a variety of mortgage solutions, including conventional loans, as long as they qualify.

- ‘Conventional always means 20% down.’ → First-time homebuyers may be eligible with a down payment as low as 3%, provided their overall profile is strong.

- ‘Conventional is only for repeat buyers.’ → Conventional loans are available to both first-time and repeat buyers. However, some 3% down conventional options are specifically available to eligible first-time homebuyers.

When Conventional is a Strong Fit for a First-time Buyer

The following borrowers may benefit most from conventional loan solutions:

- Borrowers with strong credit profiles

- First-time homebuyers who can qualify conventionally with as little as 3% down

- Borrowers comparing the long-term cost of conventional financing versus FHA

- Borrowers using down payment assistance programs compatible with conventional loans

If you have any client like this, submit a scenario request and our experts will help you match the right mortgage solution.

Conclusion

First-time homebuyers can benefit from conventional loans thanks to low down payment options and removable PMI. To navigate the mortgage process smoothly, borrowers often rely on trusted broker support and guidance.

AD Mortgage helps partners focus on their clients and deliver high-level service by automating operational tasks. Our AIM Partner Portal elevates the workflow, moving through milestones quickly and efficiently. Complete a Broker Package today.

FAQ: First-Time Buyer Conventional Loan Requirements

Can a First-Time Homebuyer Get a Conventional Loan?

Yes. Conventional loans are available to first-time homebuyers and may require as little as a 3% down payment for eligible borrowers.

What is the Minimum Down Payment for a First-Time Buyer Conventional Loan?

For first-time homebuyers, the minimum down payment for a conventional loan is 3%. However, 5% is a more common minimum for both first-time and repeat buyers.

Do First-Time Buyers Need 20% Down for a Conventional Loan?

Generally, no. First-time homebuyers may qualify for a conventional loan with as little as 3% down, depending on the borrower’s financial profile and lender requirements. Higher down payment of 20% allows to avoid PMI and is often required for second homes or investment properties.

Is FHA or Conventional Better for a First-Time Buyer?

The better option depends on the borrower’s financial profile. Conventional loans typically fit better borrowers with stronger credit scores and stable finances, while FHA loans may be a better option for those with lower credit scores.

Can First-Time Buyers Get a 3% Down Conventional Loan?

Yes. Eligible borrowers with strong financial profiles may qualify for a conventional loan with 3% down.

Do First-Time Buyers Need Homeownership Education for a Conventional Loan?

Sometimes, yes. Homeownership education courses may be required for certain Fannie Mae solutions, loans with down payments of less than 5%, and assistance programs. Additionally, lenders may require homebuyer education in certain cases.

Can Down Payment Assistance be Used with a Conventional Loan?

Yes. Many regional and local down payment assistance programs can be used with conventional loans, depending on borrower eligibility.

Is PMI Required on a First-Time Buyer Conventional Loan?

Yes, PMI is required if putting less than 20% down.

Struggling with a loan scenario?

Get a solution in 30 minutes!Fill out the short form and get a call from our AE

Submit a Scenario