Post content:

California ranks as one of the largest mortgage markets in the United States. That scale translates into a steady demand for mortgage loan originators (MLOs) who can serve it. To enter that market, you need to get licensed. And though the process is slightly more complicated than in most states, it is still manageable once you know the route.

California uses two separate mortgage regulators and three possible licensing paths. This guide turns that into a concrete plan – which regulator fits your situation, every step, fee, and deadline – with links to the official sources so you can verify each detail yourself.

Good news – each path starts with the same federal baseline. Download our Guide with Fegeral Requirements for the full breakdown.

Why Becoming a California MLO is a Good Decision

Before working through the licensing maze, it is worth confirming that the payoff justifies the effort. In California, it does.

Ask mortgage professionals who have built their careers here, and the appeal comes down to scale and opportunity.

“It is a huge market. Most borrowers are well qualified, and when it’s time to refinance, there is a lot of opportunity. The loan amount is big, which allows the MLO to make more money,” – says Thuan Nguyen, CEO of Loan Factory.

Bigger loan amounts result in bigger commissions per file, but for many MLOs, the reward runs deeper than the paycheck:

“Since I started my journey as an MLO in 1993, I’ve had so many fond memories and successful stories of clients I’ve helped through the years. If there’s one thing I’ve learned, it’s that you must have a passion for showing people how real estate financing can change their lives,” – shares Peaches Jensen, Real Estate Finance Advisor and Founder of PeachTree Financial.

California is the Largest Mortgage Market in the Country

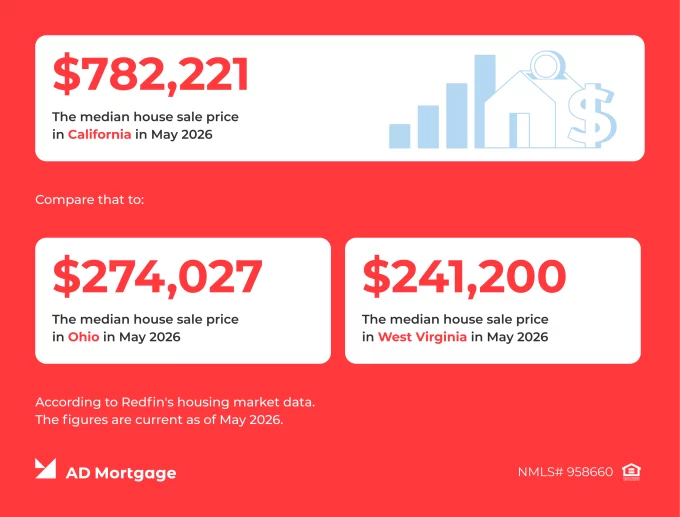

Let’s return to the numbers. In 2026, no state generates more mortgage business than California. The combination of the nation’s highest aggregate loan volume and its highest home prices leads to higher transactions. Redfin’s California housing market data put the statewide median sale price at $782,221 in May 2026, up 2.3% year over year, with 23,661 homes sold that month.

To put that in perspective, the same source shows a median of $274,027 in Ohio and $241,200 in West Virginia – meaning a California home sells for roughly three times what a West Virginia home does, and that price difference flows straight into originator income on every file.

For a new mortgage loan originator (MLO), entering the largest market in the country usually means a continuous stream of borrowers and stable income.

Salary of Mortgage Loan Officer in California

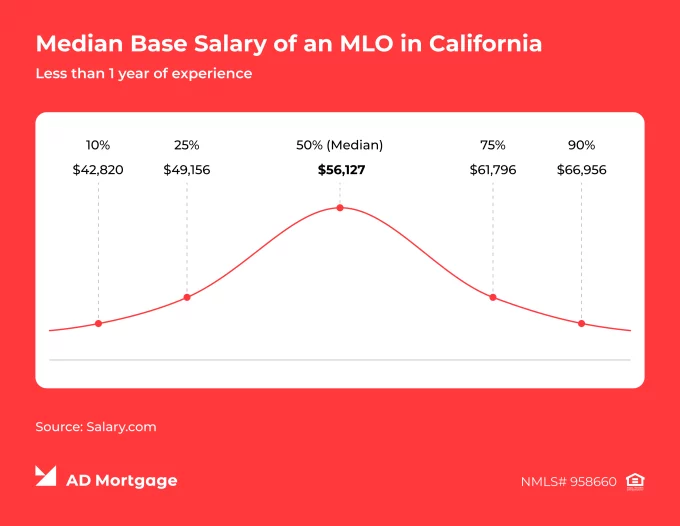

For employed MLOs, Salary.com data for Mortgage Loan Officer I in California (the entry-level tier) shows an average base salary of $56,129 as of May 1, 2026. Base pay, however, represents only part of total earnings, since commission accounts for the majority of most originators’ income.

According to Glassdoor’s California data based on 1,508 submitted salaries as of June 2026, the median total compensation for a California mortgage loan officer with <1 year of experience ranges from $83,000 to $141,000 per year. For more experienced MLOs, with 4-6 years in the profession, the total pay ranges from $107,000 to $196,000 per year.

California MLOs: Understanding the Terminology

California confuses more newcomers than almost any other state on this point. Before you apply, it helps to know how “mortgage loan officer,” “mortgage loan originator,” and “mortgage broker” differ.

On top of that, California assigns mortgage licensing to two different state agencies, and the path you choose determines which employers you can work for. Understanding these distinctions is the best way to avoid a costly wrong turn.

Mortgage Loan Originator vs Mortgage Loan Officer

These terms refer to the same role. Mortgage loan originator (MLO) is the legal term used under the SAFE Act and California licensing laws for an individual who takes residential mortgage applications or negotiates loan terms for compensation. Mortgage loan officer is simply the industry job title you’ll see more often in job postings and everyday conversation.

When you apply for a license, you’re applying to become a mortgage loan originator (MLO), regardless of what your employer eventually calls the position.

Mortgage Loan Originator vs Mortgage Broker

This distinction is more important. An MLO is an individual licensed to originate residential mortgage loans. A mortgage broker is typically the licensed business or sole proprietor that arranges mortgage loans and sponsors or employs MLOs.

If you plan to work for an existing mortgage company, you’ll generally need only the individual MLO license (or MLO endorsement, depending on the employer’s licensing structure). If you want to operate your own residential mortgage brokerage and originate loans yourself, you’ll typically need both an individual MLO license (or endorsement) and the appropriate company-level license.

The Two Regulators: DFPI vs DRE

This part is unique to California (and some other states).

Two state agencies can issue your MLO authority: a DFPI-issued MLO license, or a DRE-issued MLO license endorsement. Which one applies depends on whether you already hold a California real estate license.

If you don’t – and most new MLOs don’t – you’ll be licensed through the Department of Financial Protection and Innovation (DFPI). This is the standard path covered in the rest of this guide.

Behind the scenes, your DFPI license operates under one of two laws, the California Financing Law (CFL) or the California Residential Mortgage Lending Act (CRMLA) – but that’s determined by your employer’s company license, not by you.

If you do hold a real estate license, you can instead go through the Department of Real Estate (DRE), adding a ‘mortgage loan originator’ endorsement on top of your existing license. This route fits real estate agents and brokers moving into mortgage origination.

Interesting fact: a DRE-licensed MLO can originate loans for a CFL or CRMLA company without a separate DFPI license. But a DFPI-licensed MLO can’t originate under a DRE-licensed broker without getting DRE licensed too.

California Mortgage Loan Originator License: Quick Facts

| Regulator | Department of Financial Protection and Innovation (DFPI) for most MLOs; Department of Real Estate (DRE) licenses MLOs who hold a California real estate Broker or Salesperson license. |

| Licensing system | All applications run through the Nationwide Multistate Licensing System (NMLS). |

| Pre-license education | 20 hours of NMLS-approved coursework, including 2 hours of California-specific content for the DFPI path (DFPI MLO requirements). |

| Exam | SAFE MLO National Test with Uniform State Content – California has no separate state exam. |

| State application fee | $300 application fee under the DFPI (DFPI license fees). |

| Total estimated cost | Approximately $700 – $1,100, covering the DFPI application and investigation fees, the $110 SAFE test, the $39 FBI background check, the $15 credit report, the $30 NMLS processing fee, and a pre-licensure course ($200 – $400, varies by provider) |

| Renewal deadline | December 31 each year through NMLS, with continuing education completed first (DFPI MLO information). |

| Governing statute | California Financing Law (Financial Code §22000 et seq.) and California Residential Mortgage Lending Act (Financial Code §50000 et seq.), depending on the employer’s company license. |

How to Receive Your MLO License in California: Step by Step

Federal Requirements

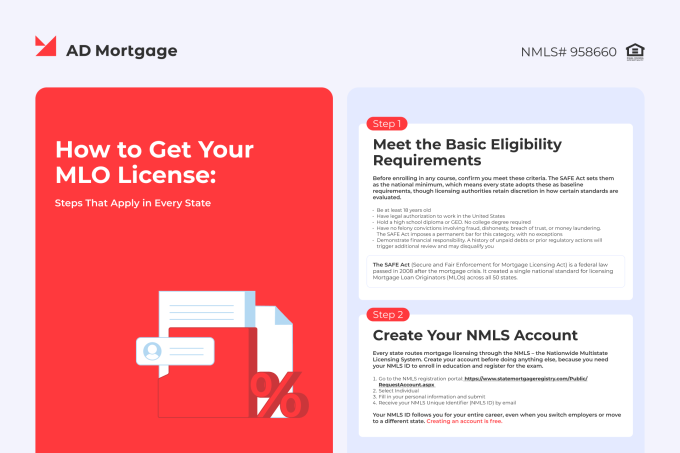

Every state shares the same federal baseline, so this section is brief:

- Create an NMLS account at the NMLS Resource Center

- Complete 20 hours of NMLS-approved pre-licensure education (PE)

- Pass the SAFE MLO Test (National Component with Uniform State Content)

- Submit fingerprints for an FBI criminal background check

- Authorize a credit report through NMLS

- Complete Form MU4 (Individual Form) in NMLS

- Submit the California DFPI MLO license application and pay the required state and NMLS fees

- Obtain sponsorship from a licensed company to activate your license

For a detailed walkthrough of each federal step, including deadlines and costs, download our complete MLO licensing guide.

California MLO License Requirements

The following requirements are specific to California and apply to the DFPI path:

1. Include 2 hours of California-specific education in your 20 PE hours

For a DFPI license, 2 of your 20 pre-licensure hours must cover California mortgage law. Most providers bundle this California-DFPI content into their pre-license packages, but confirm before you enroll. Note that pre-licensure education can expire after three years if you do not become licensed within that window, which would require retaking it.

2. No separate state exam

California uses the SAFE MLO National Test with Uniform State Content, so passing the national exam satisfies the requirement – there is no standalone California test component.

3. Pay the DFPI application and investigation fees

Per the DFPI license fee schedule, the application fee for an individual MLO license is $300, paid through NMLS. It is non-refundable, so confirm your application is complete before submitting. Additional NMLS fees apply for processing, fingerprinting, and credit reports.

4. Get sponsored by a DFPI-licensed employer

Your license stays in pending status until a company licensed under the CFL or CRMLA sponsors you through NMLS. The sponsorship request comes from the employer, and the DFPI reviews and approves it. A DFPI-licensed MLO must be employed and sponsored by a DFPI licensee to originate loans.

5. Understand the surety bond arrangement

Unlike some states that require individual MLOs to obtain their own surety bond, California generally requires the bond at the company level. Your DFPI-licensed employer is responsible for maintaining the required surety bond for its license, so individual MLOs typically do not obtain or file a separate bond.

If you have questions about your DFPI MLO application or the licensing process, you can contact the DFPI Licensing Unit at 866-275-2677.

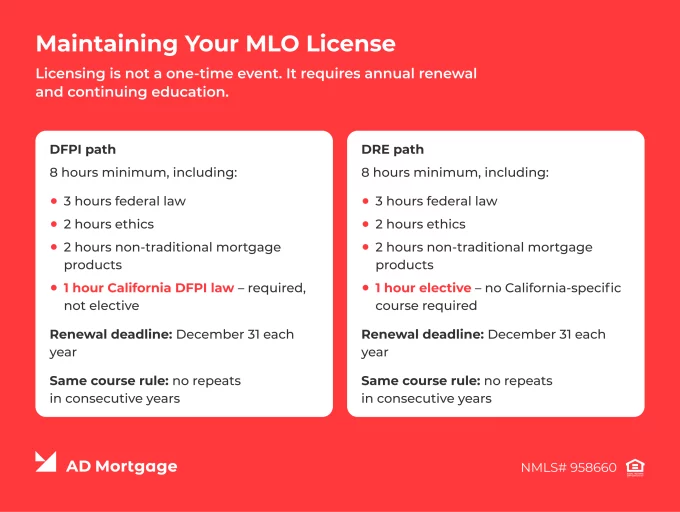

Need to Renew Your MLO License?

California MLO licenses expire every December 31. Renewal runs through NMLS. Before requesting renewal, you must complete 8 hours of NMLS-approved continuing education (CE).

California adds a wrinkle: for DFPI licensees, at least 1 of those 8 hours must be NMLS-approved California-DFPI law coursework. As with every state, the SAFE Act “successive years” rule prohibits taking the same CE course two years in a row. If you completed your pre-licensure education in the same year you were licensed, you are exempt from CE for that first year.

California MLOs can earn their CE credits at industry events that include NMLS-approved classes. Organizations that hold these events in the state include:

- California Association of Mortgage Professionals (CAMP) – the state’s mortgage trade association, which hosts conferences and live events throughout the year, including NMLS-approved CE sessions.

- Originator Connect Network – the organizer of the California Mortgage Expo series, which runs events across the state (Irvine, San Diego, Sacramento, Palm Springs, the Bay Area, and Pasadena).

- Mortgage Bankers Association – the national industry association, which holds conferences and educational events that California MLOs can attend for professional development. Some of these events also provide classes for NMLS-approved continuing education.

Attending an event like these lets you complete your CE requirement while building a professional network. For instance, in May 2026, Originator Connect Network hosted the California Mortgage Expo in Irvine. There, MLOs could attend free NMLS-approved 8-hour CE class covering the 7-hour CORE and the 1-hour California state elective.

AD Mortgage exhibited at the California Mortgage Expo in Irvine in May 2026, connecting with brokers from across the state.

How to Receive a Mortgage Broker License in California

For originators planning to open their own firm, a brokerage requires a separate company-level license in addition to your individual MLO license. Under the DFPI, you choose between two company license types:

- Decide between a California Financing Law (CFL) license and a California Residential Mortgage Lending Act (CRMLA) license. The CFL authorizes brokering and lending, while the CRMLA authorizes residential lending and servicing and carries higher requirements.

- Form your business entity and create a company (Form MU1) record in NMLS.

- Meet the net worth and surety bond requirements for your chosen license type. The CFL requires a minimum tangible net worth that scales with activity, while the CRMLA requires audited financial statements, a higher net worth threshold, a larger surety bond, and federal agency approval (such as FHA, VA, Fannie Mae, or Freddie Mac).

- Submit company applications, pay the applicable fees through NMLS, and complete background and credit reviews for all control persons.

- Employ at least one licensed California MLO to originate, and maintain ongoing reporting obligations such as the Mortgage Call Report through NMLS.

The company license involves substantially more documentation and financial qualification than the individual license, so most originators establish themselves under an existing firm before pursuing it.

FAQ: Become a Mortgage Loan Officer in California

How long does it take to become a mortgage loan officer in California?

Most applicants finish in one to three months. The 20-hour course takes about two weeks, the SAFE test can be scheduled shortly after, and the remaining time covers the background check, the DFPI application review, and employer sponsorship. California’s two-agency structure can add time if you must determine the correct path first.

What is the difference between a mortgage loan originator, a loan officer, and a mortgage broker?

In California, “mortgage loan originator” (MLO) and “mortgage loan officer” are two names for the same role: an individual who takes mortgage applications and negotiates loan terms. MLO is the legal title used on your license, while loan officer is the common job title, but not a legal definition. A mortgage broker, in turn, can refer to either an individual or a company. In the context of MLO licensing, however, it most often refers to the company that employs or sponsors MLOs and arranges loans between borrowers and lenders.

Which license do I need – DFPI or DRE?

It depends on your employer. If you plan to work for a company licensed under the California Financing Law or the California Residential Mortgage Lending Act, you need the DFPI license. If you already hold a California real estate license and plan to originate under a real estate broker, the DRE endorsement is the right path. For most new originators without a real estate background, the DFPI license is the standard route.

How much does a California MLO license cost?

Expect approximately $700 – $1,100 in total: the $300 DFPI application fee, the $110 SAFE test, the $39 FBI background check, the $15 credit report, the NMLS processing fee, and a pre-licensure course that typically costs $200 – $400 depending on the provider.

Do I need a college degree to become an MLO in California?

No. There is no degree requirement. You need the 20 hours of pre-licensure education (including 2 hours of California content), a passing score on the SAFE test, and clear background and credit checks.

Does California have its own licensing exam?

No. California uses the SAFE MLO National Test with Uniform State Content, so one national exam covers the requirement. The California-specific material is satisfied through the 2 hours of state content within your 20 education hours.

Do I need my own surety bond?

Generally, no. In California, the surety bond requirement is typically carried by the DFPI-licensed company that employs and sponsors you, rather than by the individual originator. Confirm your coverage with your sponsoring employer.

Conclusion

Becoming a licensed MLO in California is an achievable goal, even with the state’s two-agency structure. The decisive first step is determining your path: for most new originators, that means the DFPI license. From there, create your NMLS account, complete the 20 hours of education (with the 2-hour California component), pass the SAFE test, clear your background and credit checks, pay the DFPI and NMLS fees, and secure sponsorship from a licensed employer. Once you identify the correct path, the rest follows in order.

Choosing the right lender is one of the first decisions you’ll make as a licensed MLO. AD Mortgage is a wholesale mortgage lender. The company works with Broker Partners nationwide, including California. AD Mortgage offers a full range of loan programs, from Conventional and FHA to a complete Non-QM lineup.

EXPLORE WHOLESALE LENDING WITH AD MORTGAGE

Last reviewed: July 2026. Not legal advice. Licensing requirements and fees are subject to change. Always verify current requirements directly with the California Department of Financial Protection and Innovation and the California Department of Real Estate, along with the NMLS Resource Center, before beginning your application.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.

Thank you, you're successfully subscribed! Please confirm your subscription in your email.