Post content:

When comparing a jumbo vs. conventional loan, it is crucial to understand that jumbo is actually a type of conventional loan. A conventional mortgage is considered ‘jumbo’ when it exceeds the conforming loan limits. Crossing that threshold does not just change the loan name – it also triggers stricter underwriting standards because lenders assume greater risk.

Key Takeaways

- Jumbo loans are a subcategory of conventional loans. While all conventional loans are non-government-backed mortgages, jumbos are those exceeding conforming loan limits.

- Conforming loans are a more widely used option, offering predictable underwriting but tighter standards. Jumbo loans provide more flexibility while requiring a stronger financial profile.

- Due to higher lender risk, jumbo loans often come with higher pricing. However, strong borrower profiles can achieve rates very close to conforming.

- Brokers must carefully prequalify their client’s files to choose the most beneficial scenario for each case. Generally, borrowers with 760+ scores, 20%+ down, and DTI under 37% are approved for jumbo loans easier and at better terms.

Jumbo vs Conventional Loan: What is the Difference?

Why is it important for brokers to understand the difference between a jumbo and a conventional loan? Because the loan type directly impacts the borrower’s eligibility, pricing, and mortgage terms.

What Is a Jumbo Loan?

Jumbo loans are non-conforming mortgages that fall outside the limits, set annually by the Federal Housing Finance Agency (FHFA). These loans enable financing for high-cost properties, including investment and second homes.

However, jumbo loans come with some challenges. They typically feature stricter underwriting criteria, require higher credit scores, a lower debt-to-income (DTI) ratio, and larger cash reserves.

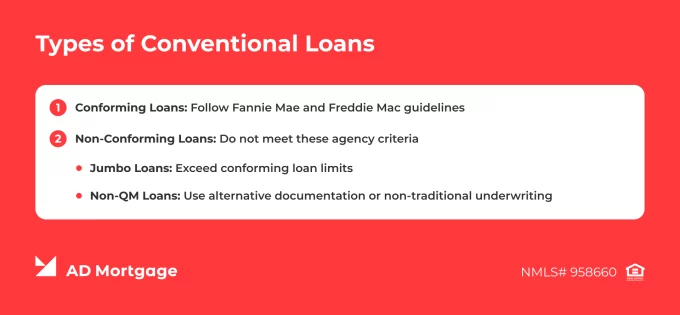

What Is a Conventional Loan?

Conventional loans are mortgages not backed by government agencies. They are offered by private lenders, including banks, mortgage companies, and credit unions. Read more about what conventional loans are in our previous article.

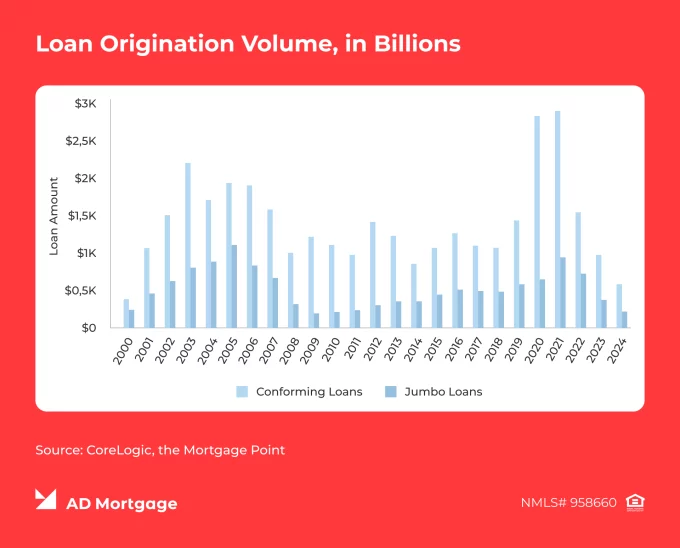

There are two types of conventional loans – conforming loans, which comply with Fannie Mae and Freddie Mac standards, and non-conforming loans, which do not. While conforming loans typically have more standardized underwriting and more favorable pricing, non-conforming loans, including jumbos, offer greater flexibility but at higher costs.

Jumbo vs Conforming Conventional: Comparison Table

While conventional loans include jumbos, comparing jumbos to conforming loans is very useful for brokers.

The table below shows the stricter underwriting standards for jumbo loans. These tougher requirements and higher pricing often come with greater flexibility in loan structure and property types.

| Jumbo Loans | Conforming Conventional Loans | |

|---|---|---|

| Definition | Non-government-backed loans exceeding conventional loan limits | Non-government-backed loans meeting agency criteria |

| Loan Amount | Above conforming limits, maximum set by the lender | Set by FHFA. In 2026, up to $832,750 for 1-unit properties in most counties |

| Credit Score | Often 700+ | Often 620+ |

| Down Payment | Typically 10%-20% | 3% for first time buyers, often 5%-20% |

| DTI | Generally 36-43% | Generally up to 45-50% |

| Reserves | Often 6-24 months | Often up to 6 months |

| Documentation | Alternative income documentation allowed, more flexible | Full but standardized |

When Does a Loan Become Jumbo?

A loan becomes jumbo when exceeding the conforming loan limits. In 2026, these are:

- One-Unit Properties: $832,750 in most counties, up to $1,249,125 in high-cost areas

- Two-Unit Properties: $1,066,250 in most counties, up to $1,599,375 in high-cost areas

- Three-Unit Properties: $1,288,800 in most counties, up to $1,933,200 in high-cost areas

- Four-Unit Properties: $1,601,750 in most counties, up to $2,402,625 in high-cost areas

Broker Tip: Check the local conforming loan limit first. This directly impacts further qualification discussion.

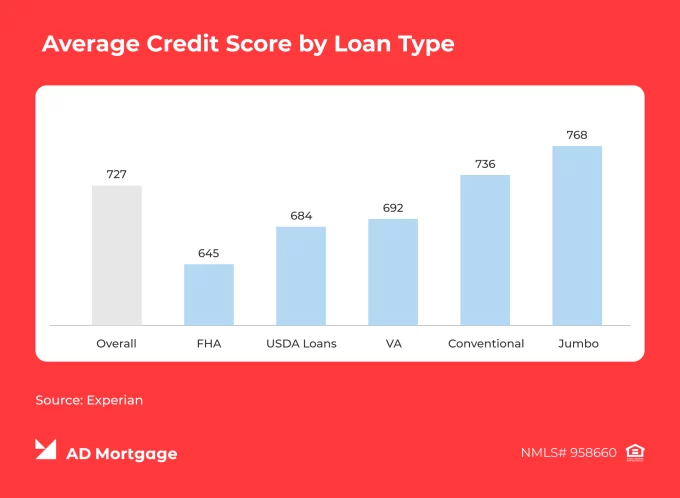

Credit Score and DTI Differences

To demonstrate a borrower’s capacity to repay a larger loan, jumbo loans feature stricter credit score thresholds, DTI, and liquidity requirements than conforming conventional loans.

Many lenders require a 700-740+ credit score for jumbos – significantly higher than 620+ for conforming loans. Jumbos also cap DTI at 36-43% – stricter than conforming loans that accept up to 50% with strong compensating factors.

Overall, stronger borrower liquidity matters a lot. Brokers should evaluate clients’ actual ability to repay during pre-qualification.

Down Payment and Reserves

Due to higher loan amounts and greater lender risk, jumbo loans demand more upfront cash from borrowers. They typically require a 10-20% minimum down payment – or sometimes more than 20% – and 6-24 months of reserves to prove financial strength post-closing.

Additionally, lenders pay extra attention to liquid, quick-access funds, such as cash, bonds, and stocks. Other assets, like retirement accounts, contribute less to overall borrower liquidity.

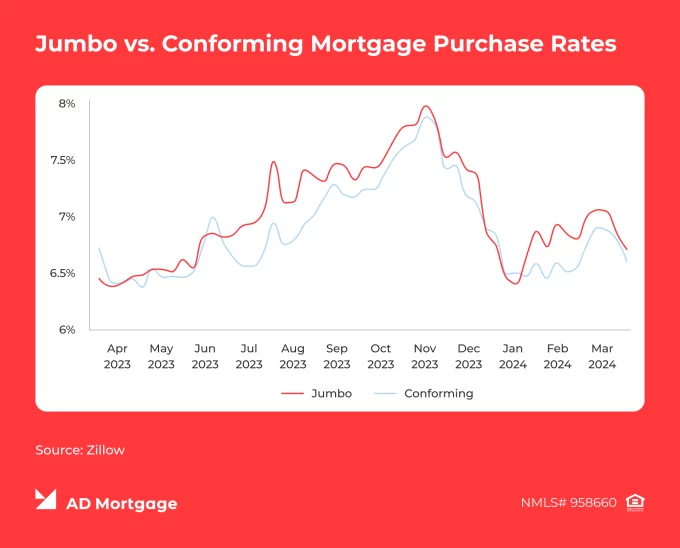

Rates: Is Jumbo Always More Expensive?

In general, jumbo loans carry 0.25%-0.50% higher rates than conforming loans. However, borrower profiles – with more than 20% down, 760+ scores, low DTI, and substantial reserves – can secure competitive pricing.

Broker Tip: Carefully prequalify borrowers – financially strong, stable clients get the most value from jumbo loans.

Which Borrowers Fit Jumbo Better?

Jumbo loans are great for high-net-worth individuals who want to purchase luxurious properties for personal use or investment purposes. However, there are several specific borrower profiles that brokers should consider when prequalifying.

These are the borrower types that can benefit most from jumbo loans:

- High-income professionals with stable employment – for example, executives or doctors with W-2 verified income of over $200,000 a year

- Great-credit borrowers with FICO over 760

- Low-DTI borrowers with DTI under 37% even after the purchase

- People buying in high-cost areas – for example, in Northern Virginia or the DC metro

- Second home or investment property buyers, as conforming loans are limited to primary residences

Which Borrowers Fit Conventional Better?

Conforming conventional loans are the more widely used mortgage solution, offering achievable requirements with standardized underwriting. These borrower scenarios fit conventional loans best:

- First-time homebuyers who qualify for a 3% down payment

- Middle-income households with stable income histories and documented assets

- Borrowers seeking lower down payment options who meet conventional qualification standards

- Primary-residence buyers purchasing modestly priced properties

Conclusion

AD Mortgage knows how difficult it might be to find the most beneficial mortgage solution for your client. For that reason, we offer a wide variety of loan programs, including conventional and jumbo options.

In case you need help matching your client with the right solution, just submit a scenario request – and our managers will connect with you within 30 minutes with a tailored solution.

FAQ: Jumbo Loan vs Conventional Mortgage

Is a Jumbo Loan a Conventional Loan?

Jumbo loans are not backed by government agencies, so they are conventional. However, they are non-conforming because they exceed FHFA limits.

What is the Difference between Jumbo and Conventional Loans?

Conventional loans are offered by private lenders and not backed by Fannie Mae or Freddie Mac. Jumbo loans are a subcategory of conventional loans that exceed conforming loan limits.

What is the 2026 Jumbo Loan Limit?

Conforming loan limits in 2026 are $832,750 in most counties and up to $1,249,125 in high-cost areas. Jumbo loan limits exceed these thresholds, and maximums are set by lenders.

Are Jumbo Loans Harder to Qualify for?

Yes, due to higher lender risk and larger loan amounts. Usually, lenders require a 700+ credit score, 6-24 months of reserves, and lower DTI.

Do Jumbo Loans Require Bigger Down Payments?

Yes, often 10%-20%, but some lenders require up to 30%.

Are Jumbo Interest Rates Higher than Conventional Rates?

Generally yes, because of larger loan amounts and higher lender risk.

Why Do Jumbo Loans Need More Reserves?

Jumbo loans typically require 6-24 months of reserves to demonstrate the ability to repay the loan and financial strength.

When Should a Borrower Choose Jumbo over Conforming Conventional?

Jumbo loans offer additional flexibility, allowing borrowers to qualify with alternative documentation, exceed conforming limits, and purchase investment properties. In some cases, jumbo loans are the best-fit option – submit a scenario to find out.

Choose among 20+ programs and get

Looking for a suitable loan program?

a detailed loan calculation

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again