Conventional loan limits are a hot topic – especially when the loan amount is shifting toward jumbo territory, or the borrower is not sure whether their county is considered a high-cost area.

The goal of this article is to create a direct broker guide, helping shape borrowers’ expectations, and address common issues efficiently.

Key Points

- Conventional loans include conforming mortgages, which fit within limits set by the FHFA, and non-conforming mortgages, which do not. These limits are updated annually and vary by county and property size.

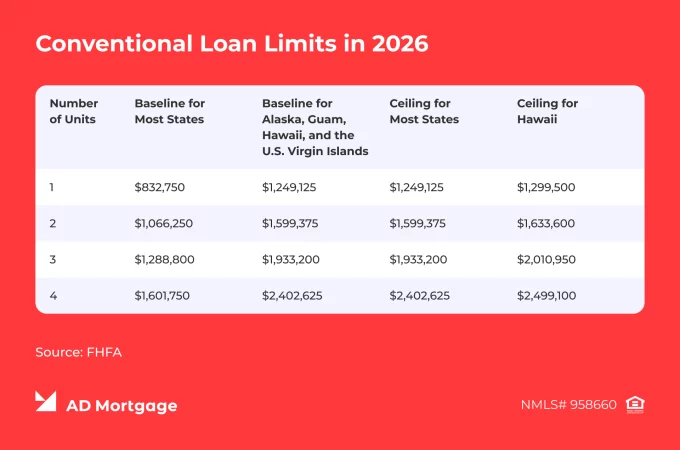

- In 2026, the baseline limits for one-unit properties in the contiguous U.S., Washington, D.C., and Puerto Rico are $832,750, and $1,249,125 for Alaska, Guam, Hawaii, and the U.S. Virgin Islands. In high-cost areas, higher maximum ceilings apply.

- The exact limit for a given county and number of units should be verified on the FHFA website.

What is the Conventional Loan Limit?

In 2026, the conventional loan baseline limit for one-unit properties in most states is $832,750. Higher-cost areas, such as New York County, feature maximum ceiling limits. Additionally, the limit varies by the number of units.

These limits are set by the Federal Housing Finance Agency (FHFA) and are updated annually.

2026 Conventional Loan Limits by Unit Count

The limits are adjusted to reflect actual property price, and therefore housing size is an important factor to consider. In 2026, the current baseline conforming loan limits for the contiguous U.S., Washington, D.C., and Puerto Rico are the following:

- 1 Unit – $832,750

- 2 Units – $1,066,250

- 3 Units – $1,288,800

- 4 Units – $1,601,750

While the difference in limits may offer additional flexibility in structuring the loan, qualifying for multi-unit properties often requires extra documentation and a more thorough underwriting review.

What Changes in High-Cost Areas?

Due to higher costs of living and elevated home prices, some counties and Metropolitan Statistical Areas (MSAs) have higher conventional mortgage loan limits. Usually, these areas include large cities or expensive suburban areas – for example, Los Angeles County and San Francisco County.

In 2026, the maximum ceiling in such areas in contiguous U.S. is $1,249,125 for one-unit properties.

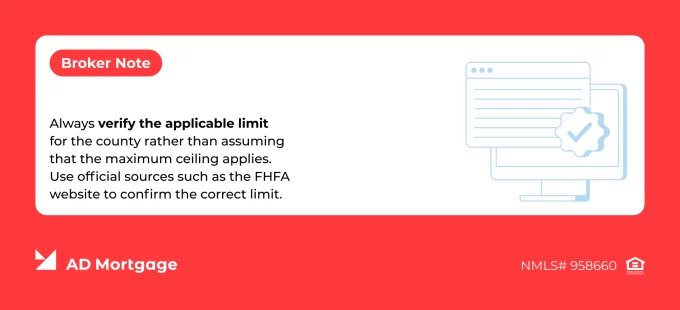

Broker Note: Always verify the applicable limit for the county rather than assuming that the maximum ceiling applies. Use official sources such as the FHFA website to confirm the correct limit.

Where to Check the Exact County Limit

As loan limits change annually and vary by county and number of units, this often leads to confusion. Brokers must carefully verify the exact county limits, using official sources, including:

- FHFA website – the authoritative source for all conventional conforming loan limits, with a county-level lookup tool and interactive map

- Fannie Mae website provides conforming loan limits overview, based on FHFA data

When Does a Conventional Loan Become Jumbo?

When a conventional loan exceeds the conforming limit, it becomes a jumbo loan, the most common type of non-conforming mortgagees.

This means that not only is the loan amount larger – jumbo loans are treated differently from conforming loans. They generally have stricter qualification requirements, more thorough underwriting, more extensive documentation, and larger down payments. Additionally, due to higher lender risk, jumbo loans may come with higher interest rates.

Comparing Conventional Loans by AD Mortgage

AD Mortgage provides a wide range of mortgage solutions, including Conventional Loan Programs. These offerings help broker partners close deals on favorable terms with fast turnaround times, innovative technology, and consistent support.

The table below shows the loan limits for AD Mortgage’s Conventional programs. Additionally, we offer refinancing options – Fannie Mae RefiNow and Freddie Mac Refi Possible – which follow the limits of the new loan being refinanced.

Loan Limits for AD Mortgage’s Conventional Programs

| Conventional Programs by AD Mortgage | Loan Limits (Valid as of May 2026) |

|---|---|

| Freddie Mac HomeOne | $832,750 |

| Conventional Standard | $832,750 |

| Fannie Mae HomeReady | $832,750 |

| Freddie Mac Home Possible | $832,750 |

| Conventional High Balance | Up to $1,249,125 per county |

Broker Talking Points

- ‘Conventional conforming limits are updated annually and vary by county and number of units. The limit applies for the whole calendar year the loan originated.’

- ‘When exceeding these limits, the loan becomes jumbo, which changes the requirements and underwriting guidelines.’

- ‘Do not assume that the national baseline applies to every county. Let’s check the exact limit for your location.’

- ‘If exceeding the baseline limits, the loan may still fall within the ceiling limits for high-cost areas. We will compare your options and structure the loan to achieve the most favorable terms.

Conclusion

There is no simple answer to ‘What is the Conventional Loan Limit in 2026?’ question. While the baseline limit for one-unit properties in most counties is $832,750, brokers shouldn’t automatically assume that it applies to their case. Verify the limit for the exact property individually using official sources.

AD Mortgage supports Approved Partners with a wide range of Conventional Programs and innovative tools that make the workflow more efficient. To match your client case with the right program, submit a Scenario Request and we will contact you within 30 minutes.

FAQ: Conventional Loan Limits 2026

What is the Conventional Loan Limit for 2026?

2026 conforming loan limits are $832,750 for one-unit, $1,066,250 for two-unit, $1,288,800 for three-unit, and $1,601,750 for four-unit properties for most counties in the contiguous U.S., Washington, D.C., and Puerto Rico. In high-cost areas, the maximum limits are higher.

What is the One-Unit Conforming Loan Limit in 2026?

The baseline limit is $832,750 for one-unit properties. In high-cost areas, the maximum ceiling is $1,249,125 for most counties, and up to $1,299,500 in Hawaii.

Are Conventional Loan Limits the Same in Every County?

No. The limits vary by county, and the state baseline should not be assumed to apply to all areas. Always verify the limits for a specific county using the FHFA website.

What are the 2-, 3-, and 4-Unit Conforming Loan Limits for 2026?

The baseline limits for most counties are $1,066,250 for two-unit, $1,288,800 for three-unit, and $1,601,750 for four-unit properties. The maximum ceiling limits in most counties are $1,599,375 for two-unit, $1,933,200 for three-unit, and $2,402,625 for four-unit properties. In high-cost areas, even higher limits may apply.

What is a High-Cost Area Conforming Loan Limit?

In 2026, the maximum ceiling limits for high-cost areas in most states are $1,249,125 for one-unit, $1,599,375 for two-unit, $1,933,200 for three-unit, and $2,402,625 for four-unit properties. In Hawaii, the maximum ceilings range from $1,299,500 to $2,499,100, depending on the number of units.

When Does a Conventional Loan Become Jumbo?

A conventional conforming loan becomes a jumbo loan when it exceeds the conforming loan limits. This changes the loan structure, eligibility requirements, and underwriting process, and often results in higher interest rates.

Is a High-Balance Loan Still Conforming?

Yes, if fitting into conforming loan limits and complying with the Fannie Mae or Freddie Mac requirements.

Where Can Brokers Check the Exact County Loan Limit?

Mortgage brokers can check the conforming loan limits for 2026 on the FHFA website, using the county-level lookup tool and interactive map.

Choose among 20+ programs and getLooking for a suitable loan program?

a detailed loan calculation