Post content:

While the flexibility of Non-QM loan guidelines is typically seen as their main advantage, this can also create uncertainty for brokers who are unsure about how to structure the loan properly. This article reviews AD Mortgage’s Non-QM offerings and explains how they help brokers win.

What are Non-QM Loans?

Non-QM loans are alternatives to traditional mortgages that allow a wider range of borrowers to qualify. People who do not fit into conventional loan requirements – for example, due to non-standard credit profiles or non-traditional employment – can achieve homeownership by demonstrating the ability to repay the loan.

For brokers, having Non-QM loans in their portfolios provides a strong competitive advantage. It helps them offer more flexibility and serve clients who fall outside standardized lending criteria. However, choosing the wrong Non-QM solution can lead to a file being declined.

AD Mortgage Non-QM Programs Overview

AD Mortgage, a leading mortgage lender, provides a variety of mortgage solutions, supporting brokers and helping their business grow. By offering flexible requirements and favorable terms, we give brokers additional leeway to match the client’s case with the right loan option.

Visit the Non-QM loans to explore all our Non-QM programs.

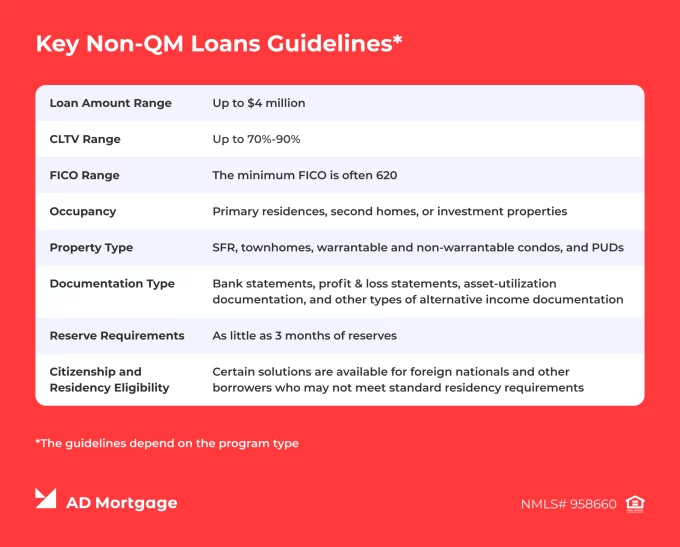

Key Non-QM Loans Guidelines to Compare Before Submission

Non-QM approvals depend not only on the borrower’s profile but also on how the loan is structured. Therefore, brokers should consider numerous features when choosing the best-fit loan scenario for their clients, including:

- Loan Amount Range. AD Mortgage offers loan amounts up to $4 million, depending on the program type.

- CLTV Range. The average CLTV accepted is up to 70%-90%, depending on the program type.

- FICO Range. The minimum FICO is often 620, depending on the program type.

- Occupancy. Primary residences, second homes, and investment properties can all be available, depending on the program type.

- Property Type. Various programs cover a wide range of properties, including single-family residences, townhomes, warrantable and non-warrantable condos, and PUDs.

- Documentation Type. Alternative income documentation is typically accepted, including bank statements, profit & loss statements, and asset-utilization documentation.

- Reserve Requirements. Most programs require as little as three months of reserves.

- Citizenship / Residency Eligibility. Certain solutions are available for foreign nationals and other borrowers who may not meet standard residency requirements.

Top AD Mortgage Non-QM Programs and Their Requirements

When brokers understand the borrower profile, they can choose the exact loan product that fully covers their client’s needs and fits their situation. Below are the core AD Mortgage Non-QM programs, designed for a variety of borrower cases.

DSCR Loan Guidelines

DSCR is a program for investors that allows them to qualify based on the cash flow generated by the investment property.

Best-Fit Borrower Type: New and experienced real estate investors.

Key DSCR program highlights:

- Minimum FICO: 620

- CLTV: Up to 80%

- Eligible Properties: 1-4 Units, Condotels, Mixed-use, and Multifamily (5-8 units) allowed

- Income Verification: No income or employment verification required

- Eligible Borrowers: U.S. Citizens, Non-Permanent Residents, ITIN, and Foreign Nationals allowed

- Reserves: Minimum three months of reserves required

- Loan Amounts: Up to $3 million

Unlike conventional loans, DSCR loans do not have limits on the number of properties financed and rely on rental income for qualification. Therefore, borrowers who might not be eligible because of their personal income can still purchase investment properties if they meet the requirements.

12/24 Month Bank Statement Loan Guidelines

This program allows borrowers to qualify based on the deposit income reflected in personal and/or business bank statements, rather than relying on tax returns. This approach demonstrates real cash flow and gives additional flexibility in documenting income.

Best-Fit Borrower Type: Self-employed individuals, business owners.

Key 12/24 Month Bank Statement program highlights:

- Minimum FICO: 620

- CLTV: Up to 90% for purchase, up to 80% for cash-out

- Eligible Properties: SFR, townhomes, warrantable and non-warrantable condos, condotels, 2-4 units, PUD, short-term rentals, rural SFR, leasehold

- Income Verification: Personal, business, or combined bank statements

- Eligible Borrowers: U.S. Citizens, Permanent Residents, Non-Permanent Residents, ITIN

- Reserves: Minimum three months of reserves required

- Loan Amounts: Up to $4 million

The program does not require tax returns and includes a free Concierge Service to calculate qualifying income, making it easier for brokers and borrowers to determine eligibility.

Bank Statement:

Empower your clients!

See Program Details

1Y/2Y Full Doc Loan Guidelines

The solution allows borrowers to qualify using traditional income and offers more flexible Non-QM mortgage guidelines compared with conventional loans.

Best-Fit Borrower Type: Small business owners, investors, or other self-employed individuals.

Key 1Y or 2Y Full Doc program highlights:

- Minimum FICO: No score or a minimum of 620

- CLTV: Up to 90%

- Eligible Properties: SFR, townhomes, warrantable and non-warrantable condos, condotels, 2-4 units, PUD, short-term rentals, rural SFR, leasehold

- Income Verification: All income types for Super Prime, no income or employment verification for DSCR

- Eligible Borrowers: U.S. Citizens, Permanent Residents, Non-Permanent Residents, ITIN

- Reserves: Minimum three months of reserves required

- Loan Amounts: Up to $4 million

The 1Y or 2Y Full Doc program is an option for those borrowers who do not fit into rigid conventional guidelines, despite having full traditional income documentation.

ITIN Mortgage Guidelines

For non-U.S. citizens, the ITIN program is a great solution that helps them make homeownership a reality. As both primary residence and investment properties are allowed, the program fits the needs of a wide range of borrowers.

Best-Fit Borrower Type: Individuals who have an Individual Taxpayer Identification Number but do not have a Social Security Number.

- Minimum FICO: 660

- CLTV: Up to 70%

- Eligible Properties: SFR, townhomes, warrantable and non-warrantable condos, condotel, 2-4 units (not available for second homes), PUD, rural SFR, short-term rentals, leasehold

- Income Verification: All income types for Super Prime, no income or employment verification for DSCR

- Eligible Borrowers: ITIN

- Reserves: Minimum three months of reserves required

- Loan Amounts: Up to $1.5 million

This program helps mortgage originators serve an underserved segment of the market by providing mortgage access to non-U.S. citizens who are actively contributing to the U.S. economy.

Free and Useful AD Mortgage Resources for Brokers

To close deals successfully, brokers need a straightforward workflow. AD Mortgage helps our partners streamline their routine by providing clear guidelines and by developing new technological solutions.

The efficiency of such tools is demonstrated in our Mortgage Professionals Pulse Report showing that 35.3% of respondents highlight technology adoption as the key to their success in 2025.

What are the key technologies and resources to follow for Non-QM information?

- ADwise → The free AI guideline assistant that helps you reduce time spent on manual research and focus on more important things instead. Use this one-window assistant to get answers about property and loan requirements, lock policies, regulations, borrower eligibility, and other issues.

- Page with Non-QM Guidelines → For those who prefer to review requirements manually, this page contains all necessary documentation.

- Program Submission Checklists → Brokers’ checklists help keep the process going without requiring them to remember every detail.

- AD Studio → The set of customizable marketing flyers with product overviews to use in your communication with customers.

- LEADer CRM → The free CRM system that helps you stay organized with your contacts and leads, and allows you to apply Non-QM programs for clients who are struggling to qualify for conventional loans.

- ADvantage Loyalty Program → The Loyalty Program offers numerous uses of a partner’s points for helping reduce costs and speed up processing. If you have points already, use them. If you don’t, earn them by closing more loans.

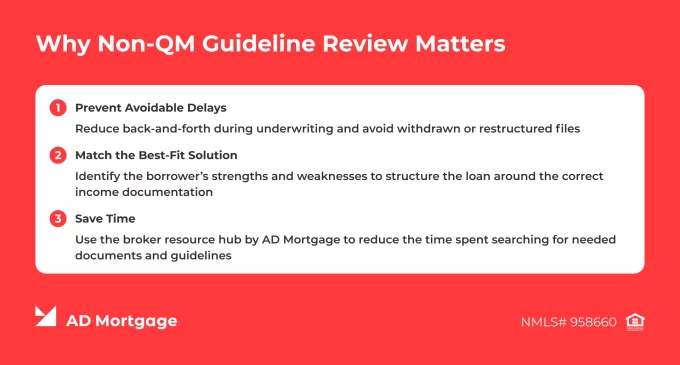

Why Non-QM Guideline Review Matters

Reviewing the Non-QM loan guidelines before submitting the file benefits the workflow in several ways:

- Prevent Avoidable Delays. Taking time to review the details can help reduce back-and-forth during underwriting and avoid withdrawn or restructured files.

- Match the Best-Fit Solution. Identifying the borrower’s strengths and weaknesses is crucial for positioning the loan appropriately and structuring it around the correct income documentation.

- Save Time. Using the broker resource hub by AD Mortgage reduces the time spent searching for needed documents and guidelines. Brokers can quickly confirm program details and move the file efficiently from submission to approval.

FAQ: Non-QM Loans Guidelines

What is a Non-QM Loan?

Non-QM loans are alternatives to conventional loans that allow borrowers with strong but non-traditional profiles to qualify. While providing greater flexibility, Non-QM loans still require demonstrating the ability to repay the mortgage.

What are the Main Non-QM Loan Requirements?

Non-QM guidelines vary by lender. AD Mortgage Non-QM programs mostly accept CLTV up to 70%-90%, require a minimum FICO of 620 and as little as three months of reserves, and offer loan amounts up to $4 million.

How do Non-QM Guidelines Differ from Conventional Loan Guidelines?

Conventional mortgages require borrowers to fit into strict criteria, and the underwriting is performed automatically, allowing only certain types of borrowers to qualify. Non-QM loans provide greater flexibility for those who do not fit the traditional lending box but have the repayment capacity – for example, self-employed individuals or business owners.

What FICO Score is Needed for a Non-QM Loan?

The credit score requirements vary by lender and mortgage product. The minimum FICO needed for Non-QM loans typically ranges between 620 and 700.

What Income Documents are Used for Non-QM Loans?

Depending on the mortgage solution, different types of alternative documentation can be used, including bank statements, asset depletion, and profit-and-loss statements.

What is the Difference Between DSCR and Bank Statement Programs?

The DSCR program is designed for investors and allows them to qualify based on the income generated by the investment property. The Bank Statement program is great for self-employed borrowers who can qualify based on the deposit income in the bank statement instead of traditional tax returns.

Where Can Brokers Review AD Mortgage Non-QM Guidelines?

To review the AD Mortgage Non-QM loan requirements, brokers can visit the dedicated page or use ADwise, the AI guideline assistant.

Conclusion

Prequalifying the borrower profile and reviewing Non-QM requirements help brokers accurately match their clients with the mortgage solutions. If you need any support in choosing the right program, submit a scenario and our experts will contact you within 30 minutes with a tailored solution.

Choose among 20+ programs and get

Looking for a suitable loan program?

a detailed loan calculation

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again