For conventional loans, the down payment is not a stand-alone requirement. It is tightly connected to numerous other variables. Therefore, it might be difficult for the borrower to determine how much they should put down. This is where brokers can help out.

Key Takeaways

- A conventional down payment can start at 3% for eligible borrowers, while 5% is a common baseline, and 20% is the threshold for avoiding PMI.

- The down payment requirement depends on lender overlays, property type, and the borrower’s profile, including credit score, DTI ratio, and reserves.

What is the Minimum Down Payment for a Conventional Loan?

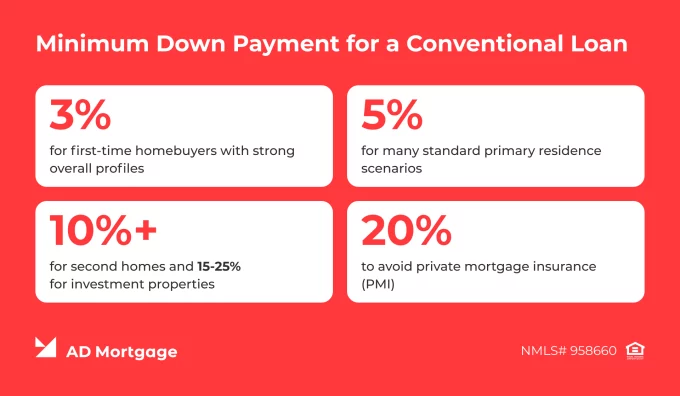

The down payment requirements vary based on lender overlays and the borrower’s goals and financial profile. The common baselines are as follows:

- 3% for first-time homebuyers with strong overall profiles

- 5% for many standard primary residence scenarios

- 10%+ for second homes and 15-25% for investment properties

- 20% to avoid private mortgage insurance (PMI)

When is a 3% Down Payment Possible?

Eligible borrowers might qualify for as low as 3% down, but this is not a universal default. Financial profile, credit strength, and program fit matter and the key is understanding requirements upfront.

Who typically qualifies for 3% down? First-time homebuyers or some low-to-moderate income borrowers.

AD Mortgage offers the Fannie Mae HomeReady and Freddie Mac Home Possible programs to help these borrowers achieve homeownership with as little as 3% down.

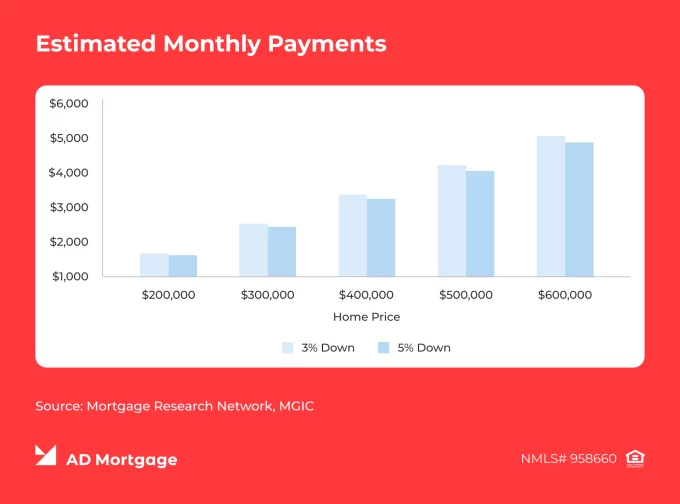

A 5% Down Payment is Often More Realistic

While 3% is possible, a 5% down payment is more common for standard primary residence loans. This is usually a more realistic situation for many borrowers.

Who typically qualifies for 5% down? Repeat buyers, borrowers above income limits, and those who fit standard conforming loan guidelines.

Of course, at 5%, PMI is still required. However, stronger profiles can qualify for better PMI pricing than at 3%.

Do You Need 20% Down Payment for a Conventional Loan?

The direct answer is no. A larger down payment may be required in certain scenarios, such as investment properties, but typically this is not a matter of qualification.

Putting 20% down helps avoid PMI and can lower monthly payments, reduce the loan amount, and potentially improve pricing.

How PMI Changes the Down Payment Conversation

Generally, annual PMI ranges from 0.3% to 1.5% of the total loan amount, although rates above 1% are uncommon. PMI continues until 20% equity is reached. It can then be canceled manually at 20% but will automatically be removed once 22% equity is reached.

Borrowers often need a broker’s help in comparing available options:

- Making a 20% down payment and avoiding PMI

- Making less than 20% down and paying PMI annually until reaching 20% equity

Therefore, the lowest upfront down payment is not always the most cost-effective choice in the long run.

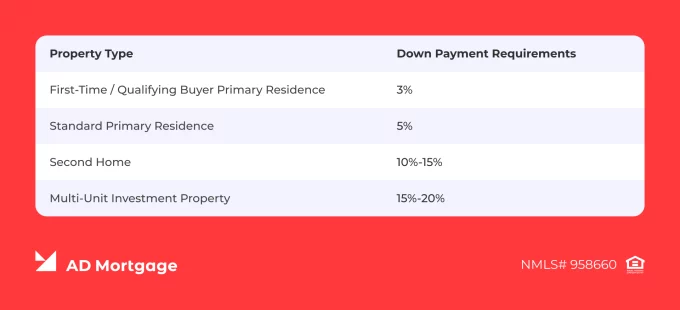

How Down Payment Requirements Change by Property Type

Understanding the type of property a borrower plans to purchase helps shape realistic expectations upfront.

What Else Affects the Required Down Payment?

The minimum down payment is established for each scenario based on lender overlays, program requirements, and key aspects of the borrower’s profile, including:

- Credit score

- Debt-to-income ratio (DTI)

- Occupancy

- Property type

- Source of funds

- Overall file strength

Conventional Loan Doan Payment vs FHA Loan Down Payment

While FHA loans might come with lower initial costs, it is crucial to consider the total loan cost when making a decision.

| Loan Type | Minimum Down Payment | Considerations |

|---|---|---|

| Conventional Loan | 3% for eligible first-time buyers, 5% for other borrowers | PMI is required until 20% equity is reached |

| FHA Loan | 3.5% with a credit score of ≥580, 10% with a score of 500-579 | Upfront and ongoing mortgage insurance premiums, often for the life of the loan |

Conclusion

Don’t know which mortgage solution will be most beneficial for your client? Submit a loan scenario, and AD Mortgage’s experts will reach out within 30 minutes with a tailored loan program.

FAQ: Conventional Loan Down Payment Requirements

What is the Minimum Down Payment for a Conventional Loan?

The conventional loan minimum down payment is 3% for first-time homebuyers and 5% for other eligible borrowers.

Can you Get a Conventional Loan with 3% Down?

Yes. A 3% down conventional loan is possible for first-time homebuyers and some low-to-moderate income borrowers.

Do Conventional Loans Require 20% Down?

Typically, no, but putting 20% down helps borrowers avoid PMI.

Is 5% Down enough for a Conventional Loan?

It might be, but eligibility depends on program requirements, property type, and the borrower’s profile.

How Much of a Down Payment is Needed to Avoid PMI?

Putting 20% down allows borrowers to avoid PMI.

Do Second Homes Require a Larger Conventional Down Payment?

Yes, often around 10%-15%.

Do Investment Properties Require a Larger Conventional Down Payment?

Yes, often around 15%-20%.

Is FHA or Conventional Better for a Low Down Payment?

FHA loans often allow lower minimum down payments, but conventional loans might offer lower overall costs in the long run.

Choose among 20+ programs and getLooking for a suitable loan program?

a detailed loan calculation