Post content:

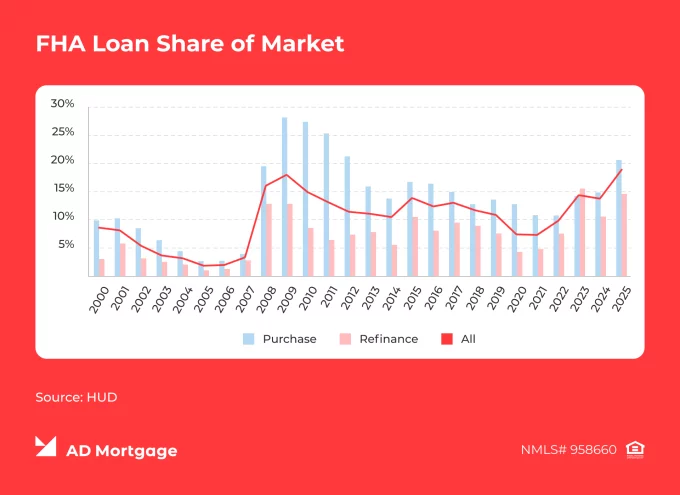

In 2025, FHA loan market share grew for the fourth year in a row. It reached $1.583 trillion of forward mortgages, which is 10% more than the year before. Additionally, FHA solutions continue to stay the most popular among first-time buyers – they accounted for 83.3% of FHA loan endorsements in financial year 2025.

Originally published: April 25, 2025 · Last updated: May 1, 2026 (updated with latest data and guidelines)

How can mortgage originators use FHA loans to help their clients purchase a house on better terms?

In general, FHA mortgages are versatile solutions that can benefit different borrower types – including those with moderate savings or lower credit scores. This article focuses on FHA loan limits for 2026, key requirements, and mortgage insurance premiums.

- What is an FHA Loan?

- How FHA Loans Work in 2026

- FHA Loan Requirements for 2026

- FHA Loan Benefits and Disadvantages

- FHA Loan Refinance

- FHA Programs by AD Mortgage

Key Takeaways

- FHA loans are widely used mortgage products offered by private lenders, like AD Mortgage, and backed by the FHA, a government agency. Thanks to this governmental support, more low- to moderate-income borrowers can achieve homeownership.

- More lenient requirements are what distinguishes FHA loans from other mortgage products. Therefore, borrowers with lower credit scores, moderate down payments, or higher debt-to-income ratios can qualify.

- FHA mortgages come with limitations that must be considered, such as loan limits, eligible property types, and mortgage insurance premiums.

What is an FHA Loan?

FHA loans are mortgages provided by FHA-approved private lenders and insured by the Federal Housing Administration (FHA) – a government agency that is part of the United States Department of Housing and Urban Development (HUD).

Thanks to government backing, lenders carry less risks and can offer more favorable pricing to the borrowers. Therefore, borrowers with lower down payment or recent credit issues might qualify for a loan.

In short, FHA loans are a preferred option for many borrowers as they are reputable and common mortgage solutions that are easier to qualify for than conventional loans.

How FHA Loans Work in 2026

In 2026, borrowers with a credit score of 580 or higher need to put down 3.5%. A higher down payment of 10% allows borrowers with lower scores from 500 to 579 to qualify.

To protect lenders in case a borrower defaults, FHA loans require mortgage insurance premiums (MIPs), paid upfront and annually. At closing, the borrower covers a fixed fee of 1.75% and then pays the ongoing fee – it depends on a variety of factors, such as loan amount and loan terms, and typically ranges between 0.15% and 0.75%.

Despite these added expenses, FHA loans remain affordable and attract a wide range of borrowers.

Federal Housing Administration: Role and Operations

The Federal Housing Administration, was founded in 1934 during the Great Depression, and since then has insured over 50 million mortgages. Now, it is among the largest mortgage insurers in the world.

The FHA’s role is to cover the unpaid principal and interest balance for lenders in case of borrower defaults. With this support, lenders can offer more mortgages to borrowers and on better terms.

FHA is mostly self-funded – the main income source of the Administration is mortgage insurance premiums. Additionally, the FHA is supported at the federal government level to maintain the sustainability of these loan programs.

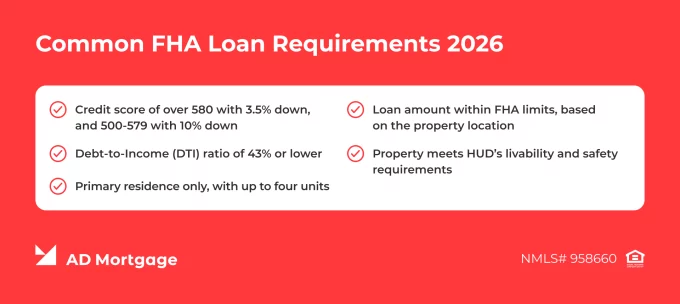

FHA Loan Requirements for 2026

While the FHA sets minimum requirements for its loan programs, FHA-approved lenders can impose their own thresholds. The most common baselines include:

- Credit score of over 580 with 3.5% down, and 500-579 with 10% down

- Debt-to-Income (DTI) ratio of 43% or lower

- Primary residence only, with up to four units

- Loan amount within FHA limits, based on the property location

- Property meets HUD’s livability and safety requirements

Based on these FHA conditions, lenders evaluate the borrower’s financial stability and creditworthiness. Understanding the requirements helps brokers to pre-qualify borrowers more quickly and accurately.

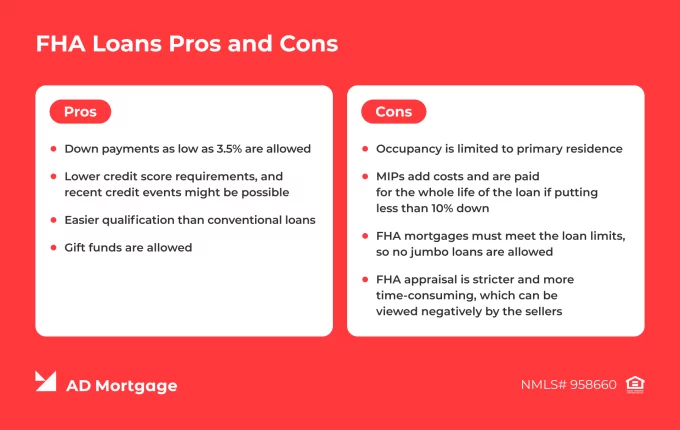

FHA Loan Benefits and Disadvantages

Mortgage originators must clearly state – like any other mortgage program, FHA loans are not a universal solution. These loans have their benefits and limitations, and do not fit all borrower profiles. The broker’s goal is to set realistic expectations about loan costs, timelines, and associated obligations.

Pros

FHA loans are a preferred option for people seeking affordable housing and might not have perfect credit history. Key advantages include:

- Down payments as low as 3.5% are allowed

- Lower credit score requirements, and recent credit events might be possible

- Easier qualification than conventional loans

- Gift funds are allowed

Cons

For stronger borrower profiles or more upscale properties, FHA loans might not be the best choice. Their disadvantages include:

- Occupancy is limited to primary residence

- MIPs add costs and are paid for the whole life of the loan if putting less than 10% down

- FHA mortgages must meet the loan limits, so no jumbo loans are allowed

- FHA appraisal is stricter and more time-consuming, which can be viewed negatively by the sellers

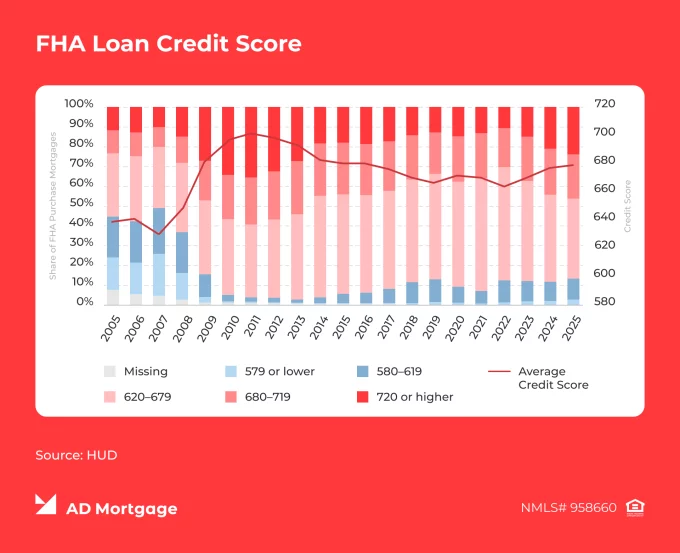

FHA Credit Score Requirements

While lenders may apply overlays, the standard credit score requirements are the following:

- Below 500: Typically, ineligible for FHA loans

- 500-579: Eligible with 10% down

- 580+: Eligible for maximum financing, with a down payment as low as 3.5% required

Down Payment Requirements

Depending on credit score, FHA loans allow down payments of 3.5% to 10%. Apart from personal savings, gift funds and approved down payment assistance (DPA) programs can be used to cover the down payment.

One thing to consider is how the down payment size impacts the MIPs. When putting 10% down or more, the MIP can be canceled after 11 years of mortgage payments. Otherwise, MIPs are required for the life of the loan. Additionally, as the MIP amount depends on the loan amount, LTV, and other factors, higher down payment results in lower annual MIP.

Loan Limits 2026

The FHA sets the ‘floor’ and ‘ceiling’ loan limits – they vary by county and number of units and are updated annually. The ‘floor’ is not a minimum amount, but instead, it is the maximum amount in low-cost areas. The ‘ceiling’ is the highest possible conforming loan limit, which applies to the most expensive areas.

In 2026, the one-unit property ‘floor’ is $541,287 in low-cost areas and ‘ceiling’ is $1,249,125 in high-cost areas.

To check the exact limits, mortgage originators and borrowers can use the FHA’s official tool.

How First-Time or Moderate-Income Borrowers Benefit from FHA Loans

It is no surprise that FHA loans remain the most popular choice among first-time homebuyers. For these borrowers, saving for a down payment is usually one of the biggest challenges. FHA mortgages provide a solution – lower down payment requirements with DPAs and gift funds are allowed.

Unlike conventional loans, FHA mortgages are available to borrowers with lower credit scores and recent minor credit events. For some families, FHA loans may be the only option to buy now, while planning to refinance later when the borrower profile improves.

FHA Loan Types: Purchase, Repairs, and Energy-Efficient Upgrades

FHA loans are not limited to purchasing a house. They also help to improve it – including small repairs, major renovations, or energy-efficiency home improvements. Thanks to those options, FHA borrowers can upgrade their house without taking a second loan or maxing out credit cards.

Note that the property must still be a primary residence and meet HUD’s basic livability, safety, and habitability requirements.

Available options of FHA loan types include:

- 203(k) Mortgage Programs allow non-structural or structural fixes with costs being financed into the loan amount

- Energy Efficient Mortgage (EEM) supports the implementation of energy-saving tools, such as solar panels, insulation, or HVAC systems.

- Disaster Victims Programs 203(h) offers funding for those willing to build or reconstruct homes in disaster areas, often with no down payment required.

FHA Loan Refinance: Streamline, Cash-Out, and Rate‑and‑Term

FHA loan options are not limited to purchasing a property. The FHA also allows borrowers to refinance a loan to achieve better terms or get a cash-out. However, it is crucial to remember that refinancing should have a clear net tangible benefit to the borrower. Usually, that means a lower rate or more predictable terms, such as when switching from adjustable to fixed rate.

FHA refinance offerings include:

- FHA Streamline Refinance: Quick refinance with little documentation and no appraisal required

- FHA Cash-Out Refinance: Replacing the existing mortgage with the new, larger one and borrowing against home equity

- FHA Rate-and-Term Refinance: Full refinance for FHA or non-FHA loans

Additionally, there is a standalone solution – FHA Reverse Mortgage (HECM). It is designed for senior borrowers who want to convert part of the home equity into cash.

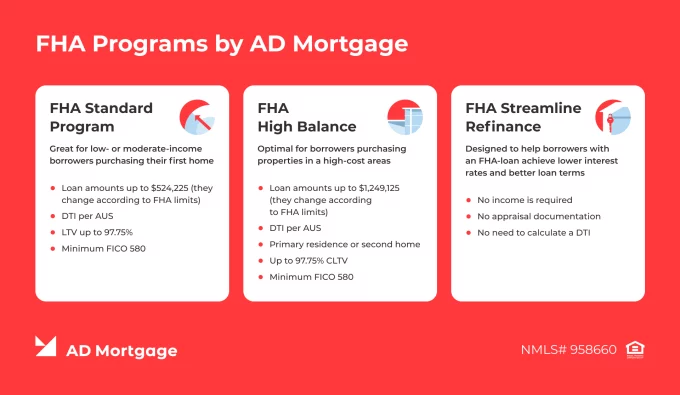

FHA Programs by AD Mortgage

AD Mortgage is an established mortgage lender that offers a variety of mortgage programs, helping brokers serve a wide range of clients. In this article, we focus on FHA offerings, but the full list of AD Mortgage programs can be found on the Programs Page.

FHA Standard Program

Great for low- or moderate-income borrowers purchasing their first home

- Loan amounts up to $524,225 (they change according to FHA limits)

- DTI per AUS

- LTV up to 97.75%

- Minimum FICO 580

FHA High Balance

Optimal for borrowers purchasing properties in a high-cost areas

- Loan amounts up to $1,249,125 (they change according to FHA limits)

- DTI per AUS

- Primary residence or second home

- Up to 97.75% CLTV

- Minimum FICO 580

FHA Streamline Refinance

Designed to help borrowers with an FHA-loan achieve lower interest rates and better loan terms

- No income is required

- No appraisal documentation

- No need to calculate a DTI

Conclusion

FHA loans are great for brokers to include into their program portfolio. These solutions are extremely common as they help a large category of borrowers – low- and moderate-income first-time homebuyers – achieve homeownership.

Choose AD Mortgage programs to receive straightforward workflow, full-time support, and convenient innovative features. Become an approved partner and let us help your business grow: Become a Partner | AD Mortgage

FAQ: FHA Loans

What is an FHA Loan and Who Qualifies?

FHA loans are backed by the Federal Housing Administration (FHA), and thanks to reduced risk, mortgage lenders are often capable of offering lower interest rates. Low– to moderate-income borrowers, including first-time homebuyers, are usually able to qualify.

What are the FHA Loan Requirements?

While lenders are able to apply their own thresholds, the FHA sets the minimum requirements. In 2026, FHA borrowers are required to have a credit score of 580 with 3.5% down and 500-579 with 10% down, lower scores are typically ineligible. Additionally, the loan must fit into the FHA loan limits.

What is the Downside to an FHA Loan?

FHA loans require a lifetime mortgage insurance premium (MIP). However, if putting more than 10% down, it can be canceled after 11 years of mortgage payments. Also, occupancy types are limited to primary residence.

What Would the Minimum Down Payment Be for an FHA Loan of $250,000?

If the borrower has a credit score of 580 or higher, they can put as little as 3.5% ($8,750). With a score between 500 and 579, 10% down is required, so the borrower needs to put down $25,000.

Why Don’t Sellers Like FHA Loans?

FHA loans require stricter appraisal, which might trigger costly repairs, and involve longer approvals. Therefore, some sellers avoid borrowers purchasing under FHA loans.

How Long Does FHA Loan Approval Take?

Usually, the approval takes between 30 and 45 days, but can be extended to 60 days in some cases.

Is It Hard to Get Approved for FHA?

FHA loans feature fairly lenient guidelines, compared to conventional loans. Therefore, it is often easier to qualify, for example, first-time buyers or those with lower credit scores

Does the Federal Housing Administration Make Loans?

No. The FHA insures the loans offered by FHA-approved lenders. Therefore, in case the borrower defaults, the lender won’t lose money and FHA will cover the costs.

What is the Goal of the Federal Housing Administration (FHA)?

The FHA role is to support affordable homeownership by reducing lender risk. Thanks to that support, lenders offer these mortgages more widely and at affordable costs.

What is the FHA 12-Month Rule?

During the 12-month period before application, an FHA borrower is required to not have any late mortgage payments. For Cash-Out Refinance, the rule implies that the borrower has occupied the property for at least 12 months.

Fill out the short form and get a call from our AE

Struggling with a loan scenario?

Get a solution in 30 minutes!

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again