For years, new homebuyers have heard the same advice: ‘Wait until you have 20% down to buy a home and avoid all those PMI costs.’ This is nothing new as I was told the same thing over 30 years ago. The problem is that while well-intentioned, this approach will often cost homebuyers more wealth than they save on PMI.

In a recent AD Mortgage Digest interview, Albert Martinez of Essent Mortgage Insurance shared insights into how PMI works, why many buyers misunderstand it, and how the right financing strategy can help families purchase a home sooner rather than waiting years to save a larger down payment.

Watch the full interview with Albert Martinex and AD Mortgage’s Serena Diaco below as they discuss PMI, down payments, and other tools.

One of the key takeaways from the interview is that PMI is not a barrier, but actually a tool for new homebuyers. Trying to avoid all PMI charges can be one of the biggest mistakes in the short and long term.

ADD US AS A PREFERRED SOURCE ON GOOGLE

The 20% Down Payment Myth

Buyers are often encouraged by a variety of sources to avoid PMI by putting 20% down when buying a house. This advice isn’t necessarily bad if reaching that 20% down can be done in short order. However, for most homebuyers, this can delay a purchase by over a year or much more.

20% down is not required to buy a home and many Conventional loan programs allow for significantly less of a down payment to qualify. PMI helps to bridge that gap, saving buyers time in achieving their home ownership dreams. It also allows them to start generating more net worth (wealth) sooner, which can pay big dividends down the line.

‘If I had to concisely describe mortgage insurance in one sentence or less, I would say that it protects the lender while allowing borrowers to purchase refi with less than 20% down.’

How PMI Actually Works

Think of Private Mortgage Insurance as a tool that buyers can use to attract more lenders instead of an added cost to buy a home. This change in approach, in and of itself, will better serve borrowers in short and long term.

PMI insures a lender against a default by the buyer. Without this insurance, the ability to buy a home would be significantly more difficult for Americans as there would be less money available to lend.

Additionally, the insurance doesn’t last indefinitely. Buyers can drop the insurance as soon as they have 20% equity in their home. The insurance will cancel automatically once they reach 22% equity, just in case they forget.

One more caveat of PMI is it’s flexible. It can be structured in many ways based on the needs of the homeowner at closing. This includes adding the cost into monthly payments, paying the premium upfront, or a combination of both.

‘Definitely not a barrier (PMI)…a bridge helping a borrower go from tenant to owner. And it can be seen as a temporary stepping stone to help folks get into homeownership faster…’

Why Waiting May Cost Borrowers More Than PMI

In many scenarios, borrowers will wait to buy while they save for a larger down payment. Depending on the circumstances, this can cost them more money in lost equity than they save from reducing or eliminating PMI.

Let’s compare two common situations in Florida:

Buyer #1:

- Purchases a home today with 5% down

- Pays PMI

Buyer #2:

- Waits to buy for a year or more to save 20% for a down payment

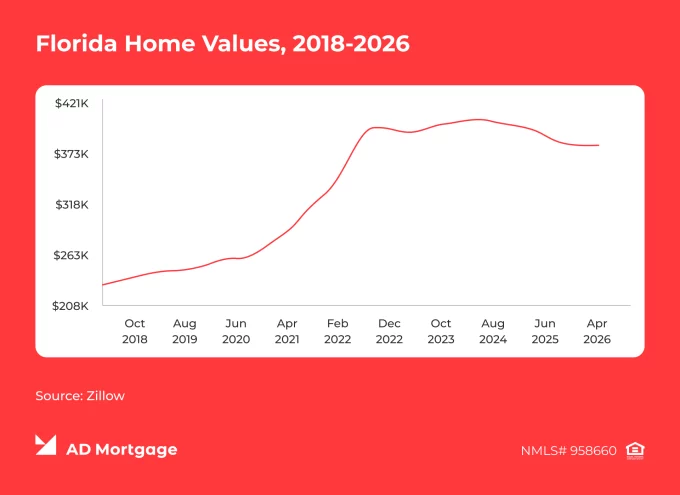

According to Zillow, over the past five years (2020-2025), Florida home values have appreciated by roughly 60%, depending on the market. While future appreciation is never guaranteed, this illustrates why some buyers who delayed purchasing in order to avoid PMI may have faced significantly higher home prices later.

As a result, Buyer #1 is much better off and Buyer #2 may have made little headway towards the 20% down payment. Here is a breakdown:

- Home price in 2020: $275,000

- 5% down payment: $13,750

- Buyer pays PMI

- Same home in 2025: approximately $440,000

- Required 20% down payment now: $88,000

Buyer #1 now has more than 20% equity in their home and has stopped paying PMI while continuing to build wealth. Meanwhile, Buyer #2 has made little progress towards their goal of homeownership.

When PMI Makes Sense

Paying PMI is worth considering in several scenarios. Brokers and loan originators should consider these when discussing options with borrowers:

- First-time Homebuyers. Allows quicker entry into the market.

- Relocating Families. Provides flexibility during time-sensitive purchases.

- Buyers in Growing Markets. Helps buyers secure a home before they get outpriced.

- Buyers Wanting to Preserve Savings. Provides flexibility for funding home-improvement projects, emergencies, and/or other financial goals.

‘Mortgage insurance PMI is not one size fits all. It’s customizable. Maybe the borrower is not comfortable with carrying a monthly payment, or they’d rather pay an upfront single premium payment. or they can combine the two – they can do a monthly plus that.’

Final Thoughts

PMI is one of the most misunderstood aspects in home financing. Although it adds to costs, it also serves as an excellent tool to get borrowers into homes.

Of course, every situation is unique, and borrowers and brokers should explore all the specific nuances as they plan their lending approach. We highly recommend covering the following questions during the early phases of buying:

- What financing options are available for this scenario?

- How much equity might be built by purchasing sooner than later?

- How much would PMI cost in the current scenario?

- How long would it likely take to pay it?

- What would waiting cost?

The goal is to make a decision that best fits the borrowers individual situation and current market conditions. As Albert Martinez explains in the AD Mortgage Digest, understanding how PMI works will help buyers and brokers better evaluate their options when starting the process.

Brokers are encouraged to utilize AD Mortgage’s resources in evaluating a scenario. Contact us with the details and get a range of options to fit your situation.