Post content:

One of the key benefits of conventional loans usually highlighted is a low down payment. High loan-to-value (LTV) ratio and favorable rates are good for borrowers, but how are lenders able to provide loans on such terms? The answer is: because PMI on conventional loans protects them from losing their money.

This article explains how private mortgage insurance works and suggests ways brokers can present PMI to their clients.

Key Takeaways

- Private mortgage insurance, or PMI, on conventional loans protects the lender when the borrower makes a down payment of less than 20%.

- The borrower can cover PMI at closing, with mortgage payments during the life of the loan, or combine two of these approaches. Sometimes, the lender covers PMI, but the interest rate increases.

- PMI is removable – it can be canceled at 20% equity, provided the borrower is current on payments and it is cancelled automatically once the 22% equity threshold is reached.

Is PMI Required on a Conventional Loan?

Generally, yes, PMI is required if putting less than 20% down on the home. Later, when the borrower reaches 20% home equity, PMI can be canceled.

The same rule applies to refinancing – if with the new loan the borrower still has an LTV above 80%, PMI is required.

Choose among 20+ programs and get

Looking for a suitable loan program?

a detailed loan calculation

See what conventional loan is in the previous article.

When PMI is Not Required

PMI on a conventional loan is usually not required when the borrower makes a down payment of 20% or higher.

Additionally, there are rare cases when PMI is covered by the lender. Then, the costs are built into a higher interest rate, which might be less cost-effective in the long run.

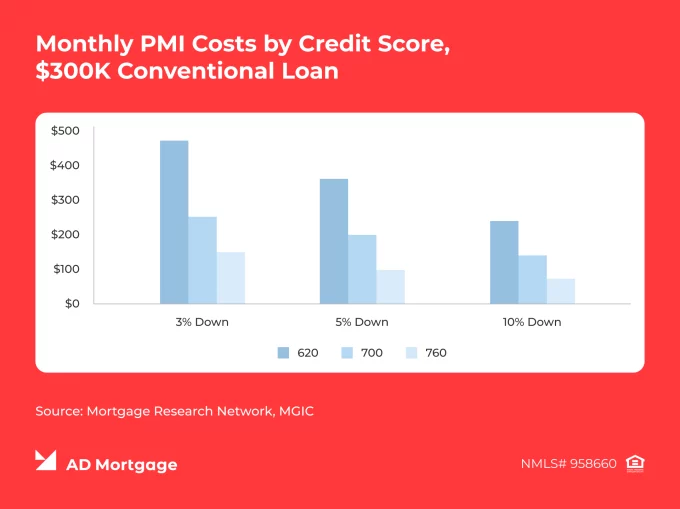

How Much Does PMI Cost on a Conventional Loan?

PMI can be paid at closing, during the life of the loan, or as a combination of both monthly and upfront premiums.

- Upfront PMI is typically between 1% and 1.5% of the loan amount, which can significantly increase closing costs.

- Ongoing PMI usually ranges between 0.3% and 1.5% of the loan amount. It is paid until the borrower’s equity reaches 20% when it can be canceled upon request or 22% when it is terminated automatically.

Estimates based on data from NerdWallet.

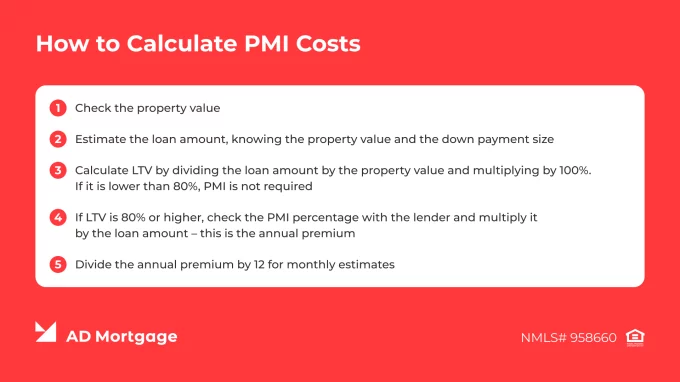

How PMI is Calculated

Conventional loan PMI is based on the original loan amount. Monthly payments are more common than upfront ones, and PMI is calculated annually and divided into 12 monthly payments.

How can brokers calculate exact insurance costs for their clients?

- Check the property value

- Estimate the loan amount, knowing the property value and the down payment size

- Calculate LTV by dividing the loan amount by the property value and multiplying by 100%. If it is lower than 80%, PMI is not required

- If LTV is 80% or higher, check the PMI percentage with the lender and multiply it by the loan amount – this is the annual premium

- Divide the annual premium by 12 for monthly estimates

When Can PMI be Removed on a Conventional Loan?

PMI on conventional mortgage is not permanent – it can be canceled, and usually early in the life of the loan. There are two ways PMI is removed:

- Upon Request, when reaching 20% equity based on the original value or 80% LTV. Lenders typically require a history of on-time payments and may request a new appraisal to confirm the property value.

- Automatically, when reaching 22% equity based on original value or 78% LTV – but the borrower must be current on payments.

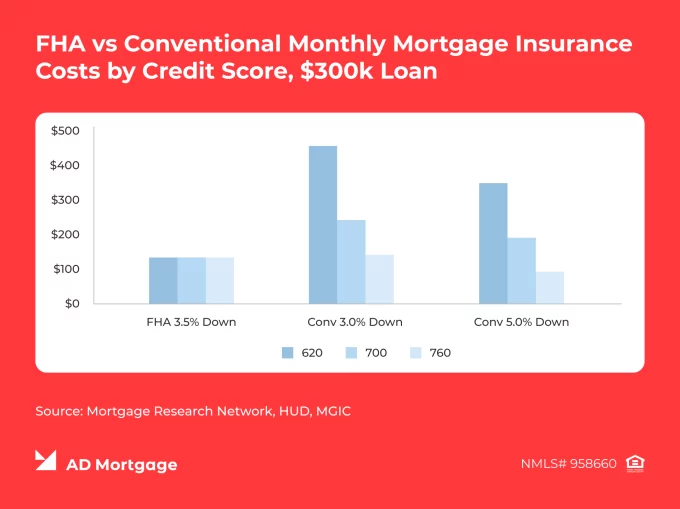

PMI on Conventional Loans vs FHA Mortgage Insurance

Borrowers often compare conventional loans with FHA mortgages, and mortgage insurance significantly impacts their final decisions. To clearly distinguish the difference between private mortgage insurance (PMI) and mortgage insurance premium (MIP), we have created this side-by-side comparison table.

| PMI on Conventional Loans | MIP on FHA Loans | |

|---|---|---|

| When Required | When down payment <20% | All FHA loans |

| Upfront Costs | 1%-1.5% of the loan amount, sometimes financed | 1.75% of the loan amount, can be financed |

| Annual Costs | Often 0.3%-1.5% | Often 0.15%-0.75% |

| Cancelation | Upon request at 20% equity, automatically at 22% equity | Automatically after 11 years if LTV ≤90%. Otherwise, for the life of the loan or until refinancing |

| Total Costs | Usually lower, no PMI with ≥20% down | Usually higher, especially with lower down payment |

In both cases, mortgage payments depend on a variety of factors – including, borrower profile, loan amount, and lender overlays. The graph below compares PMI vs. FHA mortgage insurance costs by different credit scores.

Broker Talking Points: How to Frame PMI

- ‘If you’re putting less than 20% down, PMI will be required. It can be canceled once you reach 20% equity, or automatically at 22%.’

- ‘Compared to FHA mortgage insurance, PMI on a conventional loan can often be removed sooner and may cost less overall. Let’s calculate the exact costs and compare your options.’

- ‘A 20% down payment helps you avoid PMI and may also improve your interest rate.’

Conclusion

Generally, PMI is required on conventional loans when the down payment is less than 20% (or the LTV exceeds 80%). The good news is that this insurance is not permanent. Brokers can explain PMI to borrowers not just as ‘you will pay PMI,’ but rather as ‘here’s why PMI applies, how much it may cost, and when it can be removed.’

Visit our Conventional Loan page to find the solutions that fit your client’s needs best: Conventional Loans | AD Mortgage

FAQ: Conventional Loan PMI Rules

Is PMI Always Required on a Conventional Loan?

Not always. PMI is only required on conventional loans when the down payment is less than 20%.

Do Conventional Loans Require PMI with 10% Down?

Yes. It can be canceled after the borrower builds 20% equity.

Do Conventional Loans Require PMI with 15% Down?

Yes. With a down payment below 20%, PMI is required.

When Can PMI be Removed from a Conventional Loan?

PMI can be canceled upon request when the borrower builds 20% of the home equity. Otherwise, it will be canceled automatically at 22% equity, as long as the borrower is current on payments.

Is PMI Automatically Canceled at 78%?

Yes, but the borrower must be current on payments.

Does PMI Protect the Borrower or the Lender?

PMI protects the lender in case the borrower defaults and is no longer able to maintain their loan.

Can a Conventional Loan Avoid PMI with a Higher Interest Rate?

Some lenders offer lender-paid PMI, so brokers can ask about these terms directly.

Is Conventional PMI Easier to Remove than FHA Mortgage Insurance?

Yes. PMI can be canceled at 20% equity, while MIP on FHA loans may last 11 years or for the life of the loan, depending on the down payment.

Choose among 20+ programs and get

Looking for a suitable loan program?

a detailed loan calculation

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again