Post content:

The second mortgage borrowing limit depends on a variety of factors – including home value, current mortgage balance, allowable CLTV or HCLTV, credit profile, income, property type, and lender program limits. This article explains how to estimate your client’s borrowing limit and also features a worked example.

Key Takeaways

- A second mortgage borrowing limit is determined individually based on the borrower’s financial profile, property characteristics, and the lender’s guidelines.

- Lenders determine the maximum second mortgage amount using CLTV and HCLTV. CLTV includes all outstanding balances relative to the property value, while HCLTV also includes the full HELOC credit limit.

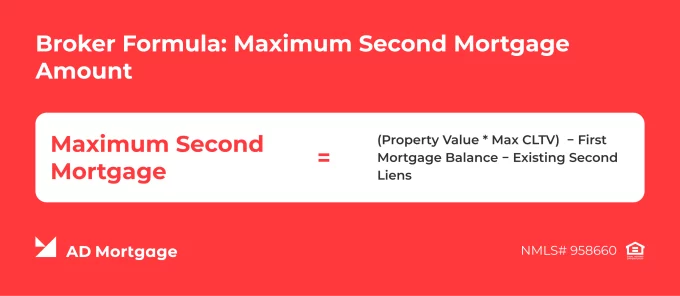

- The maximum second loan amount is calculated using the formula: Maximum Second Mortgage = (Property Value * Max CLTV) − First Mortgage Balance − Existing Second Liens.

- In most cases, the borrower cannot qualify for the maximum second mortgage amount because of lender caps and program restrictions.

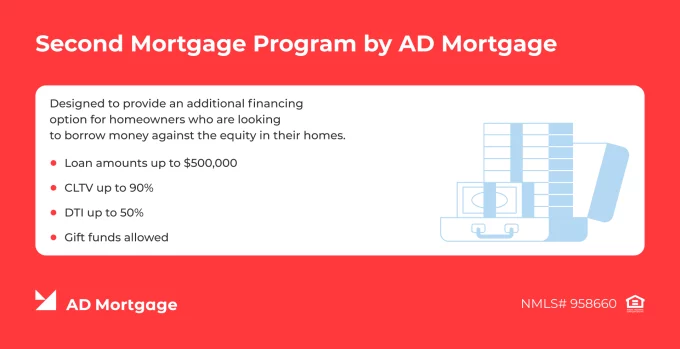

- AD Mortgage offers closed-end Second Mortgage loans with loan amounts up to $500,000, CLTVs up to 90%, and DTIs up to 50%.

What is the Second Mortgage Borrowing Limit?

The second mortgage borrowing limit is the maximum amount a borrower can qualify to borrow through a second mortgage. It is estimated based on factors related to the borrower’s financial profile, property type, and the lender’s requirements.

The main factors that affect the borrowing limit are the combined loan-to-value (CLTV) ratio and available home equity. Further in the article, we examine them in detail.

The Core Formula Brokers Use

Calculating how much your client can borrow through a second mortgage starts by determining the maximum debt amount allowed on the property. Note that even borrowers with great profiles and low first mortgage balances typically do not qualify for this amount because of existing debts and program restrictions.

Use the following formula to calculate the maximum second mortgage amount:

Maximum Second Mortgage = (Property Value * Max CLTV) − First Mortgage Balance − Existing Second Liens

How to use the formula step by step?

- Calculate the maximum debt amount allowed under the program requirements by multiplying the current property value by the lender’s maximum allowable CLTV (or HCLTV for HELOCs).

- Determine the amount of equity left after accounting for the primary loan by deducting the outstanding balance of the first mortgage from the total allowable debt.

- In case there are any existing second liens in place, subtract their outstanding balances.

- Check that the resulting amount fits into the program’s maximum loan amount requirements.

AD Mortgage differentiates itself through continuously updating programs to match changing market conditions. Check out our flexible Second Mortgage program requirements to help your clients assess home equity without refinancing: Second Mortgage | Second Home Loan | AD Mortgage

CLTV vs HCLTV: What is the Difference?

CLTV, or Combined Loan-to-Value, measures the outstanding balances secured against a property as a percentage of its current value. The first mortgage balance and any second lien are included in the calculation. In the case of an existing HELOC, only the amount that was actually used is considered debt under CLTV.

HCLTV, on the other hand, includes the full HELOC credit limit – not just the amount that was drawn. This unused amount matters because it increases lender risk exposure.

As a result, HCLTV is a stricter test compared with CLTV, and the approach used directly impacts loan qualification and borrowing capacity.

Worked Example: $500,000 Home Value

Exploring a real-life example will help you easily explain second mortgage amounts to your clients. Note that the example is for illustrative and educational purposes only.

Borrower Situation

A homeowner owns a single-family residence, worth $500,000. The outstanding first mortgage balance is $300,000, and there are no existing second liens. The borrower wants to take a second mortgage from the lender, who allows CLTV up to 80%.

Maximum Second Mortgage Amount Calculation

Let’s fill in the formula with the numbers and calculate the outcome:

Maximum Second Mortgage = (Property Value * Max CLTV) − First Mortgage Balance − Existing Second Liens

Maximum Second Mortgage = ($500,000 * 80%) − $300,000 − $0

Maximum Second Mortgage = $100,000

Actual Second Mortgage Amount: While $100,000 is the maximum estimated amount, the borrower will typically not qualify for the full amount. Due to program caps and underwriting requirements, the final approved amount may be lower. AD Mortgage provides flexible underwriting for out-of-the-ordinary borrowers, helping partners serve a wide variety of scenarios.

What Reduces the Amount a Borrower Can Get?

The most important question at this point – now that we know how to calculate the maximum second mortgage amount – is what factors reduce the final approved second mortgage. All these factors fall into four main categories.

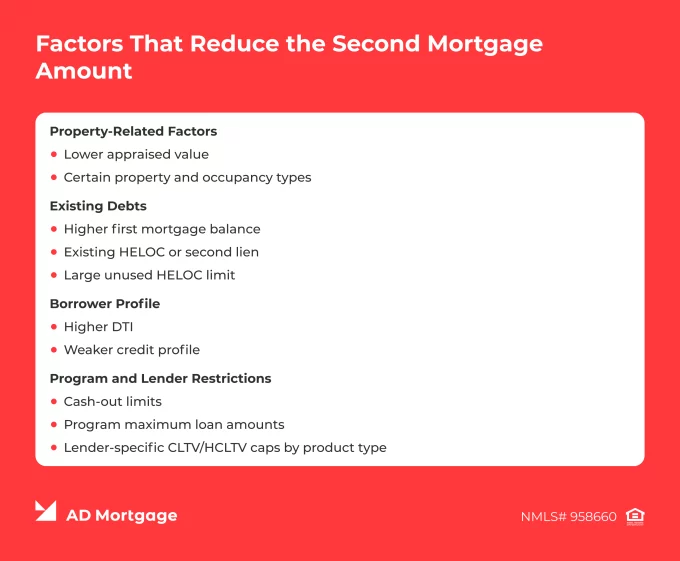

Property-Related Factors

- A lower appraised value directly lowers the maximum borrowing capacity

- Property type – certain properties, such as condos, might have stricter lender requirements

- Occupancy – investment properties usually have tighter restrictions

Existing Debts

- A higher first mortgage balance

- Existing HELOC or second lien

- A large unused HELOC limit

Borrower Profile

- Higher DTI can limit loan approval regardless of equity

- A weaker credit profile may reduce the maximum CLTV allowed or affect pricing eligibility

Program and Lender Restrictions

- Cash-out limits

- Program maximum loan amounts

- Lender-specific CLTV/HCLTV caps by product type

AD Mortgage Second Mortgage Program Considerations

In the current market, second mortgages are becoming increasingly popular, often outpacing refinance transactions. Do not miss the opportunity to capitalize on this trend!

AD Mortgage offers Second Mortgage loans with loan amounts up to $500,000 and CLTV ratios of up to 90%. Leave a Scenario Request, and our experts will contact you within 30 minutes with a tailored solution.

Should Borrowers Take the Maximum Available?

The decision on the second mortgage amount should be based on the borrower’s financial situation, payment comfort, and cash reserves. Simply qualifying for the maximum amount is not enough, as over-borrowing can increase financial risk.

The broker’s role is to carefully evaluate the client’s situation and recommend a loan amount that matches the purpose of the second mortgage. Explain to your borrower that maximum eligibility is not always the best financial decision.

Broker Talking Points

- ‘Why do you want to take out a second mortgage? The purpose of the loan will help determine the borrowing strategy.’

- ‘I will calculate the maximum second mortgage amount you may qualify for. Keep in mind that lender caps, underwriting requirements, and other factors may lower the final approved loan amount.’

- ‘If you have an existing HELOC, the lender might consider the full limit as debt, not only the drawn amount. This could reduce your borrowing capacity.’

Conclusion

The second mortgage maximum loan amount depends on the borrower’s financial profile and the overall loan scenario. However, various factors may reduce the amount the borrower qualifies for – this is where brokers play a key role in setting clear expectations.

AD Mortgage has 20 years of experience in the mortgage industry and offers a wide range of mortgage solutions, including the Second Mortgage program. Submit a loan scenario to receive a tailored solution in 30 minutes.

FAQ: How Much Can I Get with a Second Mortgage

How Much Can You Borrow on a Second Mortgage?

The maximum second mortgage loan amount is calculated based on the lender’s maximum allowable CLTV ratio. The lender compares the outstanding balances of the existing loans to the property’s value to assess risk. However, various factors, such as underwriting requirements, may reduce the amount the borrower can qualify for.

How Do You Calculate Second Mortgage Borrowing Power?

To calculate the maximum amount of a second lien, use the formula: Maximum Second Mortgage = (Property Value * Max CLTV) − First Mortgage Balance − Existing Second Liens.

What is CLTV?

CLTV, or Combined Loan-to-Value, is a metric used by lenders to assess risk by comparing the total secured loan balances to the property’s value.

What is HCLTV?

HCLTV, or Home Equity Combined Loan-to-Value, functions similarly to CLTV but also includes the full HELOC limit, not only the used amount.

Does a HELOC Count Even if It is not Fully Used?

That depends on the metrics used – yes, in HCLTV calculations and no, in CLTV calculations.

What is the Maximum Loan Amount for a Second Mortgage?

The maximum second mortgage loan amount is calculated individually based on the borrower’s outstanding loan balances, property value, loan purpose, lender caps, and other factors.

Can You Borrow up to 100% of Home Equity?

No. Lender CLTV requirements limit the maximum second loan amount, often allowing a CLTV ratio of only 80%-85% of the property value. AD Mortgage helps brokers offer more financing options to borrowers by accepting CLTV ratios of up to 90% for the Second Mortgage program.

What Reduces the Amount You Can Borrow?

A high first mortgage balance, an existing HELOC or second lien, a weaker borrower profile, lender-specific requirements, and other factors can lower the second mortgage amount a borrower can qualify for.

Is Home Value or Mortgage Balance More Important?

There is no single more important factor in the CLTV calculation. Both home value and mortgage balance directly influence the metric.

Should Borrowers Take the Maximum Second Mortgage Available?

No. Borrowers are usually better off taking the amount that matches their purpose and financial situation instead of taking the maximum amount available.

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again