What is a Second Mortgage? Requirements, Pros and Cons, and How It Works in 2026

June 24, 2026

The short answer for ‘What is a second mortgage?’ is that it is a loan that is placed on a property which is already used as a collateral for a primary mortgage. In this case, a second mortgage stays subordinate to the first mortgage – meaning the first lender is first to be repaid if the borrower sells or defaults.

This article is an extensive guide on second mortgages for mortgage originators, helping them quickly navigate and educate their clients.

Key Takeaways

Second mortgages allow homeowners to borrow against the equity in a property that already serves as collateral for a primary mortgage. Homeowners use second mortgages for various purposes – from debt consolidation to home renovations and other major expenses.

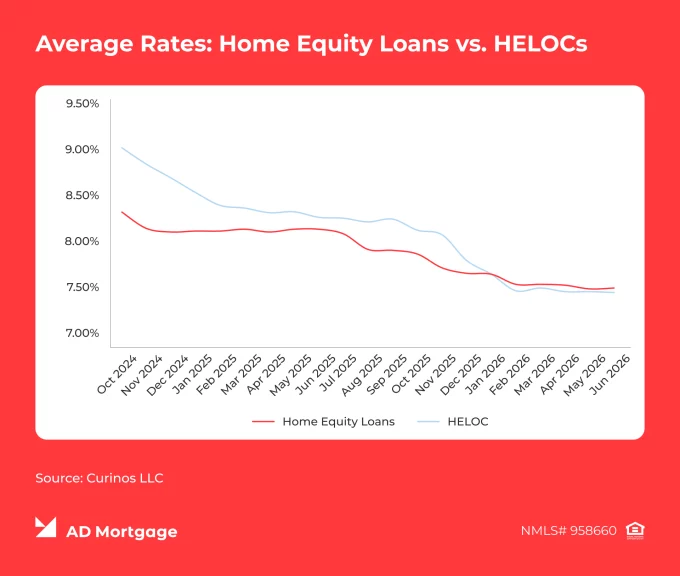

The most common types of second mortgages are home equity loans and home equity lines of credit (HELOCs). These products differ in how funds are accessed, their interest-rate structures, and repayment terms.

While second mortgages can provide access to additional funds, they also have potential drawbacks, including closing costs and typically higher interest rates than first mortgages.

A second mortgage is a loan secured by a property that already has a primary mortgage. A second lien is a lender’s legal claim on the property that serves as collateral for the loan.

When a borrower takes out a second mortgage, the lender places a second lien on the property.

These mortgages are called ‘second’ because they are subordinate to the primary mortgage. This means that if the borrower defaults and the property is sold or foreclosed upon, the second mortgage lender is second in line for repayment.

How Does a Second Mortgage Work?

The second mortgage process has its unique features compared to other mortgage products. Here are the key considerations about how second mortgages work that brokers should keep in mind:

The borrower keeps the first mortgage with its current terms. The home is used as collateral for both mortgages, and the second mortgage does not replace or refinance the existing mortgage.

The lender performs underwriting, reviewing equity, income, credit, DTI, property value, and lien position. Often, second-mortgage underwriting is stricter due to higher lender risk.

The two loans are repaid separately. The payment structure for second mortgages differs depending on the loan type – we will touch on this later in the article.

In a foreclosure sale, there is a strict lien priority: the second mortgage lender is paid only when the first mortgage lender is paid in full. Therefore, second mortgages carry higher risks for lenders, leading to typically higher interest rates than primary mortgages.

Types of Second Mortgages

There are five common types of second mortgages, each are similar but designed to meet different borrower needs.

A closed-end home equity loan provides a lump sum of money at closing. The loan terms are fixed, and the mortgage is repaid through equal monthly payments. This option is often used when homeowners need a large amount of money for a one-time expense such as paying medical bills or consolidating debt.

A home equity line of credit (HELOC)allows for borrowing money against the home equity up to a predetermined credit limit, pay it down, and then reuse it. In some ways, a HELOC functions similarly to credit cards. Often, borrowers choose HELOCs when they need to cover ongoing expenses or projects like renovations.

A fixed-rate second mortgage features an interest rate that remains unchanged throughout the loan term. These loans often overlap with home equity loans. However, a fixed-rate second mortgage can also include other types of loans.

A piggyback second mortgage is a loan taken out at the same time as the first mortgage, typically to reduce the amount borrowed under the primary mortgage or avoid private mortgage insurance. These loans are often called ‘80/10/10’ because of their structure: 80% primary mortgage, 10% second mortgage, and 10% down payment.

A standalone second mortgage is obtained after the first mortgage. It can be a home equity loan or a HELOC – ‘standalone’ reflects not the exact loan product but when the borrower obtains it.

The following comparison table highlights the differences between the main second mortgage types. It can be useful in your conversations with clients when educating them about these products.

Fund Disbursement

Interest Rate

Repayment Structure

Purpose

Closed-End Home Equity Loan

Lump sum

Fixed

Through equal monthly payments

One-time large expenses

Home Equity Line of Credit (HELOC)

Draw when needed

Not fixed, usually variable

Flexible withdrawals

Ongoing expenses

Fixed-Rate Second Mortgage

Lump sum

Fixed

Through equal monthly payments

One-time large expenses

Piggyback Second Mortgage

At home purchase

Fixed or variable

Through monthly payments, separate from first loan

Avoiding PMI, reducing down payment needs

Standalone Second Mortgage

After the first mortgage

Fixed or variable

Through monthly payments, separate from first loan

Accessing home equity

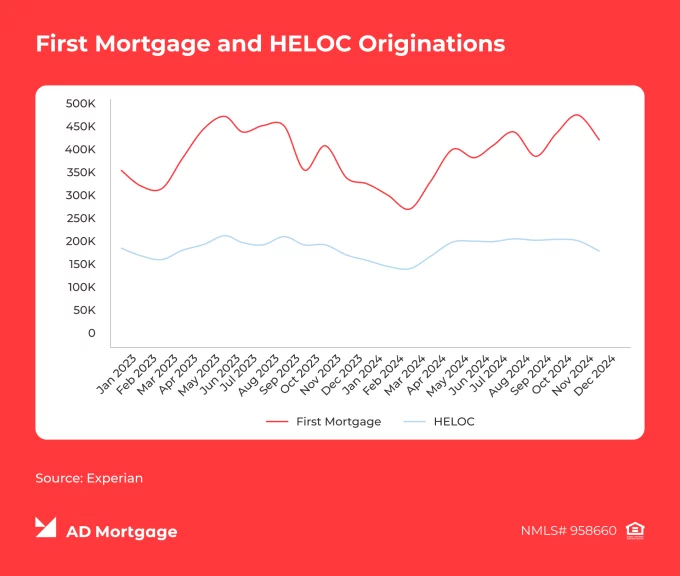

Why Borrowers Use Second Mortgages in 2026

Borrowers choose second mortgages for various purposes. Does the broker need to be aware of these reasons? Yes, definitely. Understanding a borrower’s objectives helps brokers structure loans, align them with the borrower’s long-term goals, and account for the borrower’s risk profile.

So, what are the most common reasons for obtaining a second mortgage loan?

Access Equity While Preserving a Low-rate Primary Mortgage

In 2026, refinancing is rarely an option due to increased mortgage rates. Therefore, if a borrower wants to access home equity, a second mortgage may be their primary choice.

However, as a second mortgage leads to higher ongoing costs and potential payment shock, mortgage originators need to compare the total cost of a second mortgage against a cash-out refinance. This will help them choose the most appropriate solution for their clients.

Fund Home Improvements

Homeowners might need additional funds for home renovations, repairs, or additions. Sometimes, these improvements might increase home value.

The broker’s task in such a case is to analyze the borrower’s expected expenses and suggest the correct second mortgage type. When the costs are already known and the improvements are expected to be made in a short time, home equity loans might work best. HELOCs may be a better fit for phased renovations with uncertain expenses.

Consolidate Debts

Second mortgages can be used to pay off high-interest debts, such as credit card balances.

However, it is crucial to ensure that the borrower is not simply converting short-term unsecured debt into long-term secured debt without a clear repayment plan. When consolidating debts, the borrower must have a clear financial benefit, such as a more efficient repayment structure or lower monthly costs.

Purchase Another Property

Equity can be used to fund a down payment on a second home or vacation property. To carry multiple mortgage obligations, the borrower must have sufficient reserves, consistent cash flow, and an overall strong profile. The broker’s role is to accurately assess whether the borrower will be able to handle the increased payments.

Cover Unexpected Costs

Borrowers might need cash when unexpected circumstances occur – for example, medical bills or legal expenses. Second mortgages can be a lower-cost funding source, compared with other unsecured alternatives.

The key thing to consider in such cases is whether financial issues are temporary or ongoing. If the problem is consistent, taking on an additional debt burden might not be the right choice.

Invest in Rental Properties

Leveraging equity to purchase investment properties is a prominent, yet high-risk strategy. Brokers should carefully evaluate borrower cash flow and contingency plans to ensure their clients can handle investment purchases.

Second Mortgage Requirements

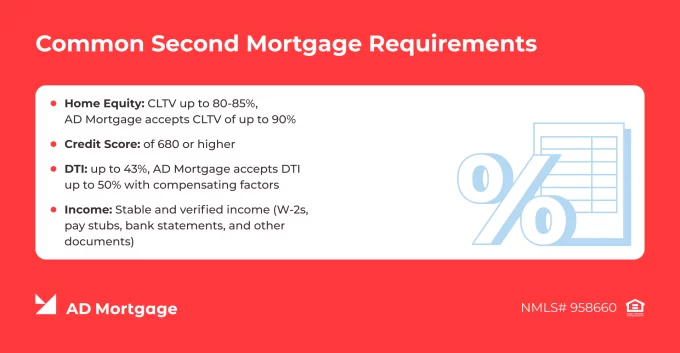

Second liens carry higher risks for lenders and therefore the underwriting process for second mortgages is often more complex and time-consuming. As with other loan types, the requirements vary depending on the lender and loan guidelines. However, there are standard qualification criteria that many lenders follow.

Home Equity and CLTV

Home equity is the core collateral factor. It is measured by Combined Loan-to-Value (CLTV), which includes both the first and second mortgage balances.

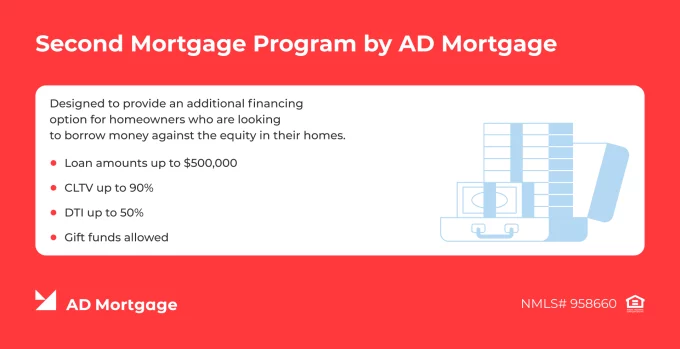

Often, lenders require a maximum CLTV of 80-85% – though AD Mortgage’s Second Mortgage program accepts up to 90%. However, a higher CLTV typically results in a tighter, more detailed review.

Credit Score and Mortgage History

Credit profile demonstrates borrower creditworthiness and their ability to manage debt obligations. Lenders carefully review borrower credit scores, payment history, and recent credit events to assess loan risk.

For second mortgages, lenders typically have stricter credit score guidelines and might require stronger compensating factors to support lower scores.

AD Mortgage accepts a minimum FICO of 680 and does not require a credit score for Foreign Nationals.

DTI

To ensure that the borrower is able to comfortably manage their obligations, lenders review the Debt-to-Income (DTI) ratio. Both first and second mortgages are included in the monthly obligation calculation.

AD Mortgage accepts up to 50% DTI under the Second Mortgage program. It is important to note that DTI is not considered independently – it is tightly connected with reserves, income stability, loan purpose, and other factors.

Income and Asset Documentation

The borrower must demonstrate stable and sufficient income. Usually, W-2s, pay stubs, bank statements, or other forms of alternative documentation may be acceptable. Additionally, lenders require verification of assets, reserves, funds to close, and gift funds.

Property Type and Occupancy

The type of property has a significant impact on its liquidity, so not all property types may be eligible with every lender. While owner-occupied primary properties are the most common, other property types, including second homes and investment properties, may also be eligible, though with stricter requirements.

Loan Amount and Program Limits

The maximum loan amounts vary, but AD Mortgage offers second mortgages starting from $50,000 and up to $500,000. The maximum cash-in-hand amount is also $500,000.

Requirements for Foreign Nationals and Non-Permanent Resident Borrowers

There are certain second mortgage programs available for those who do not have U.S. residency. While offering greater flexibility in some areas, these solutions typically feature stricter requirements to manage higher risk.

Common guidelines for Foreign Nationals and non-permanent resident borrowers often include:

Investment-property only

No FICO review – instead, lenders evaluate alternative factors such as assets, bank statements, and liquidity

Additional documentation requirements

Common Reasons a Second Mortgage Gets Denied

Second mortgages carry higher risks for lenders, and therefore, the underwriting process is stricter and more time-consuming. Out of many reasons while application might be declined, these are the most common:

Insufficient equity

CLTV too high

DTI too high

Weak mortgage history

Documentation gaps

Title issues

Property ineligibility

Recent credit event

Unclear use of funds or repayment risk

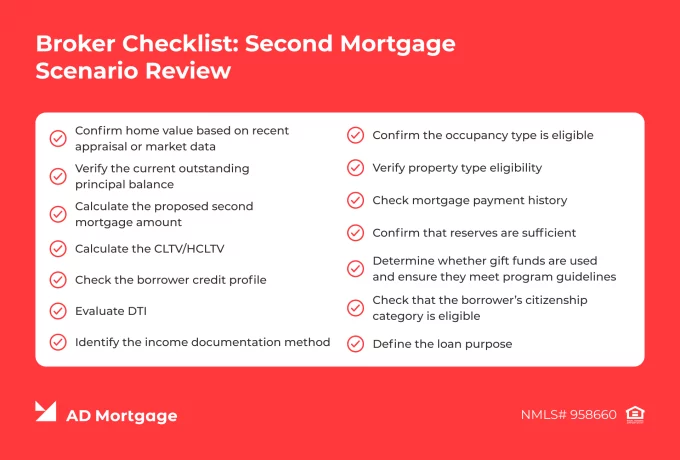

Broker Checklist: Second Mortgage Scenario Review

To come prepared and not miss any step of the process, follow this checklist:

Confirm home value based on recent appraisal or market data

Verify the current outstanding principal balance

Calculate the proposed second mortgage amount

Calculate the CLTV/HCLTV

Check the borrower credit profile

Evaluate DTI

Identify the income documentation method

Confirm the occupancy type is eligible

Verify property type eligibility

Check mortgage payment history

Confirm that reserves are sufficient

Determine whether gift funds are used and ensure they meet program guidelines

Check that the borrower’s citizenship category is eligible

Define the loan purpose

How Much Can a Borrower Get with a Second Mortgage?

Your clients will probably ask you how much cash they can get with a second mortgage. This amount can be easily calculated.

First, determine the current home value based on appraisals and other documents, the first mortgage balance, and the maximum CLTV allowed by the lender. Based on these numbers, you can find the loan amount of a second mortgage using the formula:

CLTV = (First Mortgage + Second Mortgage) ÷ Property Value

In the case of a HELOC, the HCLTV is calculated instead of CLTV. It is very similar, but includes the full credit limit of any HELOC:

HCLTV = (First Mortgage + Proposed Second Mortgage + Full HELOC Limit) ÷ Property Value

It is important to note that not all equity may be available for borrowing. The maximum available loan amount depends on the borrower’s available equity and the lender’s CLTV or HCLTV limits. Additionally, lenders can impose other program limits based on credit score, property type, and other factors.

Let’s look at an example – note that it is used for illustrative and educational purposes only. A borrower owns a home valued at $500,000, no existing HELOC, and their first mortgage balance is $300,000. A lender accepts a maximum CLTV for a second loan of 90%.

1) Calculate the maximum total debt allowed by the second loan lender:

$500,000 * 90% = $450,000

2) Calculate the maximum second loan amount by subtracting existing mortgage debts:

$450,000 – $300,000 = $150,000

Then, $150,000 is the maximum second mortgage amount for which the borrower may qualify.

However, if the borrower has an existing HELOC, it must be included in the calculations. Let’s use the same example but assume that the borrower has an existing HELOC with a credit limit of $50,000.

Then, subtract the full credit limit from the amount that we got in the second step:

$150,000 – $50,000 = $100,000

In this scenario, the borrower can qualify for a second mortgage of up to $100,000.

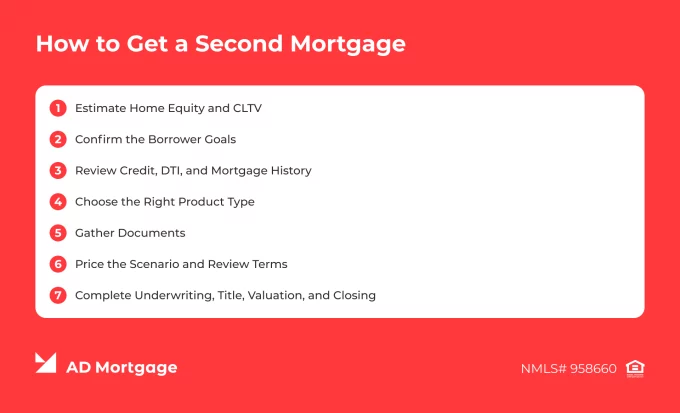

How to Get a Second Mortgage: Quick Answer

From the mortgage originator’s side, the second mortgage process consists of seven major steps:

1. Estimate Home Equity and CLTV

Determine the property’s current market value and calculate available equity, based on the lender’s CLTV requirements, the borrower’s outstanding balance, and expected second mortgage amount. This will help determine the maximum borrowing capacity.

2. Confirm the Borrower Goals

Checking the purpose of the second mortgage is crucial for choosing the right solution. The common reasons include home renovations, debt consolidation, and covering unexpected expenses, without refinancing the first mortgage.

3. Review Credit, DTI, and Mortgage History

To ensure the borrower’s creditworthiness and financial strength, check their credit score, mortgage payment history, DTI, reserves, and recent credit events. These factors directly impact the approval and loan terms, so brokers should pay extra attention to each detail.

4. Choose the Right Product Type

Based on the borrower’ profile and their strategic goals, choose the suitable mortgage solution:

Fixed-rate home equity loans offer a lump sum at closing for one-time large expenses and feature predictable monthly payments

HELOCs are great for ongoing or variable expenses as they provide flexible access to funds

While not being a second mortgage, a cash-out refinance allows to access home equity and reset the first loan terms

DSCR and other investor programs allow to purchase investment properties and cover debt service using property cash flow

5. Gather Documents

To avoid delays and back-and-forth messages during underwriting, carefully collect full documentation. This typically includes:

Mortgage statement

Income documentation

Asset verification

Identification and entity documents if applicable

Homeowners insurance

Property information

Title and lien documentation

Payoff statements if required

Renovation estimates if applicable

Lease or rental agreements for investment properties

6. Price the Scenario and Review Terms

When the borrower’s eligibility is confirmed and their strategic goals are clear, the next step is pricing a scenario. The broker compares available lender products and proposed loan amounts, rates, monthly payments, and other terms to choose the right solution.

Submit a Scenario Request, and our experts will contact you within 30 minutes with a tailored solution.

7. Complete Underwriting, Title, Valuation, and Closing

During underwriting, the lender reviews borrower and property information to ensure borrower eligibility. At the same time, the title company verifies lien position and ensures a clear title.

Once all conditions are met, closing disclosures are issued where applicable, and the loan proceeds to final signing and funding.

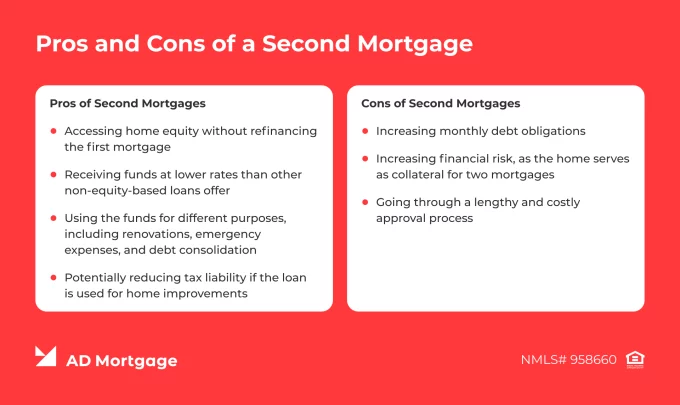

Pros and Cons of a Second Mortgage

Second mortgages are not a universal solution. They should be used strategically, aligning with the borrower’s long-term goals. Explore potential drawbacks of these mortgages and educate your clients about both positive and negative features.

Pros of Second Mortgages

Second mortgages offer several benefits:

Accessing home equity without refinancing the first mortgage

Receiving funds at lower rates than other non-equity-based loans offer

Using the funds for different purposes, including renovations, emergency expenses, and debt consolidation

Potentially reducing tax liability if the loan is used for home improvements

Cons of Second Mortgages

Despite the benefits, there are disadvantages that must be considered:

Increasing monthly debt obligations

Increasing financial risk, as the home serves as collateral for two mortgages

Going through a lengthy and costly approval process

Second Mortgage vs HELOC vs Cash-Out Refinance

When a homeowner has a first mortgage and needs to get extra cash, they usually compare three options – home equity second mortgages, HELOCs, and cash-out refinancing. To help you and your clients make informed decisions, we have created a table below comparing these solutions based on key features.

Home Equity Second Mortgage

HELOC

Cash-Out Refinance

Funding Method

Lump sum at closing

Line of credit

Old loan is replaced with the new one, and the difference is provided in cash

Rate Type

Typically fixed

Typically fixed

Typically variable

Depends on the new loan terms

First Mortgage

Terms do not change

Terms do not change

Rate and terms are replaced with those of the new loan

Payment Stability

Stable, predictable monthly payments

Payments vary based on changes in interest rates and outstanding balances

Depends on the new loan terms

Best Fit

Large, one-time expenses

Ongoing or unpredictable expenses

Accessing home equity while potentially improving mortgage terms

Risks

Additional debt secured by the home, increasing foreclosure risk in case of default

Variable rates may increase borrowing costs and monthly payments

May result in a higher interest rate and higher long-term borrowing costs

Who is Best Suited for a Second Mortgage?

Some borrowers can benefit most from second mortgages, for example:

Homeowner with strong equity who wants to keep the first mortgage

Borrower funding a specific one-time project, such as a home renovation

Borrower consolidating high-interest debt with a clear repayment plan

Investor with equity and documented cash-flow strategy

Borrower whose first mortgage rate is worth preserving

Do you have clients in similar situations? Submit a scenario request, and our experts will contact you within 30 minutes with a tailored solution.

The following scenarios may require additional analysis before choosing a second mortgage:

Borrowers with a tight DTI ratio

Borrowers with unstable income

Properties with a risk of value decline

Borrowers with limited cash reserves

Borrowers without a clear payoff strategy

Common Borrower Misconceptions about Second Mortgages

‘I can borrow all of my home equity’. → No, lenders limit the maximum loan amount with CLTV or HCLTV and may impose other restrictions. Using the formula we shared above, you can calculate the maximum loan amount of the second mortgage.

‘The rates are always high’. → While second mortgage rates are higher than first mortgages, they are lower than other non-equity-secured loans.

‘HELOCs and second mortgages are the same thing’. → No. HELOCs are a type of second mortgage, which offers a revolving credit line. Another common type is a home equity loan that features a lump sum at closing and fixed payments.

Example Borrower Scenarios

To better understand in which cases second mortgages bring the most value, let’s look at the following examples.

Restaurant Owner Wants to Leverage Equity to Grow the Business

The borrower had a mortgage on their primary residence with an appealingly low interest rate of 3.25%. They wanted to access their home equity and obtain additional funds to expand their restaurant business.

Refinancing was not an option, as it would have increased the interest rate on the existing mortgage. Therefore, an AD Mortgage Account Executive suggested a Second Lien solution using a 12-month Bank Statement program. This allowed the borrower to preserve their low first-mortgage rate while accessing equity and maintaining an affordable monthly payment.

Experienced Investor Renovating Properties

An investor with a large REO portfolio wanted to access cash quickly to fund renovations and repairs. They had several first mortgages with loan amounts ranging from $200,000 to $400,000 and interest rates between 5.25% and 6.55%.

Because the goal was to close financing within a shorter timeframe, the Account Executive recommended three DSCR Cash-Out second lien transactions. This strategy allowed the investor to keep the existing mortgage rates and access cash faster, with minimal documentation required.

Second mortgages are subordinate liens secured by properties that already have a first mortgage. This option fits borrowers who want to access equity without refinancing their existing mortgage and changing its terms.

When choosing a second mortgage solution, it is crucial to consider not only a rate, but the total impact. Submit a Scenario Request to receive a best-fit solution for your client case.

A second mortgage is a loan secured by a property that already has a first mortgage. These loans are subordinate, meaning they rank first mortgages in repayment priority.

Is a Second Mortgage the Same as a Home Equity Loan?

No. A home equity loan is a type of second mortgage that provides a lump sum at closing and fixed monthly payments. Another common type of second mortgage is a HELOC, which features a revolving line of credit and is often used similarly to a credit card.

Is a HELOC a Second Mortgage?

A HELOC, or home equity line of credit, is a type of second mortgage. Unlike home equity loans, HELOCs offer a revolving line of credit rather than a lump sum at closing.

How Much Equity Do You Need for a Second Mortgage?

Most lenders require borrowers to have at least 15% to 20% equity to qualify for a second mortgage. However, the requirements depend on the loan program and the borrower’s overall profile, so stricter guidelines may apply.

What Credit Score is Needed for a Second Mortgage?

Generally, a minimal credit score of 620 is required. However, requirements vary by lender and loan type. A higher FICO score can help borrowers qualify for better terms and interest rates.

What DTI is Allowed for a Second Mortgage?

A common DTI benchmark for second mortgages is up to 43%. However, AD Mortgage may accept borrowers with DTIs of up to 50% when strong compensating factors are present.

How Does a Second Mortgage Work?

With a second mortgage, the borrower keeps the existing mortgage without changing its terms and receives a new loan secured by the same property. The two mortgages are then repaid separately according to their terms. In case of a foreclosure sale, the first mortgage is repaid in full before any proceeds are used to repay the second mortgage.

Can You Have a Second Mortgage and a First Mortgage at the Same Time?

Yes. A second mortgage exists alongside the first mortgage, and borrowers make separate payments on each loan.

What Can a Second Mortgage be Used for?

Second mortgages can be used for a variety of purposes, including home renovations, debt consolidation, unexpected medical expenses, and education costs.

What are the Risks of a Second Mortgage?

Second mortgages increase debt obligations, leading to higher financial risk, including the potential for foreclosure if payments are not made.

How Much Can You Borrow with a Second Mortgage?

The maximum available amount can be calculated using the formula: Maximum Second Mortgage = Home Value * Maximum CLTV − First Mortgage Balance − Existing HELOC Limit (if any).

Is a Second Mortgage Better than a Cash-Out Refinance?

There is no universally better option. The choice between a second mortgage and a cash-out refinance depends on the borrower’s financial goals, existing first mortgage terms, and lender program guidelines.

Can a Second Mortgage Affect Refinancing?

Yes. A second mortgage can affect refinancing a primary mortgage, as it adds risk for lenders. In many cases, lenders require that the second mortgage is paid off before the first mortgage is refinanced.