Post content:

The question of what solution to choose – second mortgage vs. HELOC vs. cash-out refinancing – arises when a borrower wants to access home equity. However, the right choice depends on the borrower’s situation and strategic goals: while home equity second mortgages and HELOCs allow borrowers to keep their first mortgage on its current terms, a cash-out refinance replaces the primary loan with a new one.

This article compares the three options in detail, helping brokers match their clients with the right solution.

ADD US AS A PREFERRED SOURCE ON GOOGLE

Key Takeaways

- Cash-out refinancing, home equity loans, and HELOCs are useful options for homeowners to access equity and obtain extra cash to cover expenses. However, these solutions come with costs and may increase overall debt obligations.

- Second mortgages are loans taken in addition to a primary mortgage, using the same property as collateral. Home equity loans are often used to cover one-time, large expenses, while HELOCs are typically used for ongoing or unpredictable borrowing needs.

- Cash-out refinancing follows a different approach – it replaces the first mortgage with a new one on updated terms. The borrower receives the difference between the new loan amount and the outstanding mortgage balance in cash.

Second Mortgage vs HELOC vs Cash-Out Refinance: Quick Answer

Depending on the borrower’s profile and strategic goals, second mortgages or refinancing might work best. Second mortgages are secured by the same property as the first loan, which is kept with its current terms, while refinancing replaces the existing loan with a new one with new terms.

In simple terms, a home equity second mortgage provides a lump sum at closing, a HELOC offers a credit line that can be used when needed, and cash-out refinancing is the replacement of a first mortgage with another one, while allowing the borrower to receive the difference in cash.

Side-by-Side Comparison Table

The crucial point in comparing these three options is that they are not interchangeable. Instead, home equity second mortgages, HELOCs, and cash-out refinancing serve different borrower needs, and the purpose must be the primary decision driver.

The following comparison table highlights the key features of each option and can be used to help your clients shape a clearer understanding of how they differ in structure, cost, and mortgage impact.

| Home Equity Second Mortgage | HELOC | Cash-Out Refinance | |

|---|---|---|---|

| Funding Method | Lump sum at closing | Line of credit | Old loan is replaced with the new one, and the difference is provided in cash |

| Rate Type | Typically fixed | Typically variable | Depends on the new loan terms |

| First Mortgage | Terms do not change | Terms do not change | Rate and terms are replaced with those of the new loan |

| Payment Stability | Stable, predictable monthly payments | Payments may vary based on interest rates and outstanding balance | Depends on the new loan terms |

| Best Use Case | Large, one-time expenses | Ongoing or unpredictable expenses | Accessing home equity while potentially improving mortgage terms |

| Best Borrower Fit | Borrowers who want to keep a low-rate first mortgage and avoid refinancing | Borrowers with strong credit, stable income, and need flexibility | Borrowers willing to reset their mortgage but seeking better terms or larger equity access |

| Risks | Additional debt secured by the home, increasing foreclosure risk in case of default | Variable rates may increase borrowing costs and monthly payments | May result in a higher interest rate and higher long-term borrowing costs |

| Closing Costs | Typically 2%-5% | Typically 2%-5% | Typically 2%-6% |

| Refinance Impact | No impact on first mortgage. Existing rate and terms remain unchanged | No impact on first mortgage. Functions as a separate revolving lien | Replaces entire first mortgage, resetting rate, term, and loan structure |

How a Second Mortgage Works

Home equity loans are one of the most common types of second mortgages. What are the specific features of these loans?

- By definition, a second mortgage takes a second lien position and stays subordinate to the primary loan. Therefore, in case of a borrower defaults, the second mortgage is repaid only after the first mortgage has been satisfied from foreclosure proceeds.

- Home equity second mortgages are close-end loans, meaning they offer borrowers a lump sum of money at closing.

- After receiving one-time funding, the borrower repays the loan through fixed, standalone monthly payments that are not connected to the payments of the primary mortgage.

How a HELOC Works

A HELOC is another common type of second mortgage. Unlike home equity loans, a HELOC provides greater flexibility in structure and access to funds:

- A HELOC provides a revolving credit line, functioning similarly to a credit card – a borrower can draw, repay, and redraw funds when needed, up to a pre-approved limit.

- During the draw period, which typically lasts five to ten years, the borrower can access funds freely, making monthly interest payments. Then, during 10 to 20 years of the repayment period, the outstanding balance is repaid in full.

- HELOCs usually feature a variable interest rate, and therefore payments may change over the life of the loan.

How a Cash-Out Refinance Works

While both home equity loans and HELOCs are types of second mortgages and have many similarities, cash-out refinancing functions completely differently:

- During refinancing, the first mortgage is replaced with a new loan. Therefore, the borrower no longer has obligations related to the primary mortgage – they have a new mortgage instead.

- The new mortgage comes with its own rate and term. With cash-out refinancing, the new loan amount exceeds the remaining balance on the current mortgage, and the borrower receives the difference in cash at closing.

- Unlike second mortgages, cash-out refinancing does not create an additional lien. Instead, it changes the first-lien structure and may reset the amortization.

Rate and Payment Stability Differences

Two crucial features to consider when matching your client with a financing solution are rate and payment stability.

Interest rates can be fixed (as in most home equity loans) or variable (as in HELOCs). While fixed-rate loans offer predictable payments, variable-rate loans usually come with greater flexibility – and potentially higher overall costs.

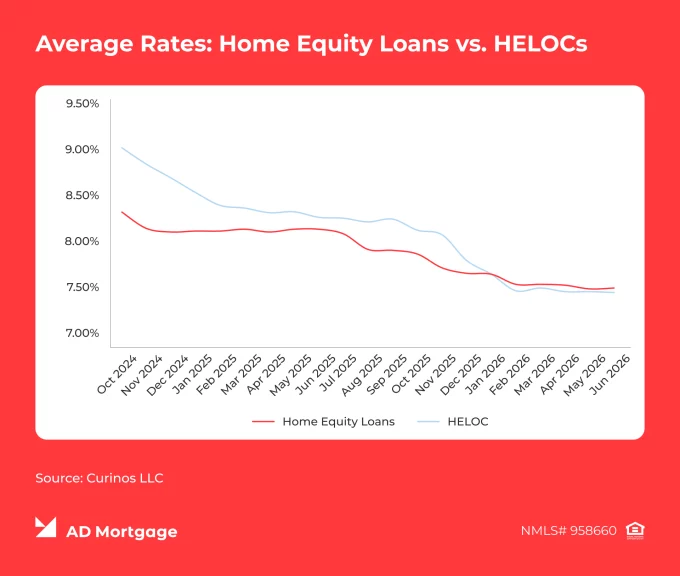

With cash-out refinancing, the first mortgage rate is a key parameter to consider. As it will be replaced with a new rate and term, it is crucial to ensure that giving up the current mortgage rate is worth it. In today’s higher-rate environment, refinancing may not always provide a lower interest rate than the borrower’s existing mortgage. Therefore, this option is less common at the moment, compared to second mortgages.

Best Use Cases for Each Option

The purpose is another point that matters. Whether the expenses are one-time or ongoing, predictable or not, and how the payment structure is going to be changed impacts the decision.

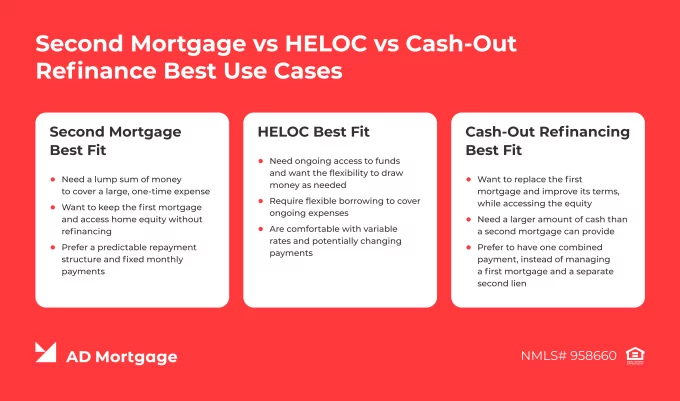

Second Mortgage Best Fit

Home equity loans may be a good fit for borrowers who:

- Need a lump sum of money to cover a large, one-time expense – for example, home renovation, medical bills, or debt consolidation

- Want to keep the first mortgage – for example, because of a low interest rate – and access home equity without refinancing

- Prefer a predictable repayment structure and fixed monthly payments

HELOC Best Fit

A HELOC may be a great solution for borrowers who:

- Need ongoing access to funds and want the flexibility to draw money as needed

- Require flexible borrowing to cover ongoing expenses, such as staged renovations

- Are comfortable with variable rates and potentially changing payments

Cash-Out Refinancing Best Fit

A cash-out refinancing might benefit borrowers who:

- Want to replace the first mortgage and improve its terms – for example, lowering the rate or converting an adjustable-rate mortgage to a fixed-rate loan – while accessing the equity

- Need a larger amount of cash than a second mortgage can provide

- Prefer to have one combined payment, instead of managing a first mortgage and a separate second lien

Risks and Tradeoffs

Whether your client chooses a second mortgage, a HELOC, or cash-out refinancing, the decision comes with its costs. Ensure that the borrower understands the risks they are taking. Below are some of the most common considerations, although the exact drawbacks depend on the borrower’s profile and financial situation.

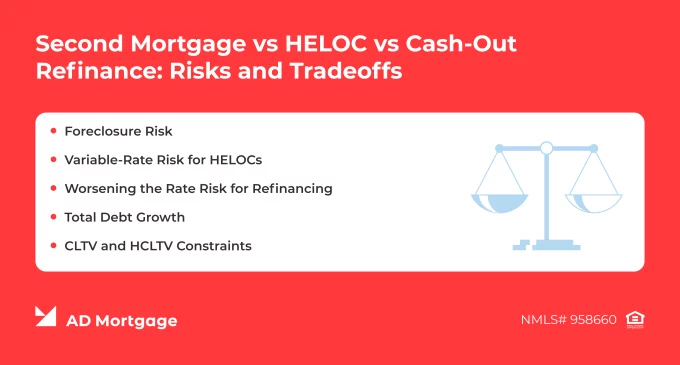

Foreclosure Risk

As all three solutions – home equity loans, HELOCs, and cash-out refinancing – are secured by the property, failing to make payments might lead to foreclosure. Therefore, the borrower must carefully review their debt obligations and their ability to manage additional payments to mitigate this serious risk.

Variable-Rate Risk for HELOCs

While home equity second mortgages mostly feature a fixed rate, HELOCs typically feature variable rates. Therefore, monthly payments may change over time, making budgeting more challenging.

Higher Rate Risk for Refinancing

Cash-out refinancing not only allows borrowers to access home equity but also resets the mortgage terms. A new mortgage might come with a higher interest rate – which is common in the current rate environment – a different payment structure, or other drawbacks that outweigh the value of the existing mortgage.

Total Debt Growth

Borrowing against built equity increases the amount of debt, which may limit future financing options. Additionally, if property values decline, homeowners may have less remaining equity, making it more difficult to refinance, sell the property, or access additional financing.

CLTV and HCLTV Constraints

During underwriting, the lender checks the Combined Loan-to-Value (CLTV) or High Combined Loan-to-Value (HCLTV) ratios to ensure that the total debt secured by the property remains within program limits.

Example Borrower Scenarios

To better understand how to match a borrower’s needs with the right solution, let’s look at a few examples.

Example 1. Low Mortgage Rate and Renovation

Borrower Situation: A homeowner has an existing mortgage with an interest rate of 3.25% that they would like to preserve. They need a large sum of money for a kitchen renovation.

Potential Fit: Home equity second mortgage.

Explanation: A second mortgage will allow the borrower to keep the first mortgage on its current terms while accessing their home equity. Additionally, unlike a HELOC, a home equity loan offers a lump sum of money at closing, providing fixed payments and a predictable repayment schedule.

Example 2. Unpredictable Repair Expenses

Borrower Situation: A homeowner is planning to make multiple home improvements over the next year but does not know yet when the funds will be needed.

Potential Fit: HELOC.

Explanation: With a HELOC, the borrower can draw funds as needed instead of getting a lump sum at closing and then paying interest on unused money.

Example 3. High Adjustable-Rate Mortgage

Borrower Situation: A homeowner has an adjustable-rate mortgage with a current interest rate of 7.25% and wants to lower the rate while accessing home equity.

Potential Fit: Cash-out refinancing.

Explanation: Refinancing will allow to reset the mortgage terms, potentially lowering the interest rate and converting an adjustable-rate mortgage to a fixed-rate loan. Additionally, the borrower will receive the difference between the new loan amount and the remaining balance on the current mortgage in cash.

Broker Talking Points

- ‘First, let’s decide the purpose – why do you want to take out a second mortgage or refinance? Often, people use these solutions to access equity when they have large expenses like home renovations or medical expenses.’

- ‘If you have a high-rate existing mortgage, then refinancing might be the right option. It might allow you to lower the rate while getting the difference between the new loan amount and the remaining balance on your current mortgage in cash.’

- ‘A HELOC is a great choice if you need flexibility in drawing funds. This solution functions as a line of credit so you can access funds when needed.’

- ‘Home equity second mortgages offer a fixed rate and predictable payment structure, while keeping the primary mortgage. Great fit for large, one-time expenses.’

Conclusion

The right solution for your client depends on a variety of factors – the first-lien rate, borrowing purpose, built equity, repayment plan, and payment-risk tolerance.

AD Mortgage – the Lender of Choice, voted for by more than 1,000 mortgage experts – is here to help you serve your clients smoothly and efficiently. Submit a Scenario Request, and our managers will contact you within 30 minutes with a tailored loan solution.

FAQ: Second Mortgage vs Home Equity Line of Credit vs Cash-Out Refinancing

Is a HELOC the Same as a Second Mortgage?

No. A HELOC (or home equity line of credit) is a type of second mortgage, but it is unique. It provides a line of credit, allowing borrowers to withdraw money as needed while keeping the first mortgage.

Is a Second Mortgage Better than a HELOC?

There is no single option that best fits every client – the solution should be chosen based on the borrower’s preferences and current situation. Home equity second mortgages offer a lump sum at closing and typically fixed payments – a great option for one-time, large expenses. HELOCs provide a line of credit and a less predictable repayment structure – a good fit for ongoing or unpredictable borrowing needs.

Is a Cash-Out Refinance Better than a Second Mortgage?

Cash-out refinancing might be a preferred option if the borrower wants to reset the loan terms. However, if the current mortgage rate is low and the homeowner wants to preserve it, a second mortgage might be a better solution for accessing home equity.

Which Option Lets the Borrower Keep the First Mortgage?

Second mortgages, including both home equity loans and HELOCs, allow the borrower to keep the existing mortgage on its current terms and take out a new one, using the same property as collateral.

Which Option Has the Most Payment Stability?

Home equity second mortgages typically feature fixed monthly payments, ensuring a high level of predictability. Cash-out refinancing can also provide predictable monthly payments if the new loan has a fixed interest rate.

Which Option is Best for Home Improvements?

If home improvements will require one-time expenses, home equity loans or cash-out refinancing might be the most suitable options as they offer a lump sum of money at closing. For ongoing or unpredictable expenses, HELOCs may be a better fit because of their flexibility when it comes to drawing funds.

Which Option is Best for Debt Consolidation?

All three options can be used for debt consolidation. Submit a Scenario Request to help us choose the best-fit solution for your client’s case.

Can a Borrower Have Both a First Mortgage and a HELOC?

Yes. A HELOC is a type of second mortgage, so it co-exists with a first mortgage, remaining subordinate to it.

Does a HELOC Affect Refinancing?

Yes. A HELOC can affect refinancing because it is counted as debt in underwriting and may impact eligibility. It also requires a subordination agreement so the new mortgage can stay in first-lien position, which must be approved by the HELOC lender.

When Should a Borrower Avoid Cash-Out Refinancing?

Cash-out refinancing does not fit when a borrower wants to keep their first mortgage on its current terms or needs a line of credit instead of a lump sum at closing.

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again