Post content:

Refinancing is a replacement of the borrower’s current mortgage with a new one that features better conditions. Before 2022, when rates were significantly lower, mortgage refinancing was a common solution, helping to reduce monthly payments.

In today’s market, refinancing is still a powerful solution. Further in the article, we give actionable client advice for mortgage originators on how brokers can use refinancing as a tool.

Key Takeaways

- Refinancing is a way for a borrower to make their loan terms better by replacing an existing loan with a new one. It usually helps to lower the interest rate, switch from adjustable to fixed rates, or borrow against home equity.

- Brokers need to educate their clients about associated costs. Usually, refinancing takes from 30 to 45 days and features closing costs of 2% to 5% of the loan amount.

- As a result of refinancing, the borrower must achieve a clear financial benefit. Therefore, it is crucial to evaluate both monthly and overall impact of refinancing the mortgage.

What is Mortgage Refinancing?

The direct answer is – refinancing is replacing the existing mortgage with another one, improving loan terms. A net tangible benefit is required, and as a result of refinancing, the borrower must receive an obvious financial advantage.

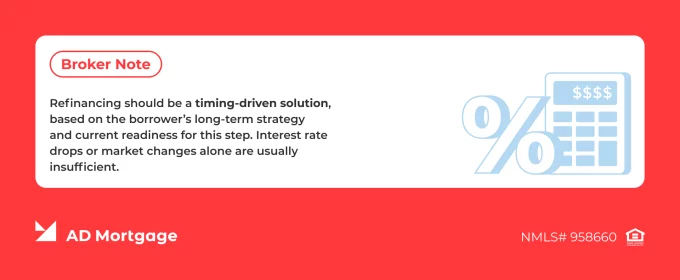

Brokers should explain to their clients the core idea that refinancing is not always about lowering the rate. There are other refinance benefits, including changing the loan terms or borrowing against their equity. Refinancing is a strong solution, and it should be structured in alignment with the borrower’s long-term goals.

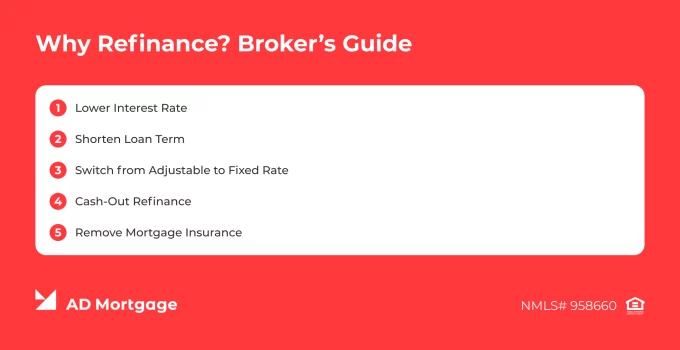

Why Refinance?

There are several reasons why borrowers might want to refinance their mortgage, depending on the long-term plans and current situation:

- Lower Interest Rate → This is the most desired outcome of refinancing for many borrowers.

- Shorten Loan Term → The borrower can reduce their overall interest by switching a 30-year mortgage to a 15-year mortgage. Extending the timeline is also possible if this option better fits the borrower’s needs.

- Switch from Adjustable to Fixed Rate → Fixed rate ensures more predictability and stability. However, when the rate drops, switching from fixed to adjustable rate can help reduce monthly payments.

- Cash-Out Refinance → Borrowing against equity allows homeowners to make various improvements, such as consolidating debts or home renovations.

- Remove Mortgage Insurance → To cancel private mortgage insurance (PMI) on conventional loans, lenders require for the borrower to reach at least 20% equity. If refinancing allows the required equity level to be reached, then PMI can be canceled.

Types of Mortgage Refinancing

There are several types of loan refinancing, differing by the goal they help to achieve. These are the most common types:

- Rate-and-Term Refinance. Improves the interest rate or loan terms. This is the most common type of refinancing that replaces an existing loan with one with better terms but without increasing the principal.

Despite the potential benefits, brokers must carefully evaluate closing costs and qualification requirements to ensure that refinancing makes sense in the long term. - Cash-Out Refinance. Allows your client to borrow against built-up equity. The existing loan is replaced with a new one with a larger loan amount – and the borrower receives the difference as cash. These funds can be spent on home improvements, debt consolidation, or other purposes.

Note that after cash-out, the new loan term might include higher monthly payments or longer repayment period. - FHA or VA Refinancing. Often offers better terms, thanks to government backing. Compared to conventional loans, FHA or VA refinance solutions usually feature more straightforward flow with limited documentation for eligible borrowers.

- ARM to Fixed Rate Conversion. Protects the borrower from rate increases and payment growth. With an adjustable-rate mortgage (ARM), the interest rate adjusts to market indexes and changes according to loan terms. Therefore, monthly payments can unexpectedly grow. A fixed rate, on the contrary, ensures stability and prevents the borrower from paying more if the rate grows.

How the Refinancing Process Works

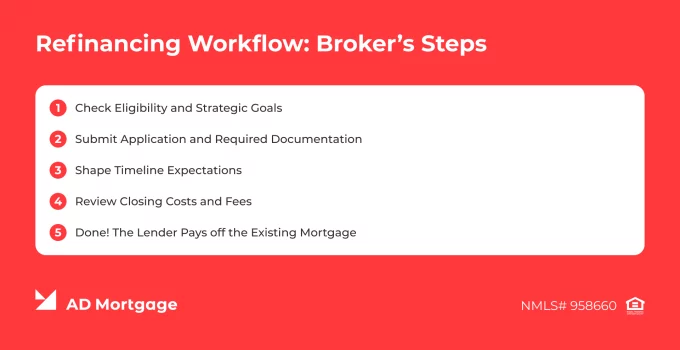

A broker’s job is not limited to advising their client to refinance mortgage when there is a clear financial benefit of this option. They also often educate borrowers and guide them through the whole process. We divided the refinance flow into five steps:

1. Check Eligibility and Strategic Goals

Start with ensuring that refinancing fits into the borrower’s financial strategy. For example, if your client’s goal is to reduce their mortgage balance, then cash-out refinance will not be the best choice.

The second step is checking eligibility. Lenders set their own requirements, and the broker must ensure that their client fits into guidelines. For conventional loans, requirements often feature having at least 20% home equity, the debt-to-income ratio under 43%, and on-time mortgage payments.

2. Submit Application and Required Documentation

For the application, the broker needs to collect all required documentation and information about the borrower, their loan, and the property. Pay stubs, W-2 form, tax returns, and other documentation may be required to verify income and assets. The lender might require credit checks, an appraisal, and a title search.

Be sure to check the exact documentation requirements with the mortgage lender.

3. Shape Timeline Expectations

Explain to your client how long refinancing takes so that they have clear expectations about the process. Typically, the refinancing process lasts between 30 and 45 days. This can take longer in some cases with complex files.

Underwriting is performed within one to three weeks. After that, the file is ready for closing.

4. Review Closing Costs and Fees

The closing costs are also considered when calculating the financial benefit of refinancing. Generally, refinancing closing costs are 2%-5% of the loan amount. They include lender and appraisal fees, title insurance, and other expenses.

Lender-paid costs are sometimes possible, but they result in higher interest rates or longer loan terms. Also, the expenses might be rolled into the loan balance. Nonetheless, ‘no-fee’ refinancing does not eliminate closing costs.

5. Done! The Lender Pays off the Existing Mortgage

The lender pays off the previous mortgage, and after that, the borrower is responsible for maintaining the new mortgage on the new terms. The broker’s post-closing role is in managing communication between the borrower and the lender.

Evaluating if Refinancing is Right

Reducing monthly payments might seem like a key goal of refinancing. However, it is not always true. While lower payments are positive, they are insufficient to evaluate the whole picture. For example, payments can be reduced when the loan terms are prolonged – and as a result the total costs are higher.

To check how the refinancing will impact the borrower’s situation, brokers can ask the following questions:

- What will the monthly savings be?

- How will the loan term change?

- Will the total costs be reduced?

- What are the closing costs? How long will it take to break even?

- How long does the borrower plan to stay in the home? Do they plan to move or sell the property in the near future?

A great tool to check whether refinancing makes sense is a mortgage refinance calculator. It can help analyze the total savings and the ‘break even’ point to determine how refinancing will impact the borrower’s financial situation.

Tips for Brokers to Advise Clients

Refinancing is a broad topic, and your clients might have difficulties understanding how the process works. To shape realistic expectations, brokers can focus on three key points in their communication – opportunities, calculations, and drawbacks.

How to Identify Opportunities

State clearly: Just because you can refinance, it does not necessarily mean that you should. There must be clear indicators of financial benefits, including lower interest rates, more predictable loan terms, debt consolidation, or other improvements.

Market conditions might have their impact on the decision, but the borrower’s strategic goals should be the priority.

How to Calculate Savings

The broker needs to compare their client’s old and new loans in detail to check the exact financial benefit of refinancing. While savings play a huge role, the ‘break-even’ point is also important as it shows how much time it will take to cover the closing costs.

Savings must be evaluated both short-term and long-term to make a reasonable decision.

What are the Downfalls and Costs

Refinancing is not a universal tool, and some of its features might be potential drawbacks for borrowers. The following nuances should be considered:

- Closing costs

- Timeline and required documentation

- Changes in loan term and, therefore, in total interest

- Higher rate or loan balance in case of ‘no-cost’ refinance

- Appraisal risks

- Prepayment penalties if applicable

Refinancing has its costs and risks, which must be carefully evaluated in advance.

Mortgage Refinancing Pros and Cons

Refinancing has its positive and negative sides – both of which must be considered by the broker and the borrower. Share the following pros and cons with your client to shape clear expectations about refinancing.

Refinancing Pros

- Improvement of loan terms – through lower interest rates, more predictable payments, or shorter timelines

- Receiving tax-free cash – if borrowing against home equity during cash-out refinancing

- Better alignment with the financial strategy – since refinancing allows for reconsideration and improved loan terms

- Switching loan type – for example, one can refinance a Non-QM loan into a traditional mortgage if they qualify

Refinancing Cons

- Closing costs – appraisal fees, lender fees, title costs, and other expenses

- Prepayment penalties – some loans charge penalties for paying off the original loan early

- Lengthy underwriting – which might require extensive documentation and a property appraisal

- Changes in loan terms – while overall terms improve after refinancing, certain benefits of the original loan might be lost

FAQ: Mortgage Refinancing

How Long Does Refinancing Take?

Refinancing takes from 30 to 45 days in general. Several factors – including the complexity of the file, whether an appraisal is required, or lender preparedness – influence the timeline.

Cash-out refinancing typically requires more time – often up to 60 days. The reason for that is stricter underwriting and more careful home value evaluation.

Can I Refinance with Bad Credit?

To refinance a conventional mortgage, the borrower is usually required to have a credit score of 630 or higher. Some lenders might accept files with lower scores, but with strong compensating factors demonstrated.

Other types of mortgages, including government-backed FHA or VA solutions, generally offer more flexible guidelines and can accept scores as low as 580.

Even if qualifying, files with ‘bad credit’ often refinance with higher interest rates or stricter underwriting.

Will Refinancing Reset My Mortgage Term?

Refinancing means replacing an existing mortgage with a new one, with new terms. Therefore, it is an opportunity to choose loan terms that better fit the borrower’s strategic plans. For example, a borrower has been paying on a 30-year loan for 10 years and wants to refinance. They can choose a mortgage with a 10-year or 20-year term. Depending on what option they choose, the remaining period will become shorter or stay similar.

Is Refinancing Worth It if Rates are Only Slightly Lower?

It depends. Sometimes, refinancing is performed not to reduce rates but to reach other benefits instead – for example, lower loan balance or improve loan structure. Evaluate your client’s situation as a whole and calculate overall savings to check whether refinancing makes sense for them.

Choose among 20+ programs and get

Looking for a suitable loan program?

a detailed loan calculation

Conclusion

To conclude, refinancing is a useful solution that can improve the borrower’s situation in several ways, such as achieving better interest rates, more predictable terms, or consolidating their debts. However, refinancing comes with its costs, and brokers must carefully evaluate the net tangible benefits it brings to the client.

To check how refinancing can work out for your client, submit a Scenario Request at the AD Mortgage website: Scenario Request Form | AD Mortgage

For broker-oriented guidance and useful advice, visit our Learning Center: Mortgage Learning Center | AD Mortgage

Thank you!

We’ll contact you as soon as possible

Oops, something went wrong

Please try to send form again