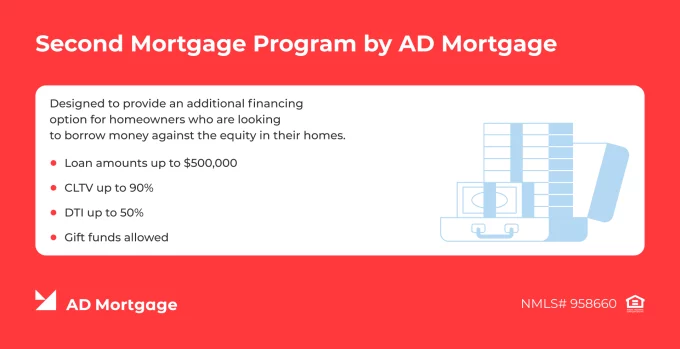

Second mortgages – including home equity loans and HELOCs – can be used to fund home renovations, repairs, and upgrades. A home equity loan provides a fixed-rate lump sum at closing and fits one-time major projects such as kitchen remodels or roof replacement. A HELOC provides a revolving line of credit and fits staged or unpredictable renovation costs. AD Mortgage offers closed-end Second Mortgage loans with amounts up to $500,000, CLTVs up to 90%, and DTIs up to 50% (program terms as of July 2026).

This guide helps brokers match each renovation scenario to the right structure – and explains the tax and qualification rules that shape the recommendation.

Can You Use a Second Mortgage for Home Improvements?

Yes, second mortgages can be used for home renovations, repairs, and upgrades. Second mortgages are a common solution for home improvements because they usually allow borrowers to qualify for larger amounts and potentially access better interest rates than other types of loans that are not secured by the property.

The choice of a second mortgage type depends on the type of planned repairs. The loan purpose plays a crucial role in structuring the loan – submit your client’s scenario and our experts will contact you with a best-fit solution.

Key Takeaways

- Second mortgages can be used for home repairs, improvements, and upgrades. They usually offer more favorable conditions than personal loans or credit cards because they are secured by the property.

- Home equity loans offer a lump sum at closing and therefore are most useful for one-time major projects. HELOCs work better for ongoing or unpredictable expenses because they operate like a line of credit.

- Some substantial renovations might help eligible borrowers qualify for tax benefits – however, tax rules vary and should be discussed with a tax professional.

- AD Mortgage offers closed-end Second Mortgage loans with loan amounts up to $500,000, CLTVs up to 90%, and DTIs up to 50% that may be used for home improvements.

When a Second Mortgage May Fit a Renovation Project

A home equity second mortgage is a common solution for home improvements because it offers fixed interest rates, a predictable payment structure, and a lump sum at closing. Home equity loans work better when the borrower:

- Wants to keep the first mortgage and access home equity

- Plans a one-time repair project and understands the budget

- Seeks repayment stability and predictable monthly payments

- Has sufficient equity in the property to qualify for a second mortgage

For example, home equity loans may be the right choice for funding home additions, kitchen or bathroom renovations, roof replacement, or other major improvements.

Second Mortgage vs HELOC for Home Improvements

Borrowers often compare home equity second mortgages to HELOCs when choosing the best way to access home equity for home improvements. We have prepared a detailed comparison table focused specifically on renovation projects, but for a higher-level overview, read our recent article: Second Mortgage vs HELOC

| Comparison | Home Equity Second Mortgage | HELOC |

|---|---|---|

| Funding Method | Lump sum at closing | Revolving line of credit |

| Rate Type | Typically fixed | Typically variable |

| Payment Stability | Stable, predictable monthly payments | Payments may vary based on interest rates and the amount borrowed |

| Staged Projects | Less suitable because funds are provided upfront | Better fit because they offer flexible access to funds |

| Overborrowing Risk | Risk of borrowing more than needed upfront | Behavioral risks because the line of credit allows to draw funds any time |

| Best Use Case | Large, one-time expenses on major projects | Ongoing or unpredictable expenses on staged projects |

AD Mortgage helps brokers offer more financing options to borrowers, finding a right fit even for nonstandard cases. Submit a Scenario, and our managers will contact you with a tailored solution within 30 minutes.

Second Mortgage vs Cash-Out Refinance for Renovations

Cash-out refinancing is another mortgage solution that can be used for funding home renovations. However, it differs drastically from a second mortgage:

- Refinancing replaces the first mortgage with a new, larger loan with a new interest rate and repayment term. A second mortgage, on the other hand, keeps the first mortgage and adds a new loan with a separate repayment term.

- With refinancing, the borrower replaces the first lien rate with the new mortgage rate. According to Freddie Mac’s Primary Mortgage Market Survey, the rates are higher now, in the 2026 tax year, than they were several years ago. Fewer people choose refinancing because they want to keep their lower existing mortgage rate.

- Closing costs and the amortization schedule must be carefully compared when making a decision.

AD Mortgage provides ADwise, an automated guideline search tool that brokers can use freely to reduce the time spent on manual research and get instant, policy‑aligned answers. Try ADwise to move your deals forward faster.

Tax Considerations for Home Improvement Borrowing

Certain substantial improvements funded by second mortgages may qualify for tax benefits. This is one of the reasons why understanding the purpose of the second loan is crucial – second mortgages used for debt consolidation or medical expenses, for example, may not qualify for the same tax treatment.

Qualification for tax benefits depends on the type of improvements. Major renovations that increase the property value may potentially qualify, while minor, cosmetic repairs may not qualify under applicable tax rules.

Tax rules vary based on the individual situation and current tax regulations – for the 2026 tax year, IRS Publication 936 applies. Therefore, consulting with a tax professional is crucial.

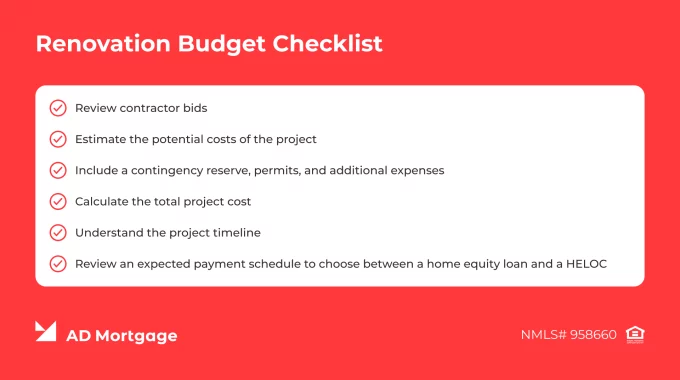

How Brokers Should Help Borrowers Budget the Project

Borrowing the maximum allowed amount is not the right approach. It increases the debt burden and leads to a potentially higher foreclosure risk. That is why brokers should help their clients accurately evaluate the appropriate loan amount based on their actual needs.

Start by reviewing contractor bids and estimating the potential costs of the project. Note that the repair budget often changes, so include a contingency reserve, permits, and additional expenses when calculating the total project cost.

Understand the timeline of the project and the expected payment schedule to choose between a home equity loan and a HELOC. For major projects with fixed expenses, home equity loans might work better, while HELOCs are often used for ongoing projects completed in stages.

What Requirements Matter Most?

Qualification for second loans depends on the borrower’s profile, underwriting requirements, and lender guidelines. However, there are several common requirements across different lenders:

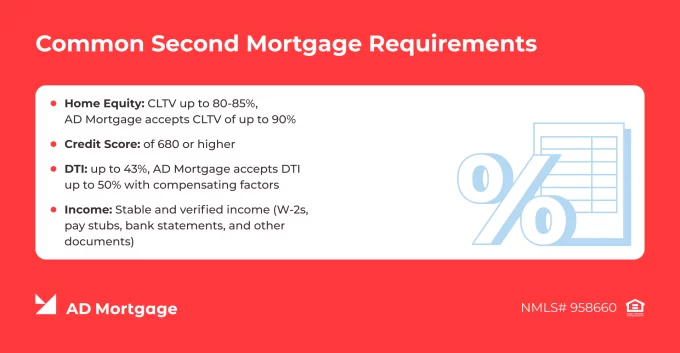

- Home Equity and CLTV. Lenders review the CLTV ratio to ensure the borrower has enough equity to secure the loan. AD Mortgage allows CLTV of up to 90% in the Second Mortgage program.

- Credit Profile. The borrower’s credit score, payment history, and recent credit events are reviewed to ensure creditworthiness. Usually, lenders accept credit scores of 620 or higher for second mortgages, according to Investopedia.

- DTI. Lenders compare the borrower’s debt obligations with their monthly income to determine whether the borrower has the capacity to cover their obligations. A DTI of less than 43% is a common benchmark, while AD Mortgage accepts DTIs up to 50% under the Second Mortgage program.

- Property Type. Eligibility varies based on the property and occupancy type. Requirements might be stricter for investment properties, condos, and other properties, depending on lender rules.

- Income Documentation. Income must be verified according to lender guidelines, and various documents – including pay stubs, W-2 forms, and bank statements – are usually accepted.

- Loan Amount. The required amount must align with the renovation plan and project budget. Note that a higher amount generally requires a stronger borrower profile.

- Reserves. Some second loan programs require borrowers to demonstrate reserve funds remaining after closing.

AD Mortgage serves brokers with complex or out-of-the-box borrower scenarios – submit a Scenario Request and our experts will suggest the right mortgage solution even for nonstandard cases.

Example Renovation Scenarios

Different client situations require different mortgage solutions. We describe three examples of how borrowers can most efficiently access equity for home improvements. Note that these examples are for illustration and educational purposes only.

Example 1. Major Kitchen Renovation and Low-Rate First Lien

Borrower Situation: A homeowner wants to renovate their outdated kitchen, hoping that a new design will result in a higher property value. The contractor estimated that the project will cost $75,000, and the homeowner needs to access their home equity to cover the expenses. However, their first-lien rate is low, so they would like to keep it.

Solution: A home equity loan allows the borrower to keep the first mortgage and take out a new loan, with a lump sum at closing, fixed payments, and a predictable repayment timeline.

Example 2. Minor Staged Repairs and Unpredictable Costs

Borrower Situation: A homeowner has a list of small repairs they are planning to complete over the next 12-18 months – update flooring, replace electrical components, and service the HVAC system. They expect these improvements to be ongoing and do not know the exact costs.

Solution: A HELOC for home improvements provides a revolving line of credit, allowing the borrower to withdraw funds as needed – instead of borrowing a fixed amount upfront.

Example 3. Home Improvements and Higher-Than-Market Rates

Borrower Situation: A homeowner’s first mortgage has an interest rate that is higher than current mortgage rates. The borrower plans to make home improvements and would like to access equity while lowering their interest rate.

Solution: A cash-out refinance for renovations replaces the first mortgage with a new one, allowing the borrower to obtain a lower interest rate if eligible. The borrower can refinance into a larger loan and receive the difference in cash to finance home improvements.

AD Mortgage offers a full range of loan programs, helping you match your clients with the right mortgage solution.

Broker Talking Points

- ‘A second mortgage is a great source of funding for home improvement. Are you planning to make one-time or staged renovations? That directly impacts the choice of mortgage solution.’

- ‘Home equity loans are often a better fit for major one-time renovations because they provide a lump sum at closing. HELOCs are mostly used for ongoing projects with uncertain costs.’

- ‘AD Mortgage offers a closed-end Second Mortgage program with maximum loan amounts of up to $500,000.’

Conclusion

Taking out a second mortgage for home repairs is a great opportunity for a homeowner to improve their house, access equity without refinancing, and potentially even qualify for tax deductions.

AD Mortgage is a wholesale mortgage lender that offers a wide range of mortgage solutions. Use an innovative, award-winning Quick Pricer to calculate the loan terms for your client scenario.

FAQ: Home Improvement Second Mortgage

Can You Use a Second Mortgage for Home Improvement?

Yes. Second mortgages can be used for home improvement, debt consolidation, covering medical expenses, and other purposes.

Is a Second Mortgage Better than a HELOC for Renovations?

A HELOC and a home equity loan for home improvements are favorable options in different scenarios. HELOCs work best with ongoing projects because a revolving credit line allows borrowers to withdraw funds as needed. Home equity loans are used mostly for one-time major projects because they provide a lump sum at closing.

Is Second Mortgage Interest Tax Deductible for Home Improvements?

It may be. Under current IRS rules (IRS Publication 936), interest on home equity debt is deductible only when the loan proceeds are used to buy, build, or substantially improve the home that secures the debt, and the debt falls within the applicable mortgage limit.

What Home Improvements May Qualify for Interest Deductibility?

Certain substantial home improvements that increase property value – such as major renovations or home additions – might qualify for interest deductibility, according to IRS Publication 936. Consult with a tax professional for details.

Is a Cash-Out Refinance Better for Home Improvements?

If a borrower wants to replace an existing mortgage with a new one on new terms, then it may be. Second mortgages, on the other hand, keep the first mortgage and provide a new loan on separate terms.

How Much Can You Borrow for Home Repairs?

The borrowing limit depends on available equity, existing debt, and lender CLTV requirements. Read our article to learn how to calculate the available borrowing amount in detail.

Can Investors Use a Second Mortgage for Property Improvements?

That depends on the lender‘s requirements. AD Mortgage offers Second Mortgage loans with loan amounts up to $500,000 for owner-occupied, second home, and investment properties.

What Should Borrowers Prepare Before Applying?

Borrowers should prepare both financial and project-related documentation before applying for a second mortgage. Brokers should collect income documentation, credit reports, the project budget, and other information in advance to help move the loan through the approval process more efficiently.